Man, do I love dividends. But do you know what I love just as much as dividends? Ensuring that my capital (money) is also growing along with the stock market. When you invest for dividends, capital appreciation is a secondary requirement for your stocks.

In English, when I buy dividend stocks, I am looking for them first to pay me, and second to grow in value. However, in my opinion, I still want my overall portfolio to continue to appreciate. To ensure that my portfolio keeps up with inflation and continues to appreciate, I use index funds as its growth element.

What are index funds? Index funds are electronic traded funds (which are baskets of stocks) correlated (tied) to a specific index. For example, if I created an index called the “A” stocks that contained Apple, AT&T, and Abbvie, I could make an index fund tied to the “A” stocks index.

Dividends vs. Capital Gains

Because the index fund is tied directly to an index, it requires very little management, thus costing very little in expenses. Expenses can add up very quickly, so index funds are a great way to invest while saving your capital from expenses.

Investing strategy. Many, many people ONLY invest in index funds. It is damn near impossible to lose money in the long run with index funds. The stock market has never lost money over a specific twenty-year period. Thus, if you invest in stock market index funds, you will attach yourself to these same gains.

The problem with index fund investing. There is a problem with index fund investing, at least in my opinion. People who invest in index funds for the duration of their lives will have to sell their index funds to extract value from them.

Index funds pay very little in the form of dividends, yielding 1-2%. So, if I had $1 million of index funds, that would equal $10,000-$20,000 of dividend income per year. Of course, the value of my index portfolio would grow, but I would need to sell some securities to obtain income.

Introduction to REITs part IV: REITs vs. Rentals

Also, investing in dividend-paying stocks has perks like dividend growth, capital appreciation, mergers, dividend raises, and compounding of dividends. I love to combine these methods of investing. In fact, I wrote two entire articles about my combined approach, “Stock Marketing Investing 103” and “Investing for Dividends 104.”

Why I love index funds. I love index funds because they are drop-dead simple. You cannot, I repeat, cannot miss these things up. You find the index funds you like, and you add money to them every week and every month. That’s it. For the most part, you reinvest the dividends that they pay you and keep doing that for the rest of your life.

Another reason I love index funds is that I use them to supplement the gains of my high-yield dividend investments. For example, I love to invest in closed-end funds—which are not known for their capital appreciation.

So, I can purchase a ton of Pimco Dynamic Fund (PCI) knowing that it will not appreciate. Therefore I can add an equal amount of my favorite index fund and get capital appreciation.

Investing for Dividends 102: Keeping Score

If I had $10,000 to invest, I would put $5,000 in PCI and $5,000 in VTI (more on this later). PCI would give me a 10% dividend yield, and VTI would give me roughly 10% capital appreciation. So, I would have a 5% dividend yield and a 5% capital appreciation. I would be getting solid returns and will be paid close to $45-50/month. Not bad at all—this is my overall investing strategy.

I start my dividend portfolio with high-yield products such as REITs, Preferred Shares, and Closed-End funds. Then I layer in Dividend Growth stocks, otherwise known as blue-chip stocks. Finally, I add in my favorite index funds to ensure I am capturing the growth of the overall markets.

But Josh, what the heck is your favorite index fund!? Okay, okay—sorry. I like to give the full context before I get into the details. I have four index funds that I have in almost all of my portfolio. My top index fund is usually the top holding in all of my portfolios. Let’s take a look.

Municipal Bonds: Tax-Free Goodness

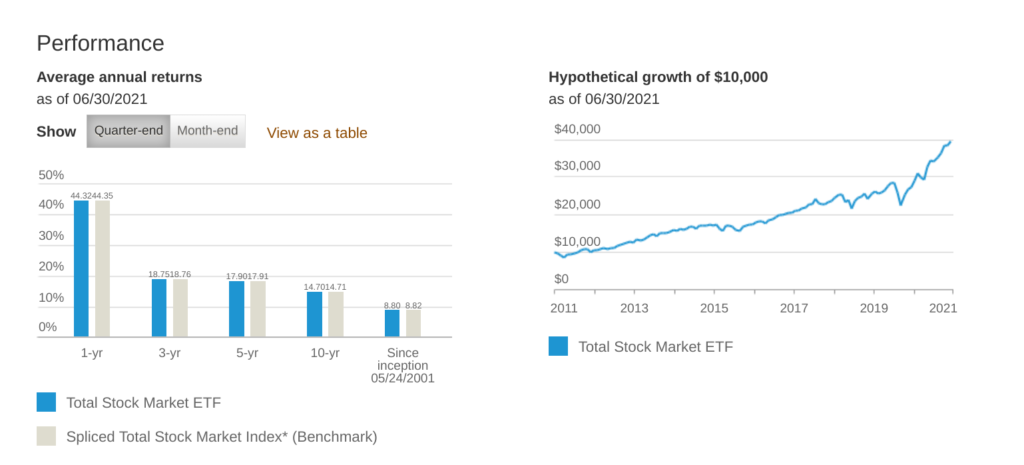

#1) My favorite index fund is Vanguard Total Stock Market Index Fund ETF or VTI. I absolutely adore this index fund because it has served me well since I started dividend investing. I would consider this index fund my best friend. It is tough to mess up your total portfolio if you have an allotment of this index fund around.

Look at the gains that VTI has made overall since its inception. Keep in mind that you want to buy as much VTI as possible when the market is down. That is why, in your portfolio, you would have gained so much more over time. Whenever I hear the stock market drop 2-3%, I am “all in” on buying VTI. It’s a no-brainer. Let’s take a look at the combination of VTI and PCI that I talked about earlier.

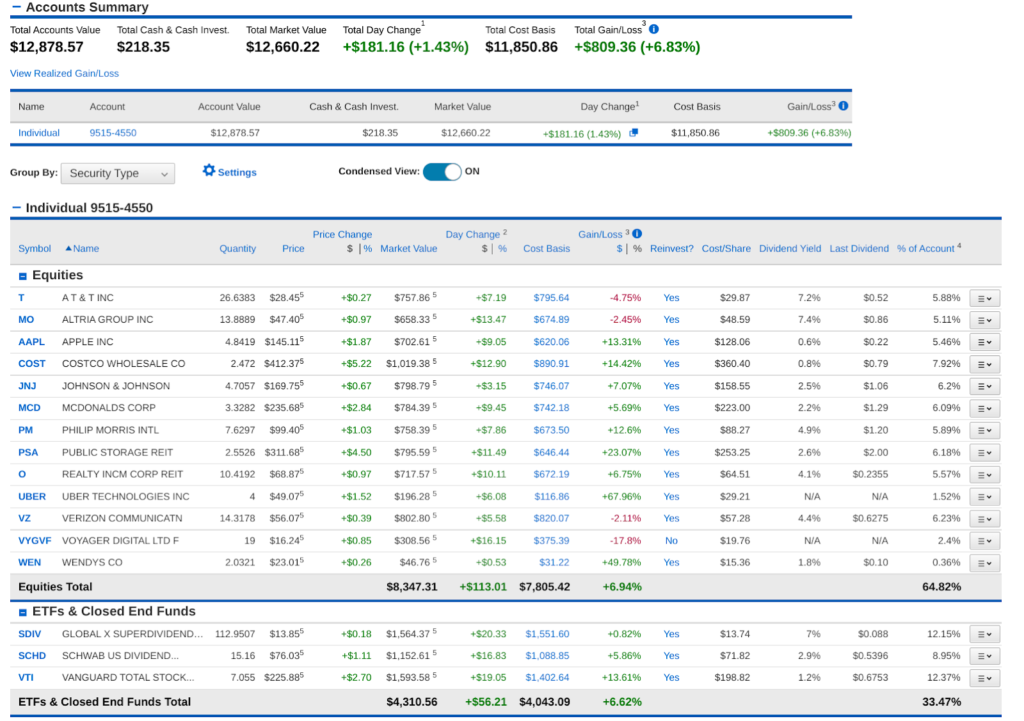

You can clearly see that the lion’s share of growth (16%) comes from VTI and the lion’s share of income ($610) comes from PCI. So, I am getting good returns and an excellent monthly income average of $55. I couldn’t ask for more.

I am a simple investor. I just want to look at my overall portfolio, see that it is doing well, and have it produce a high income in the form of dividends. When I first started dividend investing, I didn’t use a growth element at all. It was a nightmare. I want to share in the returns of the stock market and get paid while doing so. Is that too much to ask? Let look at a couple of other examples of how I use VTI.

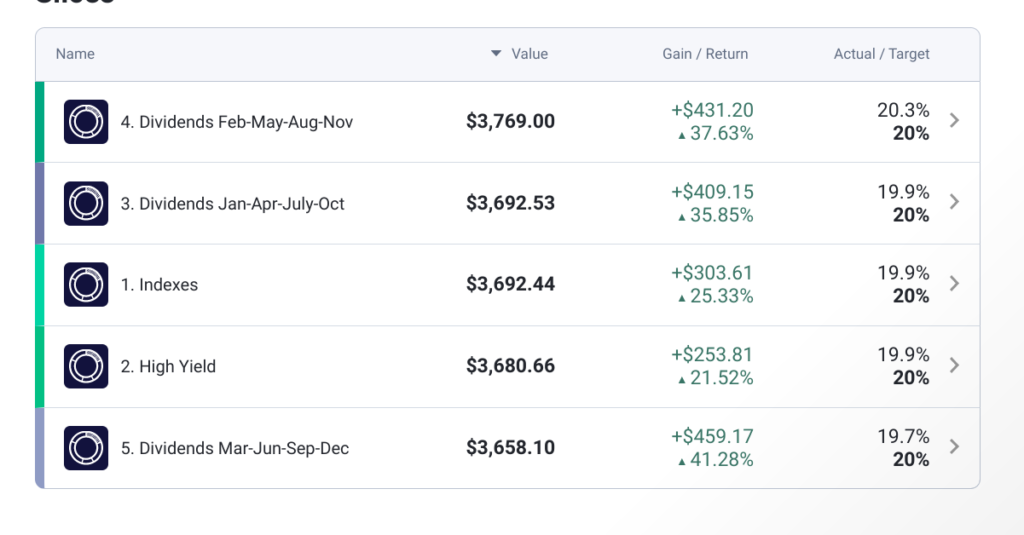

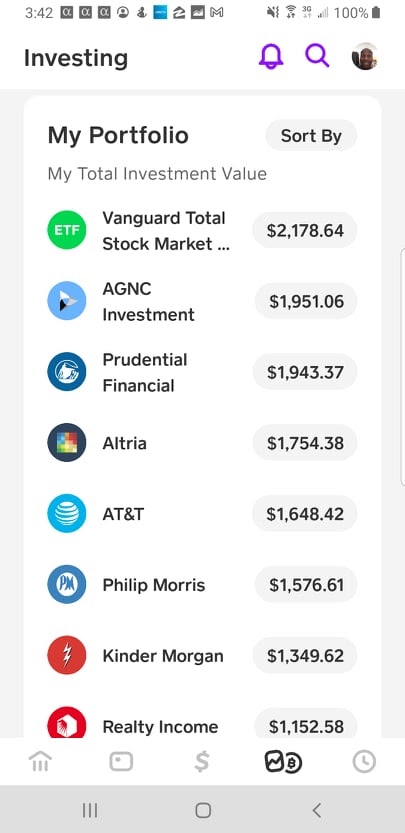

You can see VTI at the very bottom, accounting for almost 13% of my portfolio. My Charles Schwab portfolio is what I call my blue-chip growth portfolio. However, VTI has a prominent role in it. Let’s look at my M1 Finance account.

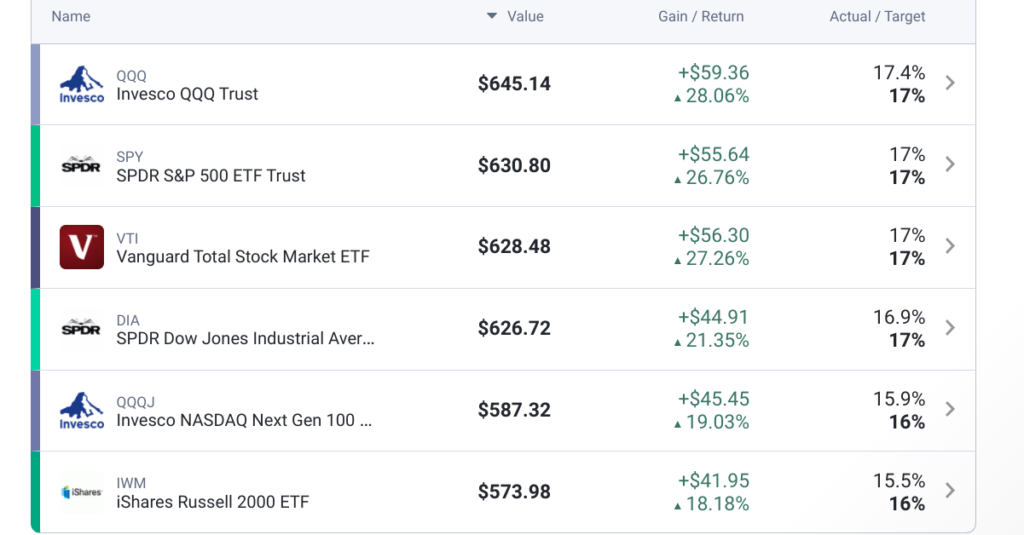

You can see that I have a different pie just for index funds as my growth element. Looking inside my index pie, you see my favorite index fund VTI, along with my other favorites, Dow Jones Industrial Index (DIA), S&P 500 (SPY), and Nasdaq (QQQ). Finally, let’s look at my Cash App.

And there you see my baby at the very top. Again, VTI has served me well in all my accounts and allowed my dividends to flourish and still retain market gains. My final account, STASH, has the same story.

Conclusion. That about wraps it up. I wanted to give a quick insight into my favorite index fund and probably my top three securities in total. I would not start any account without VTI. It is simple, and it does the job well. When the stock market has a good day, you are guaranteed to have a good day if you have enough VTI. It’s even better when you receive a $33 dividend, as I did today. Enjoy and Happy Investing!

Free PDF Downloads: Download FREE PDF books here

Financial Mindset: Become CEO of Yourself (book)

Retirement Planning: Retirement Planning at Any Age (book)

Investing: How We Plan to Retire on Dividends (book)

Cryptocurrencies: My First Book on Cryptocurrencies (book)

Real Estate: Financial Independence through Real Estate (book)

Business: Retire Rich, Retire Comfortable with a Business (book)

Everything plus way more: The Biggest Book on Passive Income Ever! (book)

Read My Books for Free: Free Kindle Books Schedule also Sign up to Access our “Hidden” Free Kindle Book Schedule where I release 15-20 more free books a week.

Follow us on our Facebook Page (here). Join our Facebook group (here)

20 Books that Will Make You Rich (here) part 2 (here)

Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply