Our 50s is the time we’ve all been waiting for—time to celebrate. We were brilliant in our 20s, chose a good partner in our 30s, and avoided debt in our 40s—now it’s time to party. Am I right?

Not really. Welcome back to the Staying Debt-Free in At Any Age series (20s, 30s, 40s), where I discuss the life-changing benefits of living below your means.

Everything comes together. If you focused a little bit (not even a lot) on your finances, debt, and budget earlier in life, you should be doing pretty well in your 50s.

Fundrise vs. USDC

However, having cash flow in your 50s leads many people to misjudge their financial security and, even worse, their financial responsibilities. Here are some things people overlook:

- Estate planning

- Paying for kids’ college

- Kids weddings

- Long-Term care/health planning

I’ll go into these a little more in-depth, but I want to take a quick detour to my time in Afghanistan.

Military Service 101. Traveling into a deployment zone is long and arduous. Think about it like traveling from a small city on the west coast of America to another small town on America’s east coast.

From Dirt to Dividends 3

When I traveled from Yuma, Arizona, to Beaufort, South Carolina, I would have to transfer to small and large airports to get to my destination.

It’s the same as when you travel to a warzone. You’ll be shuffled through airports, camps, and bases until you reach your final destination. Sometimes it can take ten days to get to your last zone.

As you retrograde and return stateside, you must stay focused on the mission. In my case, my mission was to get back to my wife with a newborn baby I hadn’t met before. Many people start to celebrate too early, and delays and other trouble will occur.

How We Plan to Retire on Dividends 3

Staying the distance. I bring up this story because many people lose focus in their 50s. You’ll start to see it as people enter their 40s because this is the first generation of 40-year-olds to have social media.

It’s a mess. Many people think they made it in their 40s and 50s. They are celebrating too early. We spend money on ourselves without thinking about how our children are doing financially.

If we expect our children to succeed 100% on their own, why do they need us? While we are off traveling to Hawaii, buying Teslas, and eating at expensive restaurants, our children are probably struggling and unhappy.

Working syndrome. We get this mentality of “we deserve to spend our money as we wish” from working hard at our day jobs.

Dividends vs. Social Security

Once we hit 50, we have been in the workforce for 30 years. We have no retirement date in sight, so we convince ourselves to “enjoy” our day-to-day lives as best as possible.

We can stay out of debt reasonably easily in our 50s because we should be making good money. However, we also are avoiding significant contributions to our kids, health, and retirement. We are living for today.

Working for money. If you are still working for money in your 50s, you’ll have a tough time towards the end of your life. You need to work for assets. Let’s break this down further.

If you are making $10,000/month in after-tax revenue, how much should you use to buy dividends, real estate, or invest in a business? It should be over 50% (at minimum).

Happy Cash Flow Retirement 7

However, in our 50s, we can fall into over-consumption and lifestyle inflation traps. Over-consumption means we are eating out, traveling, and shopping too much.

Lifestyle inflation means buying nice cars, homes, and gifts, which increases our expenses to match (or overtake) our income. We become cash flow neutral or negative.

We forget about our kids. Most people in their 50s don’t have great relationships with their kids. We celebrate our new financial liberties as we send our kids off to college and the workforce.

However, you have to become a callous person to survive in the real world. Once our children survive without our help, they will become different people. They won’t seek our advice and guidance because they figured things out independently.

Retirement Plus: Use Royalties to Supplement Your Retirement

On an island. Think of it this way. From ages zero to 18, we prepare our kids to survive on a deserted island. At age 18, we fly them over the island and kick them out of the plane with a parachute.

Very few of our kids can thrive, or even survive, on the jungle island. The few that survive make it back to America. Do you think that they will need or respect you after surviving alone? Do you think they owe you anything?

Where were we, the parents, while our kids were on the island? We were on vacation, buying new trucks, ATVs, sandrails, etc. We were trying to relive our childhood by avoiding being adults.

Build Your Rep: Create Your Body of Work

Thus, we are not around when it’s time to pay for a kid’s college, a house down payment, a baby shower, a honeymoon, or a new car. Our kids get into massive debt, affecting their marriage and mental health.

The allure of social media. As I watch my peers (I’m 41) on social media, I think about their kids. Every day I see people my age and in their 50s getting sleeve tattoos, new cars, motorcycles, etc.

However, what should we see on social media at this age? Long-term care insurance, life insurance, irrevocable trust, and land trusts come to mind. We should see business partnerships, real estate deals, and content creation successes.

Being an adult sucks, but it’s actually the real fun of life. I have brokerage accounts for five children—my two sons, two nephews, and one niece. I buy Series “I” bonds for my kids and have a house for each.

Retire by Age 38 in 10 Easy Steps

As the stock market goes into a downturn, I am buying index funds into these children’s accounts. They will experience the power of compounding at a very early age.

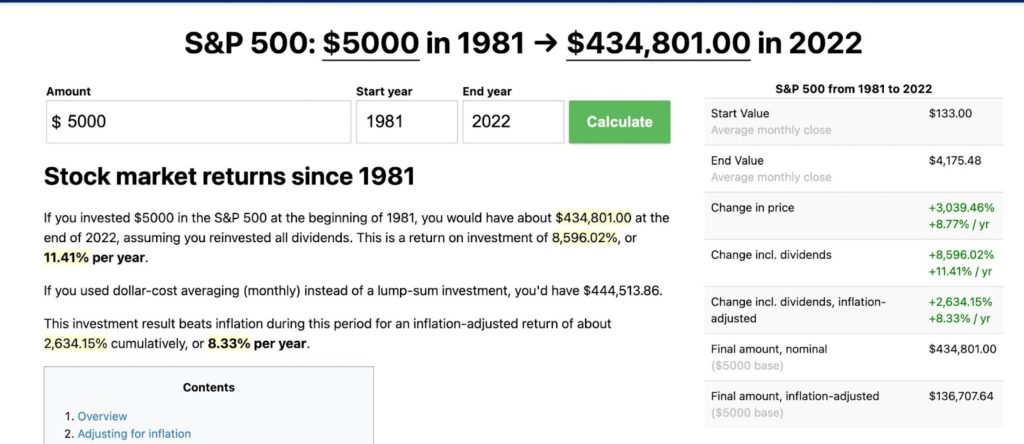

The value of compounding. I was born in 1981. If my parents had invested $5,000 on the day of my birth, that cash would have multiplied into $434,000. Yes, seriously.

Before we go off and spend all types of money on ourselves because “we deserve it,” let’s ensure our families have the resources they need for success. I could buy a house with this $434,000.

Is Your Neighborhood Being Overtaken by Investors?

It’s not all serious. Now, if you have your act together, you can have a great time in your 50s. Here are some goals you may want to set before splurging on yourself.

- Be debt-free

- Have $10,000/month free cash flow (difference between income & expenses)

- Have a brokerage account, savings, bonds, or college account, for children

- Have a plan to assist kids with buying a home

- Have a plan for medical savings, long-term care, etc.

Once you have a solid plan for yourself and your children, you are free to spend some money on yourselves. Don’t forget that your parents may need assistance.

Conclusion. It sounds boring, but being an adult is quite fun. You’ll understand things people overlook daily. You follow interest rates, mortgage loans, and changes in tax laws.

REITs vs Homeownership: The Fun of Fundrise

The best part is that you are giving this information to your children. They do not have to wait until 50 to use this vital data analysis.

I learned how to publish a book in a week. As my son leaves home, he may meet a woman who likes to write. If they marry, I can work with her to start writing and publishing books as she prepares for children.

There is no need to send her off into the workforce. She can build an audience in her 20s, have kids in her 30s, and coast in her 40s. Why would I want my son and daughter-in-law to go along the same path I traveled to reach financial security? They can accomplish much faster with less friction.

So, is the fun in life buying a boat or helping a young marriage survive and thrive? You’ll have to decide. I know where my answer lies; how about you?

- PDF of the Month: Make $500/Month in Dividends (pdf)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 6 (Free 409-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: Can Grammarly Make You a Better Writer?

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Monthly Dividend Tracker (XLSX): Check it out on Etsy

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply