How secure is your retirement? Do you feel confident that you have the financial sophistication to survive and thrive into old age?

We can all take steps to ensure a healthy, wealthy retirement. One of these steps is to use US Treasuries to protect our principal and create great passive income.

But what makes US Treasuries so crucial to the overall health of our retirement? Why should we take a lower return than stocks? Let’s find out.

Stocks, Bonds, & Options in Your 50s

Security is everything. During retirement, financial security is everything. When the stock market crashes, you do not want to be worried about your life savings or 401K.

Instead, you want to be able to draw on a large pot of money that is not invested in the stock market or real estate.

US Treasuries provide retirees protection of principal, bond growth investing, and passive income with reduced tax responsibilities. Let’s examine each of these individually.

Protection of principal. Many investors assume the stock market, real estate, and cryptocurrencies will always rise; however, this isn’t the case.

We must set aside money outside the stock market to prevent disaster during a downturn; this is where US Treasuries come in handy.

Preparing for a Recession #4

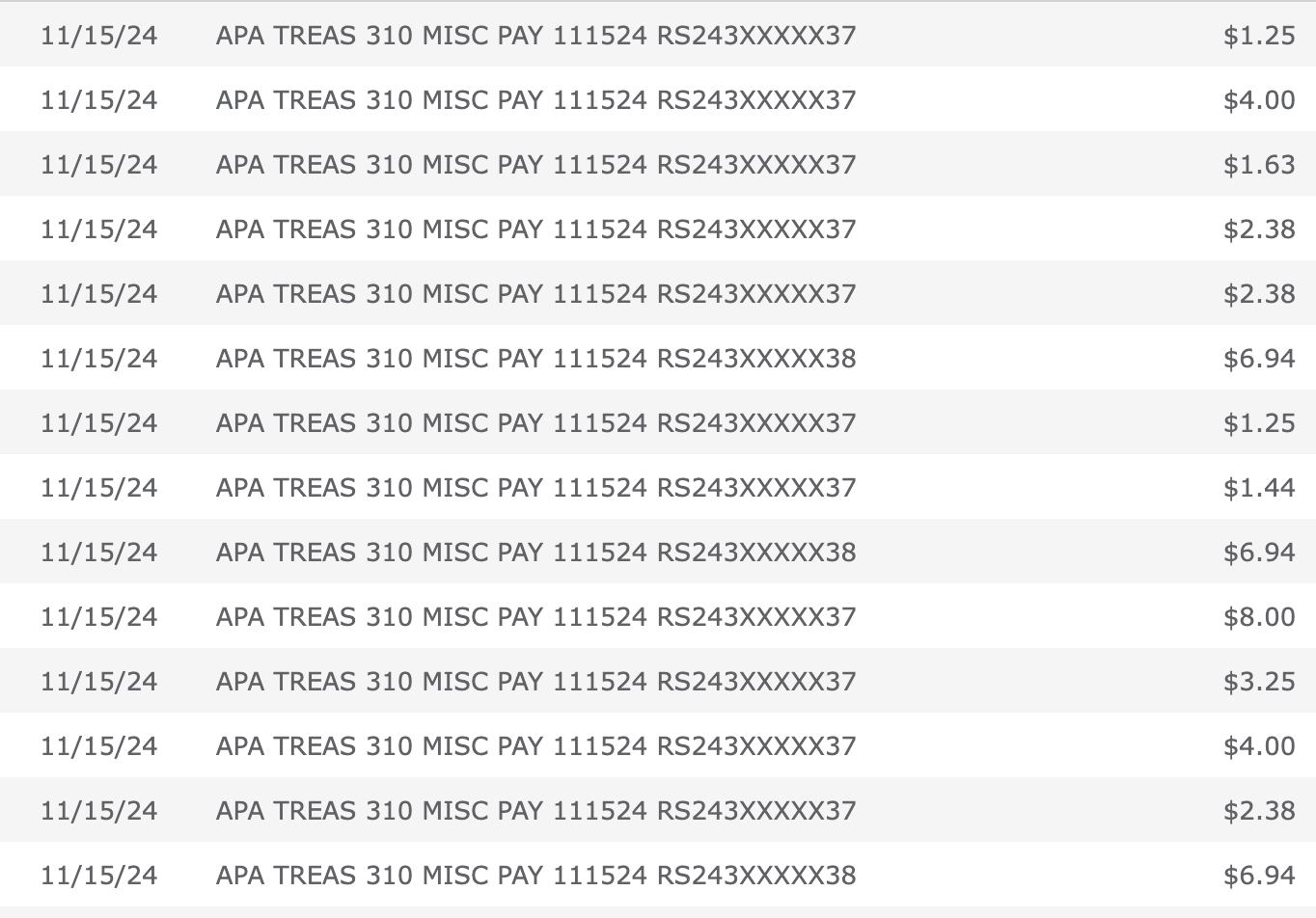

Investors consider US Treasuries risk-free assets, meaning the government pays you to assume no risk.

The best way to protect your bond investments is by building a Treasury Bond Ladder that combines multiple bond types with different maturity dates. But more on this later.

You will never lose money with Treasury Bonds as long as you hold them until maturity. If you sell them early, you may lose some principal.

When you compare this dynamic with stocks, you see a stark difference. With stocks, you have no guarantee of principal, so that is something you need to consider as you allocate resources.

Bond Growth Investing. You should always purchase bonds to hold until maturity. However, there may be times when you can sell your bonds at a profit.

30 Monthly-Paying Stocks in One Account

Bonds’ prices start at 100 when they are new. However, the price can change during its lifetime depending on current interest rates.

Sometimes, it can be 110 if you hold a superior interest rate, or it could be 90 if your bond’s interest rate is weak compared to current rates.

If you see a major discrepancy in your favor, you may want to sell your bond for a profit. Let’s look at a quick example.

Let’s say you hold a $10,000 30-year Treasury Bond with a 4.5% interest rate. If the Federal Reserve lowers its rate to 1.5%, the par value of your bond could shoot up.

The Dividend Snowball Effect

The bond market may be willing to pay you $11,000 for your bond. Therefore, you can do the math on what’s going on in your situation.

Consider how you will reinvest the money at a higher interest rate. Since you can’t get another Treasury Bond for 4.5%, you may need to look for other fixed-income investments, like preferred shares.

I am not a huge fan of bond growth investing with Treasuries. The process works better with bond funds that trade on the stock market, as it is much easier to sell them—plus, you can see how much you will make before the trade.

Passive income with reduced tax liabilities. Bonds are not high-yield savings accounts; they can be much better. First and foremost, bond investors can lock in massive interest rates for 30 years.

Stocks, Bonds, & Options in Your 40s

I have a couple 30-Year Treasury Bonds with a 4.63% interest rate. As current rates decline, I can keep my exceptional rates.

High-yield savings accounts are the first to drop their rates when rates decrease. This may have a significant effect on your passive income.

Another thing that separates US Treasuries from HYSAs is tax liabilities. US Treasury investors do not pay state tax on income from these bonds. Conversely, HYSA investors must pay taxes on interest at the state and federal levels.

If you live in a high-state-tax area, you should consider this distinction. You could save 6-12% on your passive income from your safe investments.

The Options Wheel vs. Certificates of Deposit

Building a Treasury Bond Ladder. US Treasuries come in a variety of flavors: Treasury Bills, Treasury Notes, and Treasury Bonds. You will want to navigate these types to build a great ladder.

- Treasury Bills have short durations of less than one year.

- Treasury Notes have durations between 2 and 10 years.

- Treasury Bonds have durations between 20 and 30 years.

Each investor must take their situation into account. For example, I have a nice government pension, so I invest heavily in 30-year Treasury Bonds.

If you have more short-term needs, you may want to recycle 2-year Treasury Notes. It all comes down to your vision of the future.

HYSAs vs. Series “I” Bonds vs. CDs vs. Treasury Bills

You may consider Treasury Bills as your emergency fund, Treasury Notes as your current income, and Treasury Bonds as your pension.

Using this analysis, you could split $500,000 into Treasury Bills ($200,000), Treasury Notes ($150,000), and Treasury Bonds ($150,000).

In my current situation, I would split $500,000 between Treasury Bills ($50,000), Treasury Notes ($50,000), and Treasury Bonds ($400,000).

My main concern is locking in interest rates over 4%. Again, your analysis and situation may be much different than mine. That is why it is so important to understand these investments.

The goal of your Treasury Bond Ladder is to consistently have new money available to invest while keeping some cash in high-yielding bonds.

Preparing for a Recession #3

If you are paranoid about short-term rates or the economy, you should recycle $20,000 in 1-month Treasuries. That way, you will always have cash on hand for an ever-changing environment.

If you see good long-term rates and don’t plan on selling, 30-year bonds may be your preference. Retirement changes everything you know about money.

Conclusion. When you retire, your number one source of income (your job) goes away. Therefore, you must depend on your intelligence and financial sophistication to keep you afloat.

Become a Digital Nomad with Options Trading

Another thing that makes bonds ideal in retirement is high-yield bond reinvestment. This means you reinvest your passive bond income at higher rates while keeping the principal safe.

If I had a $100,000 30-year Treasury Bond at $4.63%, it would pay me $4,630 annually. I could then invest that money in a closed-end fund at 10%.

Without compounding, I would have $138,900 in my Pimco Dynamic Fund (PDI) in 30 years. It would pay me $13,890 annually for the rest of my life.

High-yield bond reinvestment is the true value in bond growth investing and building a Treasury Bond Ladder. Every cent you earn in interest should go toward high-yielding investments. That’s how you become wealthy. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply