As we steam towards retirement, we will start to hear new words that gain more traction as we age. Annuities are definitely an older person thing, but it is valuable to explore their importance to an overall cash flow retirement system. We also want to compare them to what a dividend portfolio can provide for us.

An annuity is an insurance contract issued to create a consistent monthly payment to the holder for the rest of their life. You can read a more detailed analysis of annuities here at Investopedia.

How would an annuity function in a real scenario? Say at age 60; you had $500,000 in your 401K savings account. You haven’t been tracking the stock market, and you wanted to ensure this money lasts you until the end.

How We Built 13 Streams of Income

You would go to an insurance company and give them a lump sum of your cash, say $200,000, and they would guarantee you a payment for the rest of your life. The payment has many factors that go into it, and I highly recommend you read the article above for more details.

One of the things annuities are infamous for is being extremely confusing and complex. The value of the annuity can be tied by the stock market, how long you live, if you want your spouse to continue receiving benefits, etc. Purchasing an annuity is a big deal, and the devil is in the details. I usually read as much as I can about annuities on the Kiplinger Retirement website.

But we need to make an assumption to continue the planning process, so let’s say our $200,000 annuity will give us $8,000/year or $667/month. I simply based this amount off of the 4% rule. You would receive $667/month for the rest of your life and perhaps a small cost of living adjustment from time to time. Actually, that’s not too bad—but can dividends do better?

Build the Mindset of an Investor

I interrupt this article to have a deep, lifetime discussion. We need to talk about the type of person who invests in annuities versus that who invests in dividends. The annuity person has been working hard their entire life, saving their money in a Roth IRA, more likely, an 401K.

In a 401K, their employer and they have been saving a percentage of their earned income directly into the savings account. They pick the target date fund closest to their retirement year and keep investing.

In a Roth IRA, there is a high probability that they invest in index funds. Index funds are great, and even I have my favorite ones, but they don’t pay a lot of income via dividends.

The reason I bring this interruption up is to convey that the average annuity investor doesn’t know much about the stock market, dividends, inflation hedges, bonds, or high-income products. More than likely, they will want to turn their money over to a manager to handle their income.

Start Investing or Pay Off Debt

Ladies and Gentlemen, there is nothing wrong with remaining oblivious to the world of finance and the stock market. However, in the long run, you will pay the price. If you still have some time left before retirement, I highly recommend you start learning to handle your money yourself. It may take some time, but you will build more confidence, save more money, and leave more cash to your family. The article “How We Plan to Retire on Dividends (book)” is an excellent place to start.

One more caveat before I continue the comparison, I believe in a total cash flow retirement system that encompasses real estate, business, cryptocurrencies, dividends, and retirement planning. So if I had $500,000, I would diversify this into multiple assets classes and create income-generating investments that would easily last me a lifetime.

For example, I would:

- buy a home in a small town ($140,000),

- put a portion into high-yield stock market products to get a yield of 9% ($100,000),

- put some in growth products like index funds ($60,000),

- put some into business ideas like a dog park, an insect business, or rental car business ($100,000),

- Save into bond products ($50,000),

- and the remaining in cash ($50,000)

- I would also ensure I could rent rooms in my new home—if you are new to Military Family Investing, these are things I talk about every day.

Now, back to our comparison between what an annuity can provide versus what you can earn via dividends. We concluded that our $200,000 annuity would give us $8,000/year or $6677/month in income. This income is almost guaranteed, barring the insurance company doesn’t go out of business. There are no guarantees on the stock market.

Dividends vs. Royalties

Variety is the name of the game when it comes to dividends. You have as many choices as there are stars in the sky. Let’s start with the high-income approach. Our total portfolio was $500,000. We are using $200,000 to produce a liveable income. If we remain relatively safe with our remaining $300,000, say cash or government treasuries, we can take some risk with the additional $200,000.

Let’s put our $200,000 across four closed-end funds and generate a 10% dividend yield across the board. We will want to average into these positions over a year or maybe even two years. You want to buy high-yield products when they are at their lowest prices—offering their highest yields.

At a 10% dividend yield, our $200,000 investment would produce us $20,000/year or $1,667/month—almost three times as much as our annuity. But, it is riskier—or is it? If you have your $300,000 in safe investments, you would not have to cash out of your closed-end funds during a downturn. You could buy more closed-end funds during the downturn. It is a mindset that you will

have to build.

Boring Investing vs. Good Investing

Okay, now what if you created a dividend growth investment with your $200,000. The goal of the portfolio would be to generate 5% growth and a 5% dividend yield. Remember, your annuity is not growing anymore; you are just receiving a payment.

If we build a solid portfolio of index funds, blue-chips stocks, REITs, preferreds, and closed-end funds, we could achieve the goals of five and five. There would be two forms of growth in this portfolio, your overall capital gains and the dividend growth for each company and security.

Let’s look at our capital gains over twenty years (so from age 60 to 80). Using our compound interest calculator, our 5% in capital gains would leave us with $530,000. Excellent, we have actually more than doubled our investments.

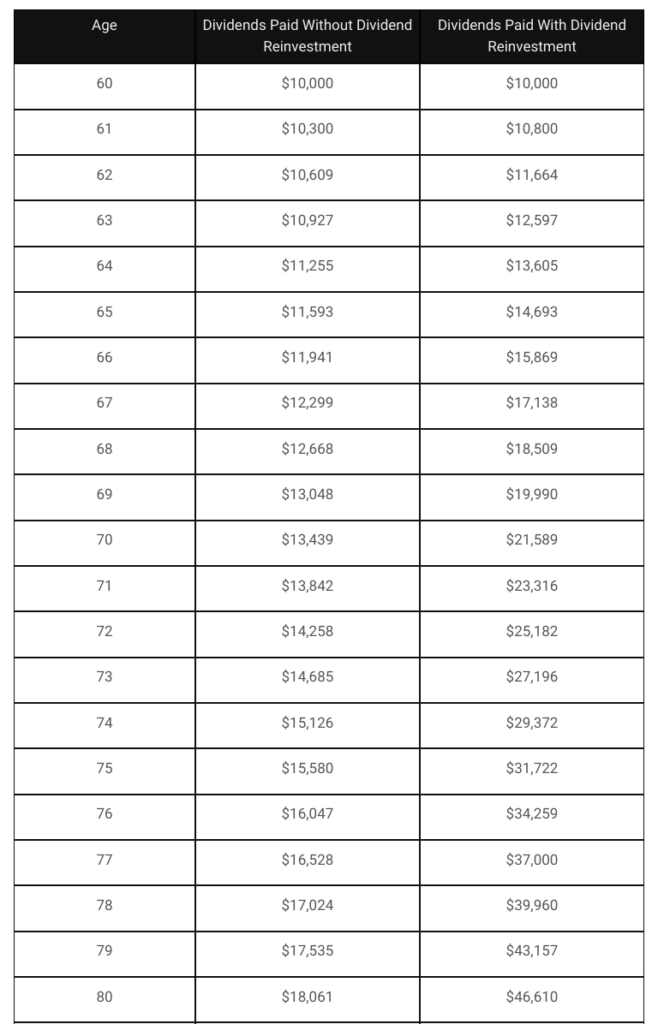

If we start with a 5% dividend yield, our portfolio will generate $10,000/year or $833/month. So, a little more than our annuity. However, with our companies and funds growing their dividends, we would be receiving higher payments every year. Using our simple dividend growth calculator, you can see how impressive the numbers are. By age 80, without reinvesting your dividends, you would be receiving $18,000/year or $1,500/month. That is, with a dividend growth rate of 3%, which is highly realistic. I will leave the chart at the end of the article because it is simply amazing.

Good Debt vs. Bad Debt

Conclusion. You can see that dividends will simply destroy an annuity over time. However, (with dramatic pause), you would have to jump in and start learning. You would need to take 1-2 hours a day to get familiar with stocks, blue chips, REITs, preferred shares, closed-end funds, business development companies, and electronic traded funds.

But, you would be retired; what better things do you have to do than grow your wealth? I am a hardcore dividend investor, and I have seen the magic of dividends. My wife and I have raised our dividend growth portfolio to almost $200,000 in two years and a monthly payout of $500/month.

And we are 40 years old. With our dividend growth calculator, the numbers are insane, even if we stopped today and just let everything compound. As I said earlier, we are total investors and believe in a cash flow retirement system. We have rents, royalties, and dividends keeping us warm at night and a military pension for backup. It’s a great life.

If all this sounds good, jump into Military Family Investing, where I publish an article every day and release some form of a book each week. Follow our Facebook page to see the daily release and find our magazine “Financial Independence Magazine” on Kindle. Look at our free book schedule to know when the magazine will be up for free.

Life is better when you take control of your finances. The best time to take control was ten years ago, and the second-best time is today. Good Luck and Happy Investing.

Free PDF Downloads: Download FREE PDF books here

Financial Mindset: Become CEO of Yourself (book)

Retirement Planning: Retirement Planning at Any Age (book)

Investing: How We Plan to Retire on Dividends (book)

Cryptocurrencies: My First Book on Cryptocurrencies (book)

Real Estate: Financial Independence through Real Estate (book)

Business: Retire Rich, Retire Comfortable with a Business (book)

Everything plus way more: The Biggest Book on Passive Income Ever! (book)

Read My Books for Free: Free Kindle Books Schedule also Sign up to Access our “Hidden” Free Kindle Book Schedule where I release 15-20 more free books a week.

Follow us on our Facebook Page (here). Join our Facebook group (here)

20 Books that Will Make You Rich (here) part 2 (here)

Want to Build Passive Income from Books and Affiliate Marketing? (Learn here)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article.

Leave a Reply