So you are still average? Great, so am I. There is no reason to whine or cry about our “basic” lifestyle. In fact, it is something to celebrate. When we lead normal, everyday lives, there is no outside influence for us to live above our means.

This is part two in the Retirement Planning for the Average Person series. Find the first article here and download the free pdf here. Now, back to our regularly scheduled program.

If we were movie stars or football players, we would expect to have massive homes and expensive sports cars. But we aren’t those people, nor do we need what these people have. Or do we?

Create Content for Your Home-Based Business

Herein lies the rub—us middle-class folks have started to want this nice stuff. Even worse, we want this nice stuff from earned income jobs. Trying to live these amazing lifestyles can have an adverse effect on our retirement and estate planning.

Do you know the difference between an asset and a liability? If not, let’s do a quick refresher. First, the book you need to read is “Rich Dad Poor Dad” to get the best information on changing your mindset. Now, for the definitions.

An asset puts money into your pocket and a liability takes money away from your pocket. Under these simple definitions, is your house an asset or liability? My primary residence is an asset because our two roommates cover the full mortgage—we achieved mortgage positive.

Since we are average, we should not be collecting liabilities. Yet, here we are buying new cars, boats, RVs, sandrails, etc. Each time we buy a liability we are doing double damage to our retirement plan. Here’s how:

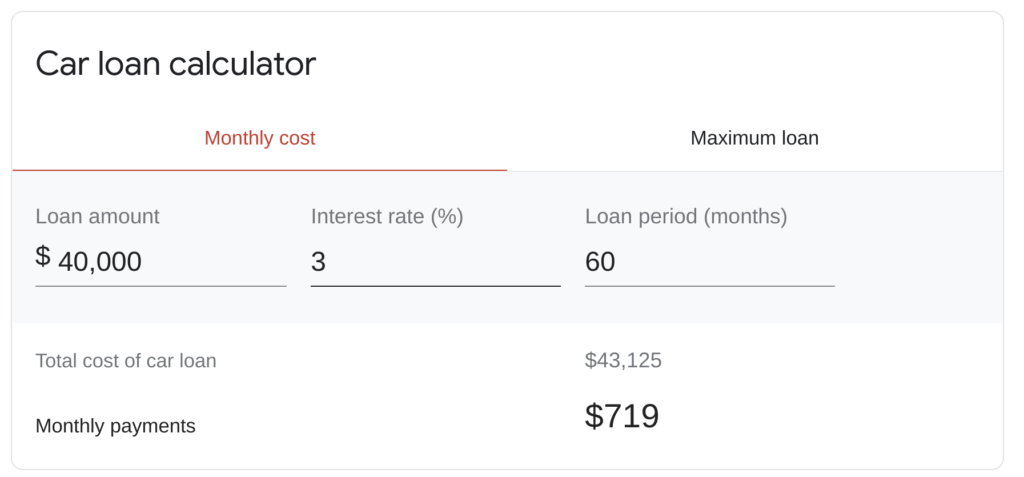

Let’s take the example of buying a car for $40,000. We take a loan at 3% for 60 months, leaving us with a payment of $719/month. The total amount of the loan will be $43,125. That doesn’t seem too bad on the surface.

Start a Community Garden and U-Pick-It Farm

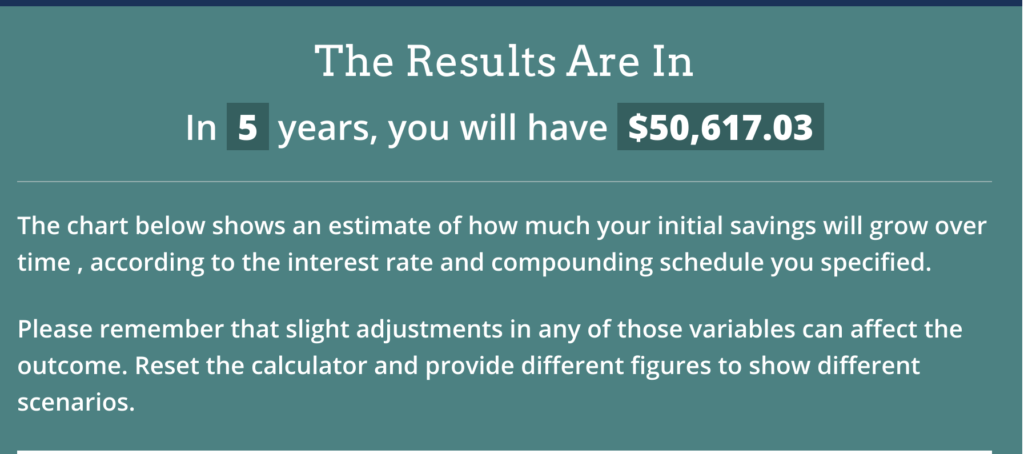

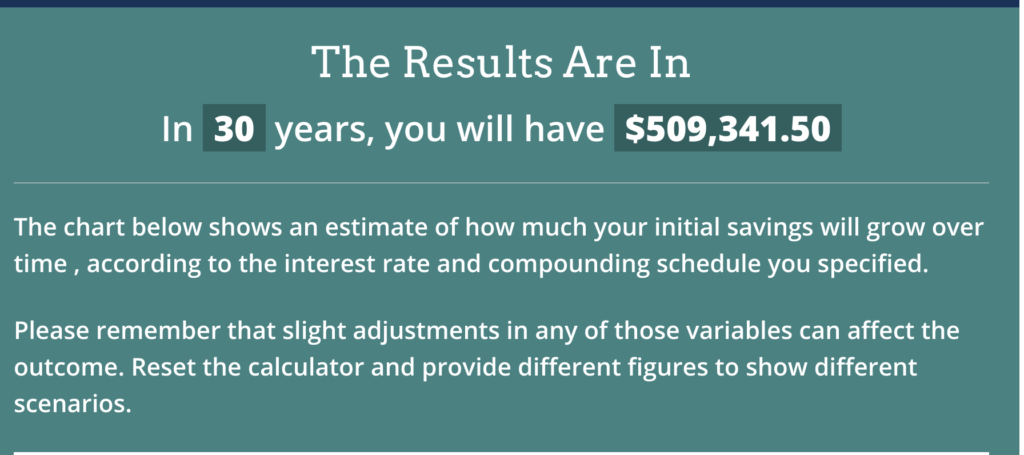

Now, let’s invest that $719 into my favorite index fund over five years. We will then let it sit in our account for another 30 years. After five years, we will have $50,617. Now, let’s just sit it in our brokerage account for another 30 years at an 8% interest rate.

Without adding a single penny, just leaving our $50,000 in our account will yield $500,000+. So what is the actual cost of buying these liabilities? As average people, we can still do what the rich do and invest like the rich invest. We have to see the long-term benefits of this approach to life.

Now, how do we start building our mindset to that of an investor and lifelong learner? There are two mindsets, and we need to understand them before we jump into creating passive income. The book “Mindset” tells us that the two mindsets are Fixed and Growth.

Why I’m Bullish on Chainlink

A fixed mindset tells us we are born the way we are, and nothing can change us. No amount of work ethic or education can make us more intelligent or more successful. A fixed mindset convinces us that we will never be rich or achieve financial freedom as an average person.

A growth mindset knows that learning is part of life. More importantly, a growth mindset understands that failure and mistakes are part of the learning process. This understanding is vital because as we build income streams, everything will not always be perfect.

For example, throughout my 52-Week Dividend challenge, I made some mistakes. I bought some companies based on emotion and lousy information. But in the end, I was up 8% and earned $400+ in dividends. Year two will be even better for my portfolio.

Happiness isn’t Free

Adopting a growth mindset is essential to being an average person with an above-average retirement. I wrote two articles about “The Succeeding in Reading.” Reading connects multiple thoughts and information from other people to form wholly original creations in our brain. The book “Limitless” tells us that reading is probably the best thing we can do for our brains.

Indeed, I would love to give you the keys to becoming an extraordinary dividend or real estate investor, but those are secondary to having a solid brain. If you want to have an above-average retirement, start reading today.

What should you be reading? Romance, mysteries, and thrillers are great, fun reads, but save those for your free time. Once you dedicate 3-4 hours a day to passive income streams, then enjoy your free time. Yes, I said 3-4 hours a day. If you don’t have time, find time during the magic hours.

Do #1. Start with dividend investing as a source of passive income and specifically investing in blue chips stocks. Once you have a nice-sized portfolio, you can even learn how to sell covered calls to earn more passive income on top of your dividends.

Diversify Your Passive Income

Do #2. Understand that real estate is a mindset. If you can understand how real estate works, you will not need many properties to change your life. Renting out a shed for $300 is enough to fund your dividend portfolio. It is the little things that give us the biggest return on our investment.

Do #3. Read and build passive income from decentralized finance. DeFi is growing every day, and having an above-average retirement, we need to jump into cryptocurrencies as soon as possible. Reading ensures we do our due diligence and move in the right direction—primarily since crypto is known to be directionless.

Do #4. Begin building royalties from our creations. Everyone is good at something or knows a rare niche. Starting a blog, YouTube channel, or writing ebooks is essential for earning royalties and building a passive income.

Is Rental Income the Best Passive Income?

Do #5. Take something we love and create an automated business. If you love sewing or knitting, you can turn that into an automated business. You create an online course about your sewing habits, tie it to your blog, create a landing page, and let the automation do the rest.

An email goes out with the code for your course, they go through the class, and you get paid. Once you set the systems in motion, you just keep creating more content. If people can make millions of dollars playing video games online, surely we can make $1,000/month doing what we love.

What limiting beliefs do you have about money? Everything I listed above is not difficult. If I can teach myself to write and design, you can too. However, if you feel you will always be average or poor, nothing can assist you.

You are what you believe. My wife and I will have a million dollars in our dividend portfolio before I turn 50. I am 40 years old now, and we have $190,000. I do not doubt our ability to achieve this goal. We just keep working towards it with routine checks, dividends, royalties, and rent payments.

Dividends vs. Royalties part II

What is your goal? More importantly, why do you NEED to achieve this goal? What is your rich life? Start there if you cannot envision your future with lots of time, family, and money.

The average person doesn’t see a future of being wealthy, and guess what? They are right. If you can see that bright future, you will not buy liabilities, stop toxic consumerism, and start working towards a happy cash flow retirement.

Conclusion. Mindset is everything for your retirement. If you are average and want to stay average, keep doing what you are doing. If you want to be above average, do something different. Try renting a room, buying dividend stocks, investing in USDC, funding a Roth IRA, writing an ebook, starting a hot dog stand, etc.

Doing any of these things is progress. Working a job is average. Buying liabilities is below average. Becoming debt-free and building passive income is above-average. You can do the math from there.

- Build Passive Income: 21 Passive Income Ideas (book)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself (book)

- Retirement Planning: Don’t Gamble with Retirement 4 (Free PDF)

- Investing: The Pros and Cons of Dividend ETFs (Free PDF)

- Cryptocurrencies: The Magic of Cryptocurrencies (Free PDF)

- Real Estate: Real Estate is a Mindset (Intermediate) (Free PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free PDF)

- Everything!: The Biggest Book on Passive Income Ever! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Sign up to Access our “Hidden” Free Kindle Book Schedule

- My first Children’s book: A Child’s First Book on Passive Income (book)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

- Writing: Can Grammarly Make You a Better Writer? (direct)

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Amazon Author Page: Check out my author page on Amazon

- Monthly Dividend Planner: Check it out on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply