It’s an exciting time to be a bond investor. The Federal Reserve raised interest rates to help combat the high inflation that is running rampant throughout the country.

I have always said that I am a buyer of 30-year Treasury Bonds that yield over 4%. Lucky for me, now is the best period for purchasing bonds in the last 15 years.

But why invest in Treasury bonds over dividend stocks? Is the 60/40 portfolio consisting of stocks and bonds still a viable investing methodology?

How to Raise Financially Intelligent Kids

To answer these questions (and more), let’s review the importance of obtaining guaranteed fixed income over 30 years and what that means to your investing success. Let’s begin!

The importance of US Treasuries. US Treasuries represent a risk-free investment guaranteed by the full might of the US government. Since Treasuries are risk-free, we can weigh all over investments against them.

There is one caveat: they are only risk-free if you hold until maturity. Therefore, buying 30-year Treasury bonds carries significant risk if you look to sell before 30 years.

Bonds trade on the open bond market, several times larger than the stock market. You can purchase a 30-year Treasury bond directly from the US government.

Thanksgiving: A Time for Grace & Passive Income

However, investors bid up or down the price of your bond. Therefore, it may have a coupon of 4.5%, but your effective yield could be, for example, 4.8% or 4.2%, depending on your price.

All this is to say that you can sell your bonds for a profit when your coupon is much higher than current rates—your bonds can appreciate in value.

The world of selling and buying bonds on the open market is challenging. I read “The Bond Book,” and the author even recommends holding bonds until maturity because of how difficult it is to trade bonds.

Holding 30-year bonds for 30 years. I intend to keep my 30-year Treasury bonds for 30 years. Now that yields are significantly above 4%, I am in love with investing in Treasury Bonds.

Five Takeaways from “Rich Kid Smart Kid”

Let’s compare 30-year Treasury bonds against other fixed-income and equity investments. This is how we can truly see the value in bonds.

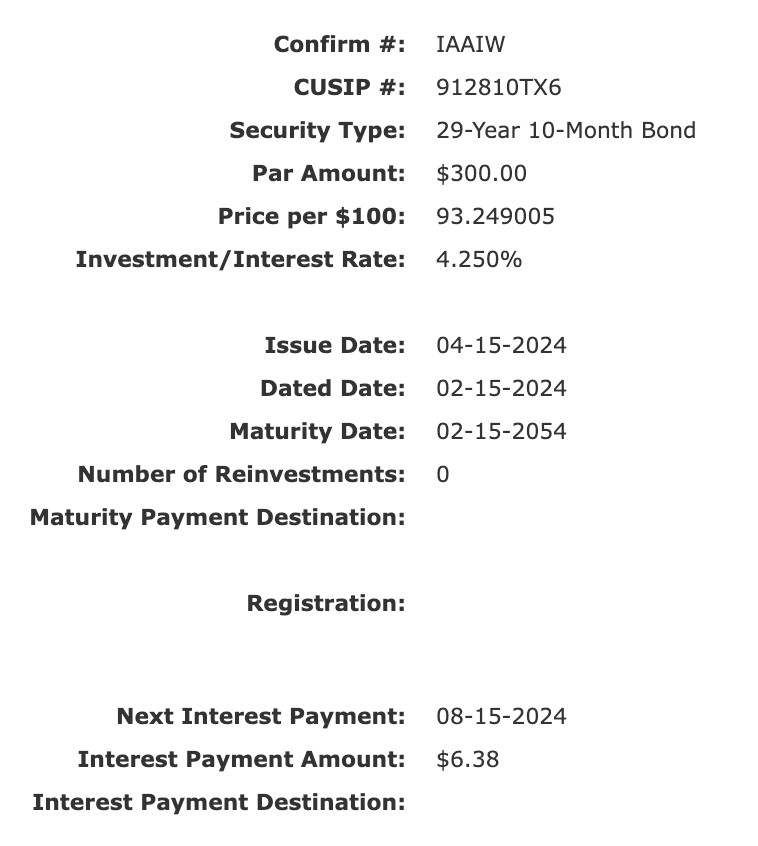

First, let’s take a look at the most recent 30-year Bond I purchased from Treasurydirect. I bought a $300 bond for $281. The coupon is 4.25%. My effective yield is roughly 4.7%.

I just locked in a risk-free 4.7% yield for 30 years—someone, please give this man a round of applause. Because this is a fixed-income bond, I can see how much money this bond will pay me throughout its existence.

Each semi-annual interest payment will be $6.38, for a total of $12.76 annually. Over 30 years, the bond will pay me $382.80, and then I will receive my initial $300 back. This gives me a total of $682.80 at the end.

Spicy Dividends for a Bland Life

You will be hard-pressed to find a decent certificate of deposit over five years in length. Banks take all the risk on CDs, and CDs don’t trade on the open market. Therefore, banks must be careful not to lock in long-term high-interest rates on their CDs.

Interest rates on high-yield savings accounts can disappear like leaves in autumn. However, you store money in HYSAs as part of your emergency fund, not necessarily to make a large profit.

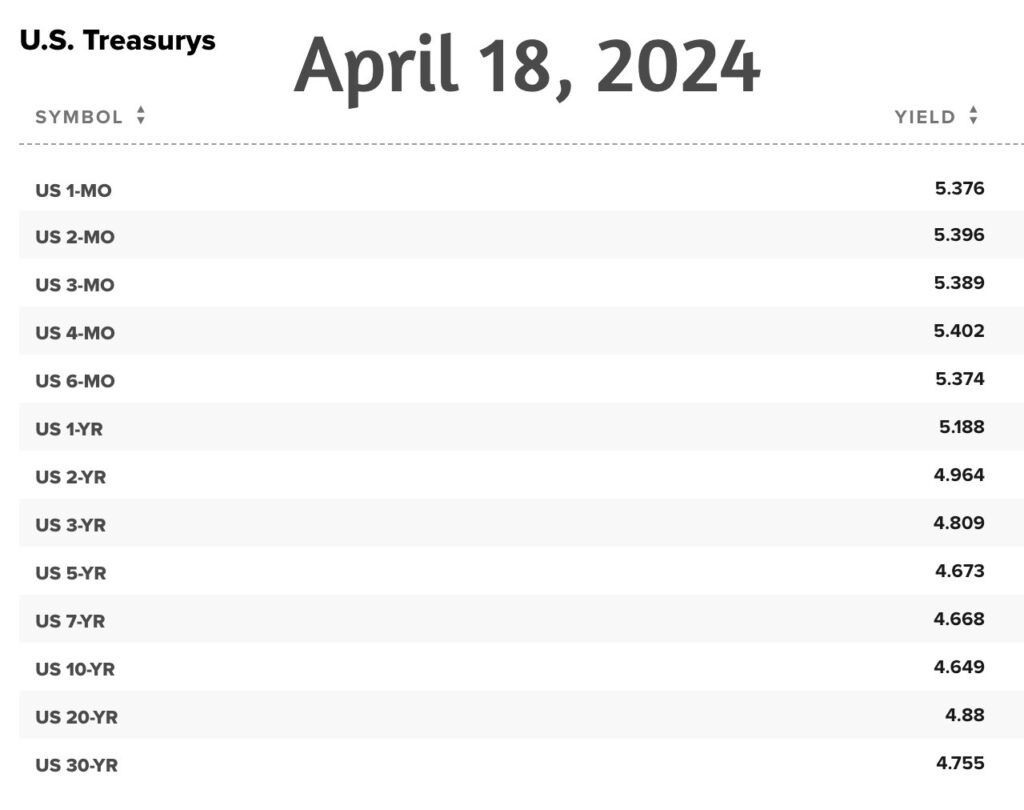

Yields on short-term Treasury Bills and Notes can be higher than the 30-year in what we call an inverted yield curve. However, there is no guarantee that your 5.3% one-month Treasury BIll will reset at such a high rate.

Some great dividend stocks yield 4.7% or higher. I can think of AT&T (T) and Verizon (VZ) off the top of my head. These stocks also offer the chance to appreciate some over the next 30 years.

Tired of Being Broke, Behind, and Bullied?

However, most stocks offering yields above 4.7% are mature companies like utilities and telecommunications. Most young or growth stocks offer much lower yields.

Stock vs. Bonds. It’s a good idea to have stocks and bonds, even if not in a traditional 60/40 portfolio. Being able to purchase bonds over 4% and invest in stocks over 4% is a blessing.

As interest rates decrease, investors will move toward high-yielding dividend stocks; remember, investors seek yield. T and VZ may begin to yield much less as investors bid up their prices.

Also, as rate increases decrease, the price of your bonds may increase. A bond’s par value is 100. Your 4.2% coupon bond may sell for 110 if the Federal Funds rate is lower than 3%.

Growth stocks tend to increase in value as money becomes cheaper. This means they can borrow more to expand faster. The takeaway is that it is a good idea to be a well-rounded investor who understands the effect of interest rates on all types of investments.

The Options Trading Debit Card

Why long-term bonds. But why do I like 30-year bonds over, say, five or ten-year Treasury Notes? I like locking in a good deal for as long as possible.

Long-term inflation is around 2.5%. Although the federal government taxes the interest on my bonds, I will still beat inflation by a little.

I can destroy inflation by using high-yield bond reinvestment as a strategy. This means I would take my $6.38 compound payments and invest in high-yield products like closed-end funds and preferred shares.

That means my $300 principal will stay safe, and I would invest my $382 in coupon payments at rates over 10%. My $382 could produce well above $38 per year in dividends for the rest of my life.

Building Generational Wealth Via Real Estate

Investing in bonds requires strategy. The goal is to protect your principal while smartly reinvesting your interest payments.

When you invest in stocks, your principal is not guaranteed—you are 100% at the whims of the stock market. This is something to consider as you evaluate your risk tolerance.

My bond strategy. My current bond strategy is to purchase $50 in Series “I” Bonds and $300 in 30-year Treasury Bonds monthly.

I will continue to purchase 30-year Bonds as long as they stay above 4%. If they fall below 4%, I will re-evaluate my strategy versus the current environment.

The Pros & Cons of Homeownership #3

I love investing in dividends, but bonds are also an important part of my investment strategy. They are somewhere between my emergency fund and my dividend portfolio, a place to protect and grow money.

Conclusion. Many people do not invest in 30-year Bonds because of the high duration risk. This means they can gain or lose value due to current interest rates.

I take a simple approach; long-term inflation rates are around 2.5%. Investing in bonds above 4% will help me stay current with inflation.

It’s Time to Purchase a Certificate of Deposit

I have other ways to beat inflation; however, protecting principal is always vital to at least some of my portfolio. Investing is a highly personal affair, as only you know your risk tolerance.

Current bond yields are an enticing entry point into the bond market. The Federal Reserve plans to lower rates by the end of 2024.

Inflation is proving to be more sticky than we believed, so rates may not lower this year. Either way, I will enjoy my 4% 30-year Treasury Bonds for a long time. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply