We all go to the stock market to achieve various results. Some of the reasons are to generate income, build wealth, and provide tax shelter through capital gains.

No matter the reason that attracts you to the world’s biggest stage, you’ll need to be intentional with your money and investing goals.

Not all stocks and funds are equal for those wanting to generate income. You must lay out your plans clearly before jumping into the world of income-producing assets. Let’s begin.

Becoming an Entrepreneur #6

Dividend stocks vs. Income stocks. Dividend stocks typically fall under the category of Dividend Growth Investing (DGI). Income stocks usually fall under the category of Income Investing. Knowing the difference will help you better meet your financial goals.

Investors use dividend growth investing to build generational wealth and create income. The process consists of buying stocks with a proven dividend growth history. As you reinvest your dividends and continue to dollar-cost average, your positions will grow quite powerful.

A great example of a dividend growth stock is Coca-Cola (KO). In 1974, the dividend was $0.01. Today it is $0.46. Along the way, the share price has continued to reach all-time highs.

After 30+ years of investing in KO, you would be sitting on a mountain of capital gains and a significant income stream. Once you retire, or earlier, you could turn off dividend reinvestment and start receiving your dividends in cold, hard cash.

Don’t Gamble with Retirement 10

Income investing is much different. Income investing seeks to put money into your pocket today by offering much higher yields. Typically, those yields come at the sacrifice of price growth.

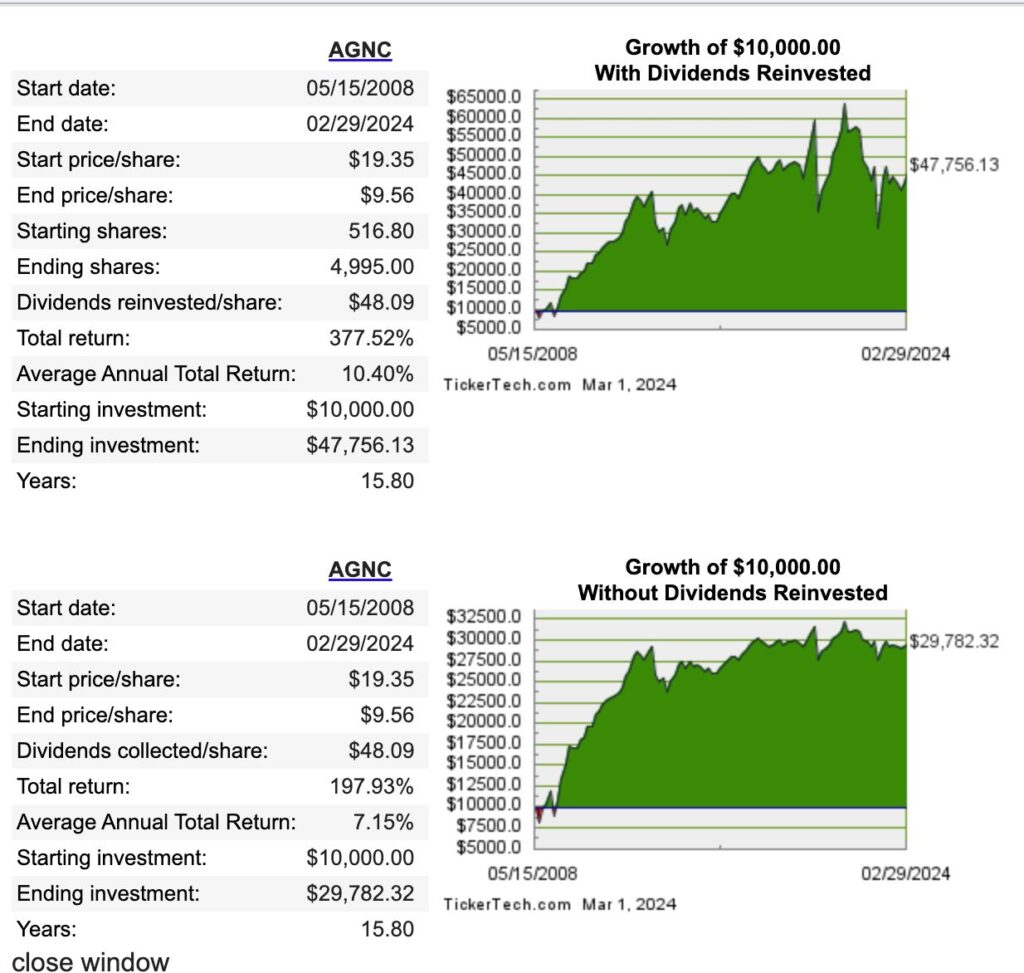

Let’s take one of my favorite high-income stocks, AGNC mortgage REIT (AGNC). From 2008 to 2024, you would have received $48 of dividends per share, starting at a purchase price of $19. Most of your gains come from dividends. Check out the dividend calculator at The Dividend Channel.

The goal of income investing is to help you get through life today. However, if you reinvest 25% or more of your dividends, you can ensure your portfolio continues to grow ahead of inflation.

Which method is right for you? I am partial to income investing for one primary reason. Put simply, we live in the real world, not in our investment portfolios.

Becoming an Entrepreneur #5

I remember trying to invest in my 401K when I was a young husband, father, and homeowner (2008). I always had to borrow against my 401K balance because life continued to happen.

In 2019, I learned about dividend investing and income investing. I started to take some of my dividends to use in real life. It felt good to take my wife to dinner on behalf of AGNC’s monthly dividend.

The most difficult part about life is changing your mindset about receiving a paycheck versus living on dividend income. Our parents and the school system train us to depend on a job and paychecks.

In truth, wealthy people generate lots of passive income from investments, including dividends. The sooner you get comfortable using your dividends, the hungrier you will become to grow your portfolio.

My wife and I currently earn about $1,600/month in dividends. We can use this money to do whatever we want because it will return to our accounts next month.

While we reinvest most of our dividends, we still have the option to spend some if we feel the urge. There is nothing quite like having more money than you can spend.

Starting income investing young. It is tough to tell a young person to purchase Visa (V), Mastercard (MA), Microsoft (MFST), or Johnson & Johnson (JNJ) and hold it for 20 years without taking dividends.

Series “I” Bonds vs. Series “EE” Bonds

In an ideal world, let’s say a young person received $12,000 as a high school graduation present. It would be a great idea to put $3,000 into each of those stocks and save them until they turn 65. However, that’s not the reality.

I currently have a small, $12,000 income portfolio with M1 Finance. It pays me roughly $120/month in dividends.

I would much rather see a young person create a portfolio like this early in life. They can then automatically transfer $25 to a dividend growth investing portfolio with the four stocks.

Also, the young person can transfer $50 per month to their checking account so they spend. $50 is enough to fill up their car or go to the movies. It’s not much, but it will help them see the benefits of living on passive income.

Treasury Notes vs. Certificates of Deposit

That would leave $45/month to reinvest into the income portfolio. Over time, the dividends would increase so the investors could increase their commitments.

Again, this is just my opinion. Chances are the person falls in love with income and dividend growth investing. This would spark something inside them to generate more revenue and continue investing. This happened to me in 2019.

Living on passive income. The most essential part of living on passive income is living on passive income. The sooner you make the mental and financial transition, the better you will be BEFORE you retire.

Too often, retirees work hard and save lots of money in their 401Ks, only to live in fear of extracting those same resources.

Over time, even as an income investor, you’ll appreciate the value of dividend growth investing. You’ll see companies, such as Facebook (META), initiate their first dividends. You will want to be a part of their dividend growth story.

Bond Investing in Your 70s

After 30 years of dividend growth investing, you stand to have a massive portfolio with significant dividends coming your way. However, dividend growth investing works best when you reinvest all dividends until retirement.

Income investing creates a paycheck for you today. One day, you will be so flush with cash flow that you must reinvest into dividend growth strokes and index funds.

My goal is to get to $80,000/year in dividend income. I will use mostly income investing to achieve this goal. From there, I can use those dividends to build DGI portfolios for my kids and grandkids.

Are We Living in Fast Forward?

Conclusion. My top reason for entering the stock market is to extract current income. I want my stocks to pay me today. Once I have the cash in hand, I can decide who I want to spend my dividends.

I have a few fairly large DGI portfolios, but my main focus is income investing. I know that cash flow makes you wealthy, so creating a sustainable lifestyle—without working—is my number one goal.

The media will try to convince you to invest heavily in your 401K. These are outstanding tax-advantaged accounts, but you will lock away your money for 30 to 40 years.

Start a Review & Content Business Toward Passive Income

During those years, life will happen. Your air conditioner will break, your house will flood, or your car will break down. Cash flow will help you get through all of these scenarios.

I lived a life where I tried to invest heavily in my 401K. Life simply beat me down so much that I had to take multiple loans against those accounts.

Once I began dividend and income investing, I used cash flow to escape a bind or pinch. It’s great to get multiple dividend paychecks a month. You’ll understand my logic when you see the dividends hitting your account. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply