Have you seen the new narrative concerning retirement? It basically says that no one will be able to retire unless they are in the top 5-10% of wage earners.

Do you believe this nonsense? I believe that anyone who sets a goal and stays on the path can retire comfortably with honor.

However, you must understand all the tools available to set a goal. Many people only focus on a 401K plan, Social Security, or a Roth IRA. However, there are many more ways to supplement your retirement income, with income investing being my favorite. Let’s begin.

Santa’s Bringing Closed-End Funds for Christmas

The road to retirement. The most crucial step to retiring is projecting your future budget. The definition of being wealthy is having more income than expenses.

Therefore, you are wealthy if you earn $4,000 per month and live on $3,000 per month. Always keep the definition of wealth in mind.

Towards the end of my military career, my wife and I began living on $6,000 per month. Once I retired, I discovered my pension would pay me $9,000 monthly.

Even with this fantastic income, I still supplement my retirement with additional income streams, including dividends ($1,500), royalties ($200), options trading ($1,000), and rent ($800).

I keep growing my income because we never know what the future holds for me or my family: the more income, the merrier.

Five Takeaways from “The Option Wheel Strategy”

Dividends and retirement. Today, I want to focus on income investing as a way to add more income to your retirement. What is income investing?

Investing for income is when you purchase high-yielding products on the stock market with the primary purpose of producing income.

Let’s say you have $2,000 to invest. You could purchase Tesla (TLSA) stock that should appreciate in value over the years; however, it doesn’t pay dividends.

You could purchase a shiny new Bitcoin ETF (like BTCW). But these also do not pay dividends. When you invest for capital gains, you must sell your shares to produce income for expenses.

The Magic of Trading Long Strangles

I want my income now. Plus, I want to keep my shares. I never want to sell shares to generate income. In fact, I want to reinvest some of my income to grow my shares over time. Welcome to income investing.

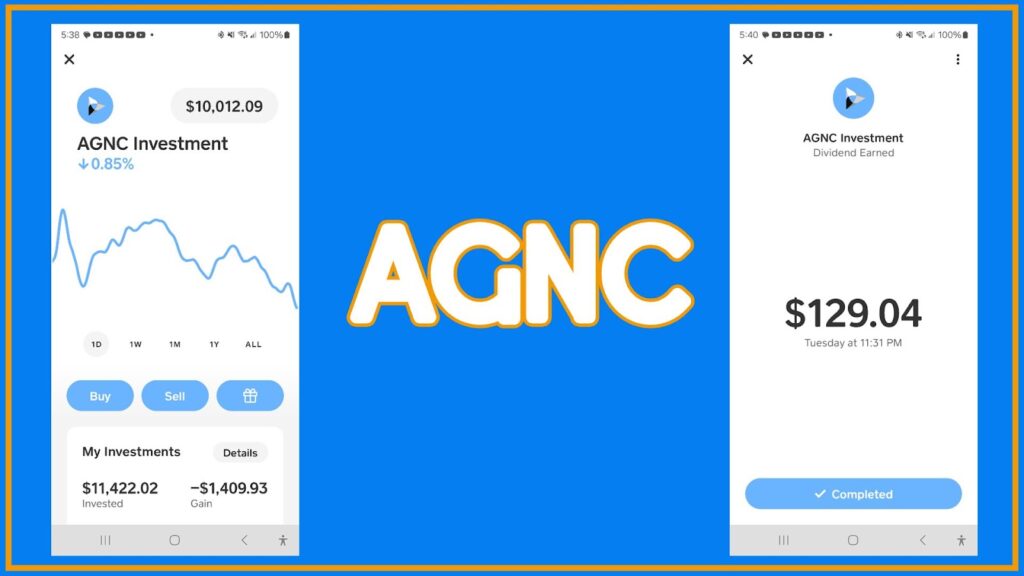

The appeal of immediate income. Let’s take a look at one of my favorite monthly dividends. On my Cash App brokerage, I invested $11,422 in AGNC, a monthly-paying mortgage REIT.

This position pays me $129.04 per month. We can calculate the yield on cost for this position by taking the annual dividend total ($1,548) and dividing it into the amount invested ($11,422).

The yield on cost for this position is 13.55%, which is outstanding. If I never added any more money to the position over 20 years, it would still generate $30,960. If I reinvent 25%, it would generate even more over the years.

Should Multiple Families Live Together?

The main takeaway is that I never have to sell my shares to generate income for retirement. AGNC keeps working to keep food on my table and electricity in my home.

Income investing and budgeting. Returning to budgeting, the best way to become an income investor is to have your dividends slowly pay for your bills.

When you first start purchasing the six types of income products, you won’t receive much in dividends—it takes a lot to build a hefty paycheck.

You may only be able to pay your Netflix or Hulu bills after the first year but keep at it. Soon, you will be able to cover your water or phone bill.

You could cover your car payment or mortgage in a few years—the sky’s the limit. But how do you get the money to invest in income products?

Income Investing for the Win!!

The power of cash flow. Most people do not understand the power of cash flow, which is the difference between income and expenses.

This number is negative for many people, meaning they live on credit cards or other forms of debt. The goal of life is to create the greatest positive amount of cash flow possible.

Let’s say you earn $10,000 per month at your job but live on $10,000 per month. Your first task is to reduce your expenses.

You can do this by slashing your food and entertainment budgets and reducing your streaming costs. Let’s say you free up $1,000 extra dollars per month.

Seven Reasons to Become an Income Investor

You funnel that extra $1,000 directly into income-generating products like AGNC. After a year of investing, AGNC would be paying you over $140 per month.

Reduce expenses but also increase income. You could get a part-time job, create content, or rent a room. Do whatever it takes to make more money to invest.

Let’s say you start by buying an ATM and renting a room. These help you create another $2,000 per month. Now, you are investing $3,000 per month in AGNC (in reality, you would diversify).

In five years, you could have $60,000 invested in AGNC, which would pay you $677 per month. I predict you would have much more if you became serious about your financial journey.

My wife and I invested over $300,000 in less than five years by increasing our income and reducing expenses. It’s possible.

Five Takeaways from “Rich Dad Poor Dad for Teens”

The magic of cash flow. The best part is that you can keep your income streams going into retirement. Let’s review what you learned over the years.

You learned how to invest for income ($677), rent rooms ($1,000), and leverage an ATM ($1,000). As you retire, you already have over $2,500 in additional income.

The more creative you become, the more income you will generate. But always feed the money back to your dividend-paying assets. Here’s why.

Dividends are the most passive form of passive income. If you never opened your brokerage account for five years, your dividends would continue growing and compounding.

Managing an ATM and roommates requires action from you. If you went into a coma, these income streams would stop. That’s why focusing on your money system (dividends) is vital. In the end, your dividends will set you free.

What is Financial Awareness?

Although my wife and I have a great military pension, my focus is on converting that income into dividends. When I pass away, my pension goes with me, but my dividends stay.

Conclusion. The best part of investing for income is that you must create a life around this pursuit. It requires you to think like a business owner or entrepreneur.

You must reduce expenses and increase income to generate cash flow. You then use this cash flow to invest in high-yield income products like closed-end funds, preferred shares, Mortgage REITs, business development companies, dividend stocks, and dividend ETFs.

Winning the Lottery with Options Trading

As you create and invest more cash flow, your income portfolio will generate more income. You make more money every month you invest.

If you can understand this process in your 40s and 50s, you will be on your way to a fruitful retirement.

Many people think only of their 401 (k) and Social Security as sources of retirement income. However, adding dividends, rental income, and a small business (ATM machine) can create a great lifestyle.

Traveling to Istanbul on Passive Income #1

Even better, you can teach the next generation about dividends, rents, and business when they are in their 20s or earlier. What better way to pay it forward than to create financially independent children?

Don’t believe the “never retire” hype. You can retire honorably, but it requires a different approach. My parents were raised in the old ways—to work hard for the same company for 30+ years.

At age 38, I had to perform a hard pivot. I became an income investor and never looked back. Now, at age 43, I generate $1,500 per month in dividends. I want to make this $10,000 monthly over the next 20 years. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply