Inflation comes for all of us; how we deal with it determines our financial success in life. I like to say that inflation is the cost of being alive.

There are many ways to outpace inflation (dividend investing, real estate, cryptocurrencies, business), but you must balance each against your goals, dreams, and risk profile.

I have championed Series “I” Bonds for over four years, and my love for them still continues. However, will buying and holding Series “I” Bonds truly help you conquer inflation?

Don’t Gamble with Retirement 12

Why Series “I”? So, why have I been such a massive proponent of Series “I” Bonds from the US Treasury Department? That’s easy; Series “I” Bonds are just amazing products. They are so extraordinary that the government only allows you to purchase $10,000 annually.

The goal of Series “I” Saving Bonds is for your money to stay equal with inflation. For example, investing $50 in 1999 should equal $50 in 2029 (30 years later).

Will Series “I” Bonds help you far outpace inflation? No, that’s not their intended purpose. You have other methods to outpace inflation; however, all other methods require risk.

Series “I” Bonds are truly risk-free assets that you set up to invest straight from your checking accounts automatically. In fact, I just renewed my subscription to Series “I” Bonds for $50 per month.

The Biggest Book on Passive Income Ever 4!

I stopped my allotment to Series “I” Bonds as I went through the process of retiring from the military. Now that my retirement pay is settled, I am back investing in the things I love.

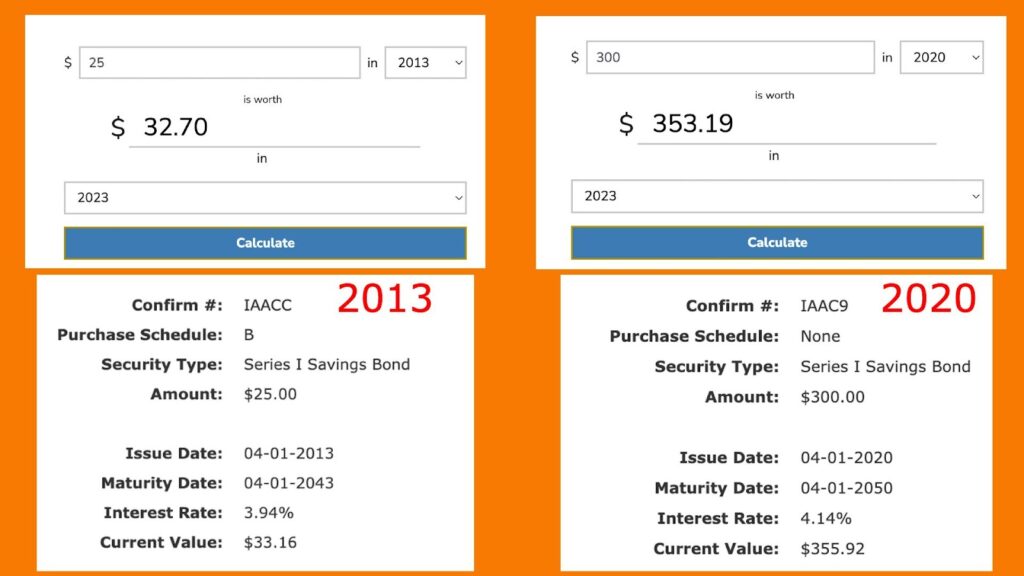

Let’s look at the facts. Luckily, I have been investing in Series “I” Bonds since 2013. Therefore, we can compare my actual bonds versus an inflation calculator from the World Wide Web. Let’s begin.

Let’s start with a $25 savings bond I bought in 2013. The inflation calculator says my $25 should be worth around $32.70. My bond is worth $33.16, not bad.

Next, let’s review a bond I bought at the start of the pandemic in April 2020. If you recall, interest rates were at their absolute lows around this time.

Dividend Stocks vs. Income Stocks

I bought a $300 Series “I” Bonds that month. The inflation calculator says that my $300 should be worth $353.19. My bond is worth $355.92. This is amazing!

As you can see, investing in Series “I” Bonds is like putting your money in a time capsule. You can preserve your wealth by investing in these bonds, but not necessarily grow your wealth.

Series “I” Bonds versus 30-year Treasury Bonds. We cannot just shove all our money into Series “I” Bonds without looking at different ways to survive inflation.

Becoming an investor means you leverage all types of products; however, you balance the good with the bad. Let’s start by looking at 30-year Treasury Bonds.

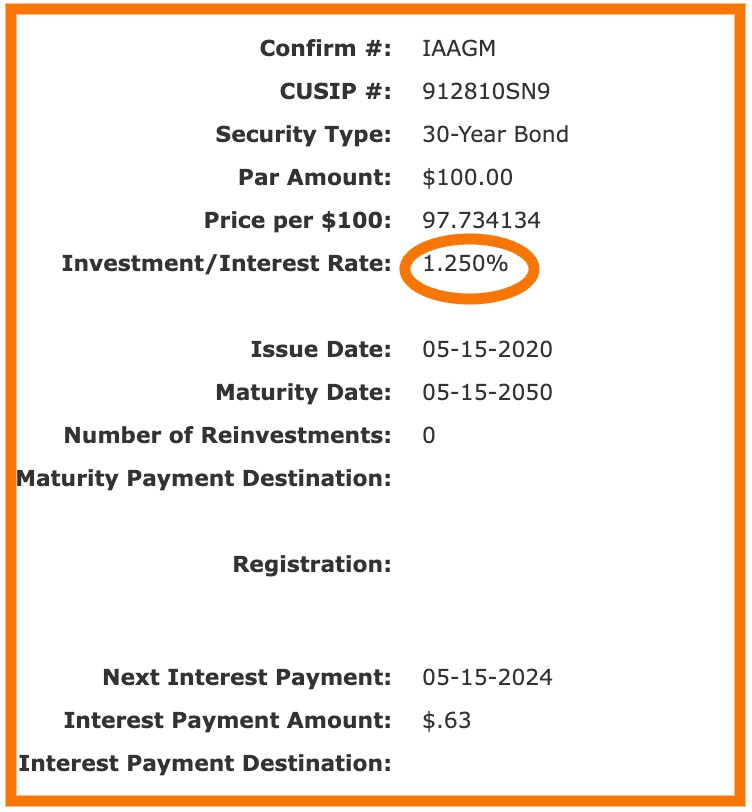

I love me some 30-year Treasury Bonds, but the ones I bought in May 2020 are worthless. Their interest rate is 1.250%, which is just pathetic. These particular bonds did not survive the inflationary spiral in 2022 and 2023.

Happy Cash Flow Retirement 12

However, if you lock in 30-year Bonds at 4% higher, they may reward you with higher returns over the next 30 years. That’s the risk with buying 30-year Bonds versus Series “I” Bonds; you must purchase 30-year Treasuries at the perfect time.

Let’s move on to index funds. Many people invest in index funds to beat inflation. The stock market, on average, returns 8-10%, which can easily trounce inflation of 3%.

I bought two shares of the SPDR S&P 500 Index Fund (SPY) in September 2020 for $353.64 each. My inflation calculator says my $353.64 should be worth $416.22, but my index funds are worth $519.41 each.

They outpaced inflation by over $100 each. However, in 2022, the S&P 500 was below the rates I purchased them for in 2020. Therefore, I would have suffered a substantial loss if I had needed the cash when the market was down.

Royalties to the Rescue

My Series “I” Bonds were never negative, even during the worst bear market in stocks and bonds. That’s their advantage over index funds. Index funds will likely trounce inflation, but they may fail you when you need them the most.

Let’s get creative. I’m going to throw in an odd comparison. Becoming creative can also help you beat inflation.

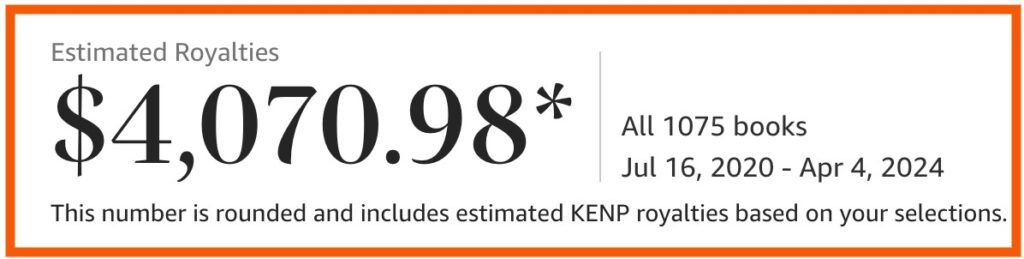

I released my first book on Amazon in January 2021 (there was a test book in June 2020). The cool part of releasing books is that it costs me little money, just the cost of purchasing services from Grammarly, Canva, and Pixlr.

Over the last three years, I have made $4,070 in book royalties on Amazon. If I invested $2000 in Series “I” Bonds in 2020, would that beat the amount from book royalties?

Even investing $2,000 in 2020 would not beat inflation as handily as my book royalties ($2,354 versus $4,070). If you don’t have a massive amount of money to invest now, starting a creative business (writing, podcasting, YouTube, or music) can pay off in spades.

Use the G.I. Bill as an Income Stream

Getting started with Series “I” Bonds. The key to investing in Series “I” Bonds for the long run is being patient and understanding the purpose of these saving bonds.

Series “I” Bonds are a place to park your money and allow it to continue to grow along with inflation. When you need these funds, the money will be worth as much as you remember when you invested it.

High-yield savings accounts can also serve as a way to keep your money growing, but there is a huge difference. The Fed dictates interest rates for banks and savings accounts; Series “I” Bonds derive rates directly from inflation numbers.

Therefore, there is a chance that inflation is high, but interest rates are low. This phenomenon happened in May 2022, when Series “I” Bond rates were 9.62% and the Federal Funds rate was 1%.

Options Trading for the Average Person

Series “I” Bonds kicked everyone’s rear ends in 2022, and I didn’t have to do anything but sit there and watch. The government adjusts your bonds’ rates automatically throughout its thirty-year run.

Here is the kicker: you don’t need to pay interest on your savings bonds until you redeem them. With high-yield savings, you’ll pay federal and state tax (unless you live in a state without it) on these accounts yearly.

You can even avoid paying taxes on Series “I” Bonds if you use them for a qualified educational purpose. How cool is that?

I Love Being Bored; I Means I Am Becoming Wealthier

Conclusion. As you can see, there is much to love about Series “I” Bonds. I am genuinely in love with these saving instruments.

I aim to max out my annual contributions ($10,000) by the time I am 53 years old (10 years from now). That would be a great way to leave a lasting impression on my family legacy.

To summarize, you don’t purchase Series “I” Bonds to destroy inflation but to prevent it from making a dent in your purchasing power.

Dividend Investing with a Splash of Options Trading

There are many ways to beat inflation; you just need to choose a few that suit your lifestyle and risk tolerance. I like to make money through writing, dividend investing, rental income, and options trading.

However, these all involve some type of financial or time risk. Series “I” Bonds allow me to sleep well at night, knowing I have money safely growing if needed.

How will you use Series “I” Bonds to diversify your portfolio? The best way to jump in is to go head first. You can start by opening a TreasuryDirect account today. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply