I want 30-year bonds that yield over 6%. Unfortunately, I must look beyond 30-year Treasury Bonds, which currently pay 4.5%.

But where do I look? How do I find high-yield bonds that are also reliable and low-risk? It’s time to venture into the world of corporate bonds.

I’m new to the world of corporate bonds, so you will be able to follow me along my journey of discovery. There is a lot to learn, so let’s dive right in. Also, look at other entries in my Investing for Interest series.

- Investing for Interest 101: What is Fixed Income?

- Investing for Interest 102: Super Safe Savers

- Investing for Interest 103: Treasure in Treasuries

- Investing for Interest 104: Bountiful Bond Funds

- Investing for Interest 105: The Hunt for Baby Bonds

- Investing for Interest 106: My Favorite High-Yield Savings Account

- Investing for Interest 107: Series “I” Bonds for You and I

- Investing for Interest 108: The Magic of CD Ladders

- Investing for Interest 109: Series “I” vs. 30-Year Bonds

- Investing for Interest 110: Bond Buying is Back, Baby!

- Investing for Interest 111: CD Ladders vs. Treasury Ladders

- Investing for Interest 112: Series “I” Bonds vs. Series “EE” Bonds

- Investing for Interest 113: Baby Bonds vs. Treasury Bonds

- Investing for Interest 114: Individual Treasury Bonds vs. Treasury Bond Funds

- Investing for Interest 115: Tips for Buying T.I.P.S.

- Investing for Interest 116: Series “I” Bonds vs. T.I.P.S.

- Investing for Interest 117: Treasury Bills vs. Notes vs. Bonds

- Investing for Interest 118: The Magic of Money Market Funds

What are corporate bonds? Corporate bonds are bonds that corporations issue to generate money from investors. Corporations use bonds when they can leverage investor money more cheaply than borrowing from a bank.

Let’s review the chain of risk for bonds: treasury bonds, mortgage-backed securities, municipal bonds, and then corporate bonds. Why is the chain of risk important? Because you’ll receive a higher yield as you take more risk.

Investors consider treasury bonds to carry no risk; they carry the full weight of the US government. Corporate bonds carry default risk, which contributes to their grading.

Therefore, two factors determine corporate bond yields: the prevailing interest rate and the company’s default risk. This allows us to find good deals on the bond market.

Purchasing corporate bonds. I have not yet purchased corporate bonds from Charles Schwab, as the minimum is usually $10,000. However, I am working up to buying some over the next year.

First, you must find corporate bonds that you can then search for on the bond market. The bond market is much larger than the stock market, but it can be more challenging for retail buyers like us to navigate.

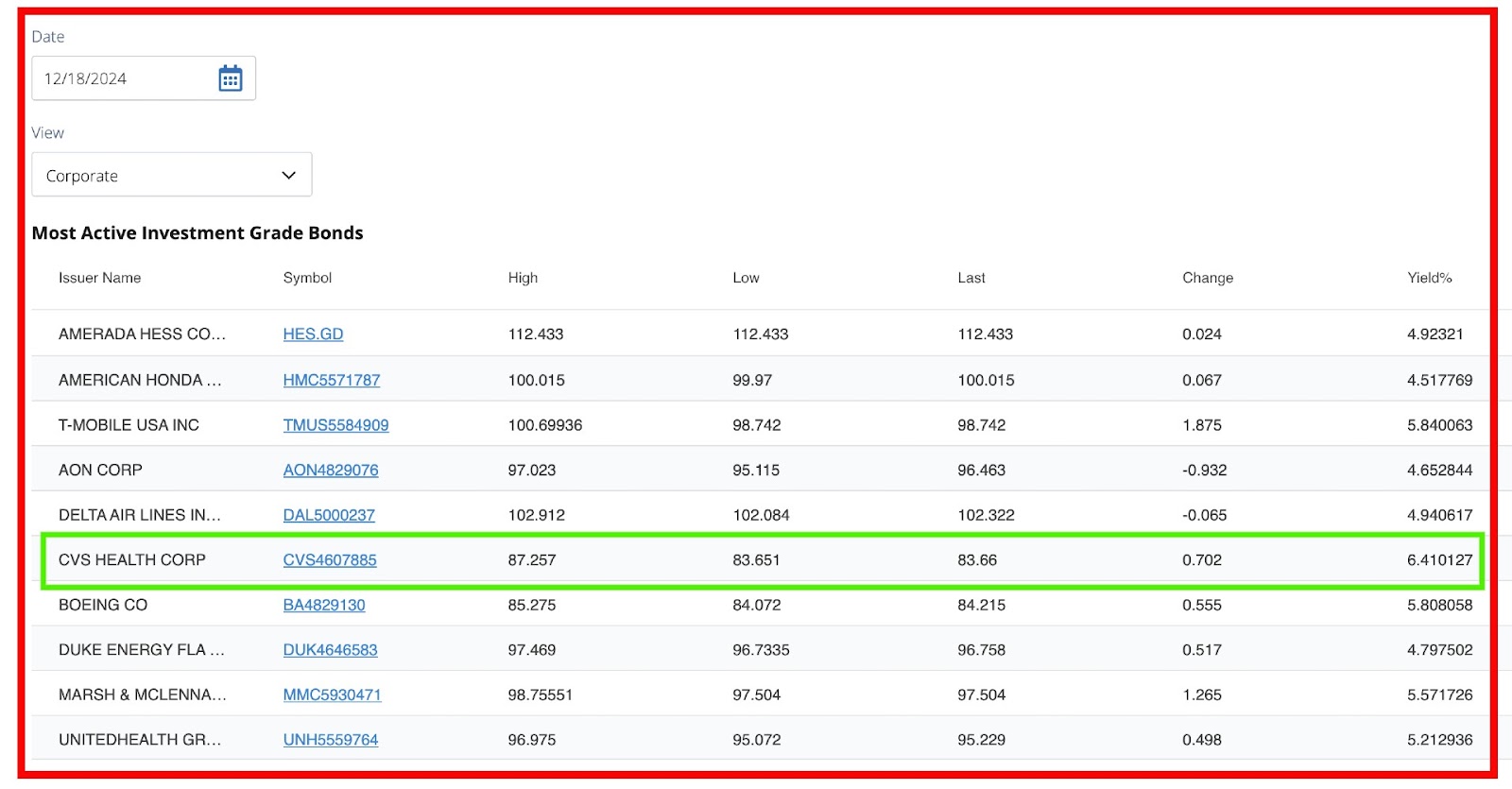

I started my search using “Most Active Corporate Bonds” on the Firna.org website. Right away, the CVS bonds yielding 6.41% caught my eye. I have never seen anything sexier!

I love CVS and own its stock. I would love to purchase these CVS bonds for Christmas, so now it’s time to take a deeper look at what they offer.

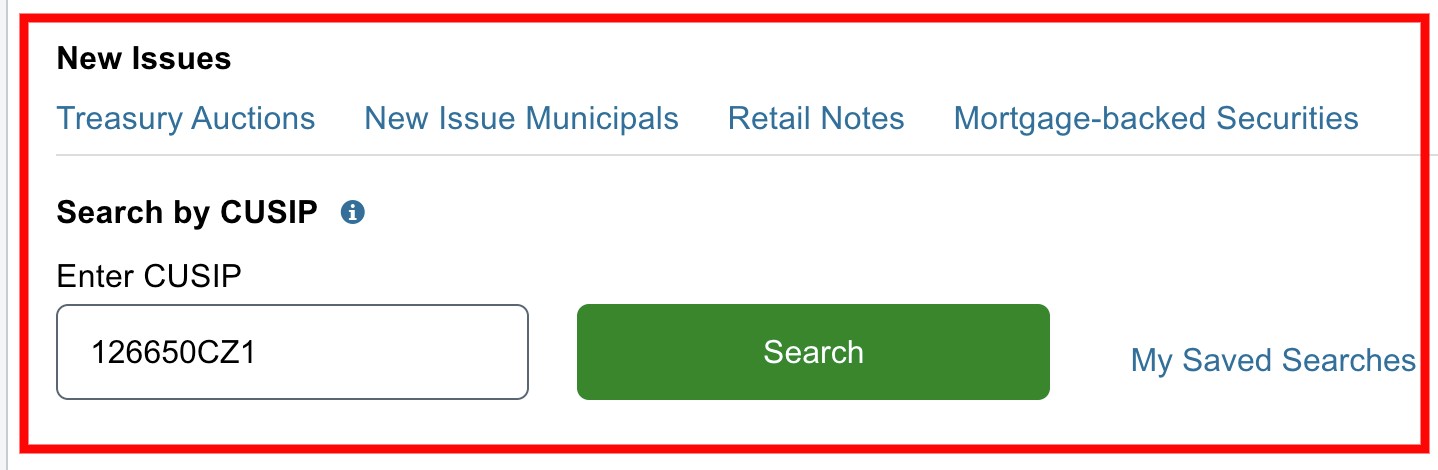

You can click on the CVS bonds to view more yield and price history data. I love reviewing stuff like this, don’t you? We will need the CUSIP to review the bonds on Charles Schwab.

In July 2020, the price of the CVS bonds was $140, and their yield was 2.9%. Today, the price is $85, and the yield is 6.2%. CVS is having a hard time in real life, so the bonds are suffering—along with prevailing interest rates increasing to 4.25%.

I use Charles Schwab to search for my bonds. To access the bond market, you will need to read some warnings and disclaimers.

Now, I can enter the CUSIP on Charles Schwab to pull up purchasing data on the CVS bonds. This brings up even more data on the bonds, including the minimum and maximum bonds you can buy from this CUSIP.

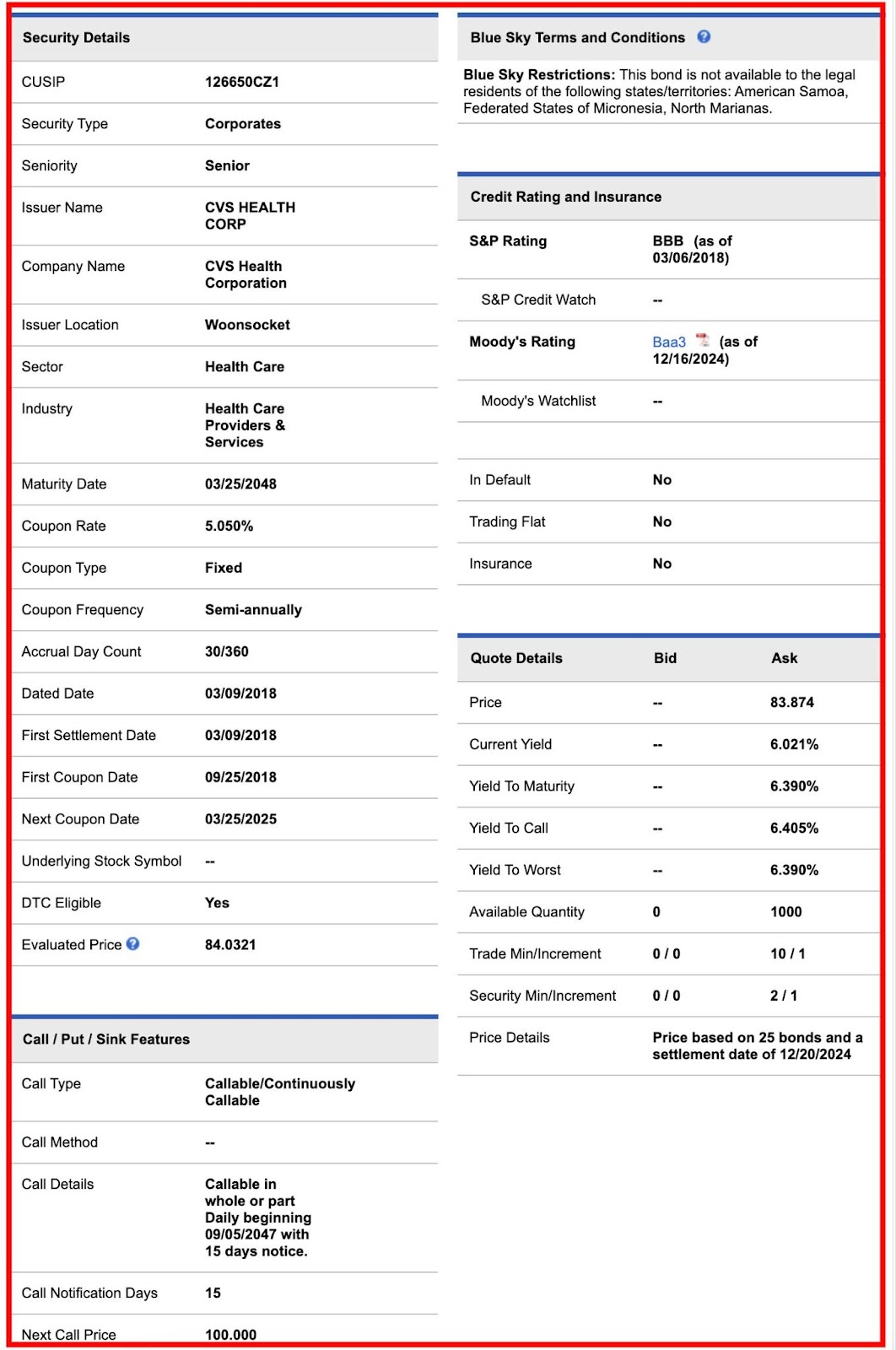

You can click on the CVS bonds on Charles Schwab to see even more data, such as that they are senior bonds.

The seniority of the bonds is vital to understanding their position on the capital structure if the company should fold. For reference, company shares (equity) are the lowest on the totem pole.

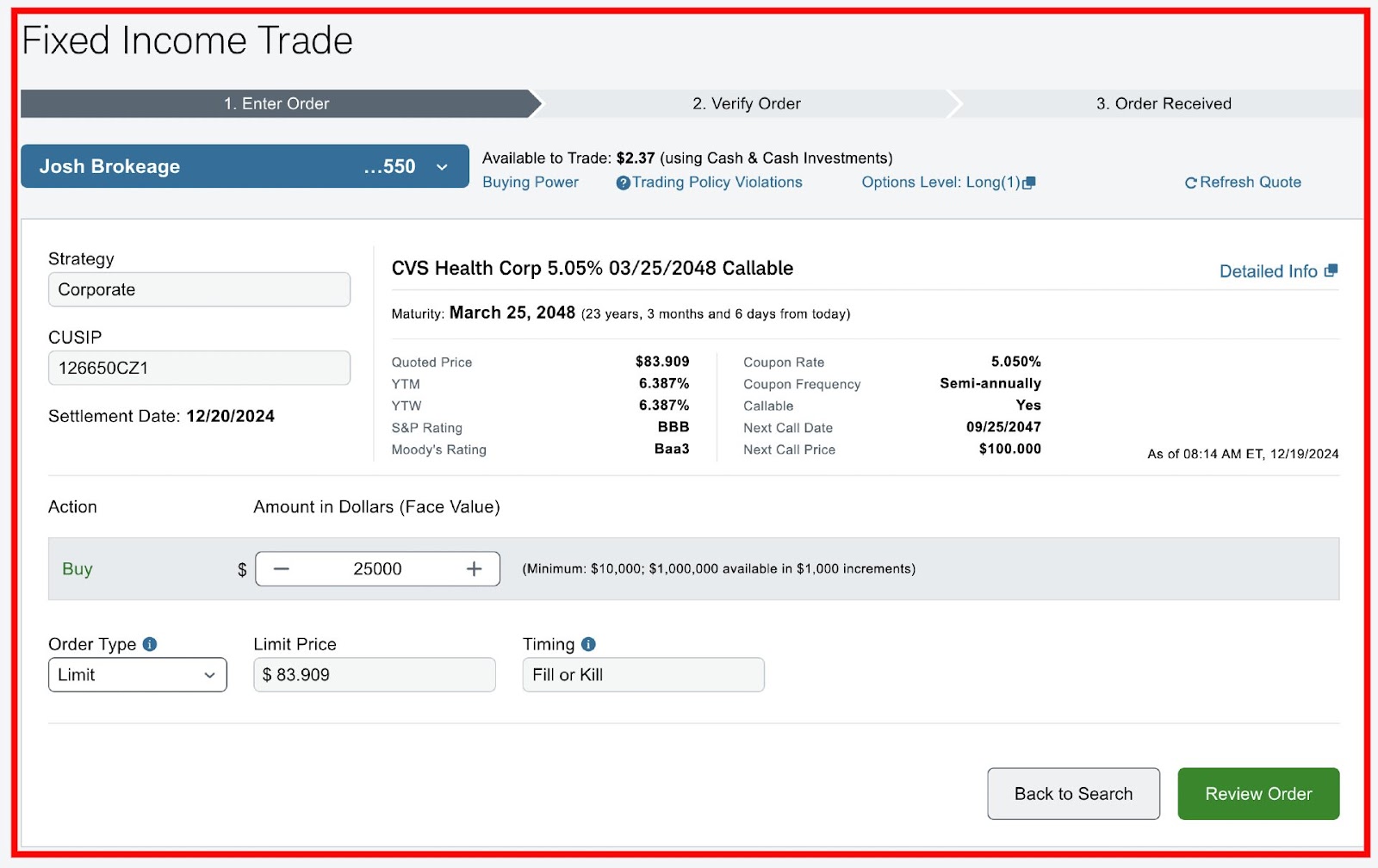

Clicking the buy button makes my heart break. As you can see, the minimum purchase is $10,000, and increments of $1,000 are available. Man, I wish I had $10,000 to spare. However, I promise to purchase some corporate bonds in 2025.

The magic of corporate bonds. For the CVS bonds, I would collect 6.4% interest for over 23 years. How amazing is that?

Let’s say I invested $10,000. I would collect $640 in annual interest payments, totaling $14,720. Also, remember that I am paying $84 per bond instead of $100.

However, CVS would reimburse me at $100 per bond. If I purchased 12 bonds for $10,000, they would reimburse me $12,000.

The magic of corporate bonds is that you can find higher yields than treasuries and lock them in for a generation. You also get to invest in your favorite corporations.

You can experience known capital appreciation and high yields. I want to purchase a corporate bond every year; it should become easier as time passes.

You can also leverage high-yield bond reinvestment to maximize your bond growth investing. For example, you can use interest payments to purchase high-yield bond closed-end funds from PIMCO (PDI) that generate 12% returns.

I find it simply amazing to jump into the world of corporate bonds. Learning more about these bond purchases will be my task for 2025.

There are other ways to purchase corporate bonds. If $10,000 is too steep, there are different methods. Each method has its pros and cons.

Corporate Bond ETFs– There are many corporate bond ETFs that do not use leverage. One of the biggest is the Vanguard Intermediate-Term Corporate Bond ETF (VCIT), which currently yields 4.24%.

I am not a fan of the yield; however, bond funds are very liquid. This means you can maneuver in and out of these products on a whim. But it removes the fun of searching for individual companies and CUSIPs.

Preferred Shares– I love preferred shares because they are a combination of fixed income and equity. They trade on the stock market but act as fixed-income products. Plus, they typically have a $25 face value.

CVS doesn’t have preferred shares, but companies like JP Morgan (JPM), Public Storage (PSA), and Wells Fargo (WFC) do. Preferred shares are considered dividend income, and some even offer qualified dividends.

Baby Bonds– Baby bonds look and act like preferred shares; however, they sit higher on the capital stack. They also pay interest income, which is usually more costly than dividend income.

Bond closed-end funds– I trust the best bond managers in the world to manage my bond funds. My favorite manager is PIMCO, and I purchase their bond closed-end funds (PDI, PTY, PDO).

They offer high yields and consistent monthly income. However, the price can fluctuate wildly due to prevailing interest rates and the use of leverage.

Conclusion. I am ready to get my hands dirty and purchase corporate bonds directly at the source. I don’t have $10,000 lying around, but I will make it a point to buy a stack of corporate bonds in 2025.

Corporate bonds offer more security than individual stocks, with some known price appreciation. My main concern is getting a high yield from a trustworthy company like CVS.

The world of corporate bonds is massive, and I am just dipping my toe into the abyss. I have already learned a lot and can’t wait to add more diversity to my high-yield income portfolio.

There is nothing quite like high-yield income investing. Turning my money into more money is always fun. Corporate bonds offer high yields over a long time—what more can you ask for? Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply