An asset is something we can pass on to future generations. Focusing on their futures ensures we make the best decisions for our and their well-being and longevity.

Honestly, we should be financially savvy and independent in our 70s; there is no reason not to be. Therefore, we can begin mapping out our future endowments instead of worrying about how to feed and clothe ourselves.

Welcome to the Stock Market Investing in at Any Age series (20s, 30s, 40s, 50s, 60s), where we turn income into cash flow. Let’s begin with a short story.

Happy Financial Independence Day 3

My early retirement. I retired in 2023, at age 42. The majority of my retirement income comes from my military pension—which is not an asset.

My pension is not an asset because I cannot pass it on to my children and grandchildren. I aim to make more dividend income than pension income in about 15 years.

I now make $9,000/month in retirement income and $2,200/month from dividends. So, I have a ways to go; however, it is more than achievable.

Building up my dividends is essential because they are actual assets I can pass along. When I reach my 60s, I want to invest all of my retirement income in dividends.

Is your legacy important? My grandpa understood money. He wasn’t rich, but he never had issues with money. He owned real estate and acted as a bank in his community.

Cursed Retirement? What is the Sequence of Return Risk?

When I look back at my 20s, I wish I had someone looking out for me financially. Not feeding me money, but ensuring I made smart decisions.

In our 70s, we should act as a ladder to success for our children and grandchildren. That doesn’t mean just being an ATM but also teaching and mentoring them about money.

The more we understand money and wealth creation, the more we can pass along. Therefore, our mission in our 70s is to convert everything we can into cash flow.

Income investing until the end. We will have a massive income investing portfolio in our 70s. At least 70-79% of our portfolio should be in closed-end funds, preferred shares, and dividend ETFs.

Dividend Investing 103: Picking Your Platforms

I’ll be honest; we should be making at least $20,000/month in dividends in our 70s—on the low end. If we have followed our income investing principle for 20-30 years, things should work out well for us.

If you are playing catch-up, you may need to take drastic action. Perhaps you downsize your home and invest the profits. Or you sell something important.

We should not rely on liquidating our 401 (k) to extract income. We can do better by converting our 401 (k), IRAs, annuities, pensions, and social security into income.

Why is income necessary? We want to be able to take care of our families. Wouldn’t you like to bring your kids and grandkids to Disney World in Orlando, Florida?

The Magic of High-Yield Index Fund Reinvestment

Do you want to travel to Spain or Italy with your family? Or how about going on a cruise? The only way to get there is by having lots of money.

Our income allows us to be generous. We can start an income investing portfolio for our grandkids via custodial accounts. I already have accounts for my kids, nephews, and nieces.

Money helps us keep our families together. We need it to help us fly family members home for the holidays or deal with emergencies.

Handling the rest of our portfolio. If we are 75, we should invest 75% of our portfolio into income-investing assets. This includes closed-end funds like PIMCO Dynamic Fund (PDI).

We can allocate 5% to speculation, such as Bitcoin ETFs and young IPO stocks. These would also be good investments for our grandkids’ custodial accounts.

Dividend Investing 102: Picking the Right Stocks

We should allocate 10% to index funds to ensure we have growth. My favorite index funds are Dow Jones Industrial (DIA), Nasdaq 100 (QQQ), Total Stock Market (VTI), and S&P 500 (SPY).

The final 10% goes to dividend growth investing stocks like McDonald’s (MCD), Google (GOOG), Facebook (META), and Home Depot (HD). DGI stocks help us grow our wealth alongside inflation while paying us throughout the journey.

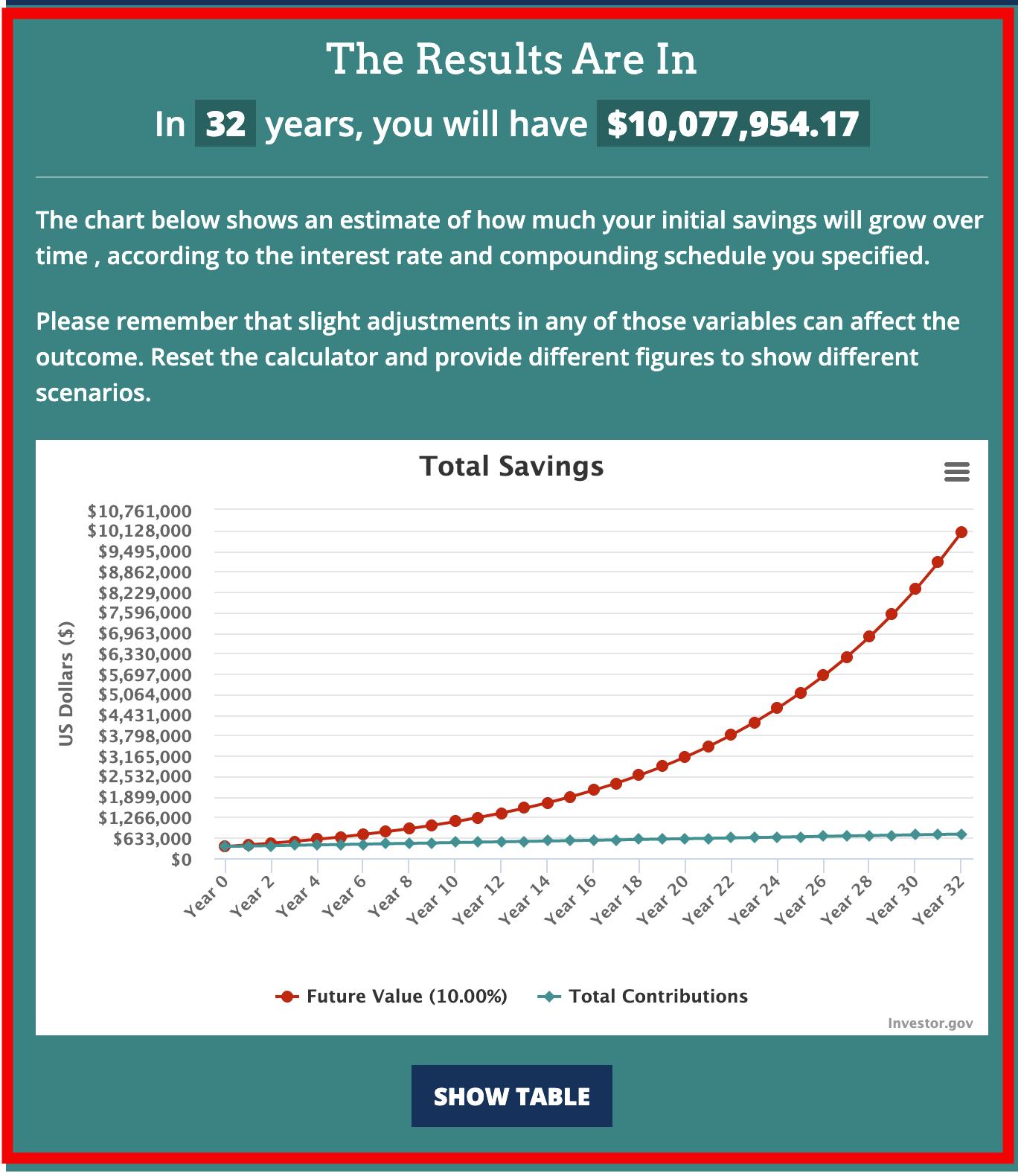

Running the numbers. Let’s run the numbers on my current $363,000 portfolio. I am 43 years old; therefore, I will give myself 32 years of income investing until I reach 75.

First, I want to add $1,000 per month to the portfolio. Remember, my goal is eventually to invest my entire pension into income products.

My Five Year Plan for My Book Business

I will grow the portfolio at a 10% growth rate over those 32 years. I plug those numbers into my compound interest calculator and reach $10 million.

More importantly, the portfolio will yield at least 10% annually in dividends. That would give me $1 million in annual dividend income or $83,333/month.

With this type of money, I can do a lot for my family—wouldn’t you say? My task is to keep my eye on the prize and ensure I reach these numbers.

Getting you to your numbers? How about your numbers? What is your current age, and how much do you have in your brokerage accounts?

If you don’t have massive numbers, don’t fret. You have something you use to catapult you into the world of income.

Dividend Investing 101: What Are Dividends?

You can start a consulting business, invest in real estate, or become a content creator. My wife and I arrived at these numbers by getting roommates.

If you start with nothing at age 18, you must overcome the lack of resources. The only way to gain assets is by living far below your means and creating something from nothing.

Once you build something amazing, you must understand how to extract yield from the stock market. Do you know the difference between fixed income, bond ETFs, preferred equity, REITs, BDCs, asset managers, and index funds?

If you don’t follow these products, now is the time to start. If you don’t know the difference between a mortgage REIT and an equity REIT, then head over to SeekingAlpha.com today.

Putting it all together. We live in the information age. There has never been a better time to learn about income investing and how to extract yield from the markets.

Minimalism is Now a Necessity

I am a massive fan of income investing. While I love index funds and dividend growth stocks, my heart is in income investing.

Imagine going through your 20s with an income investing portfolio that pays you $2,000/month. Would that have been amazing?

Although we didn’t receive that level of support, we can still pay it forward to our kids and grandkids. That’s my focus in life.

Conclusion. I won’t need $83,000/month in passive dividend income, but it would be a nice luxury.

Saving & Investing 103: What is Your Investment Philosophy?

I can begin forwarding income to my family while I am still alive. This will allow me to fund my and my wife’s long-term care plans without breaking a sweat.

More importantly, I won’t need a reverse mortgage to fund my lifestyle. With the proper mindset, I can forward all of my property, income, and assets to future generations.

Many people don’t want to leave money to their kids and grandkids. I think planning for their futures is the entire point of our lives.

I already lived my glory years in the Marine Corps. My wife and I have been married for 20 years and have had our young and “dumb” days.

Now we are laser-focused on getting these kids into great positions to have more kids while living great lives. That’s the power of having “the information.” Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply