We have finally made it to my favorite type of passive income—income investing. Although we took the long way, it is necessary to understand how we got here.

Income investing is not for the faint of heart. That’s why starting with interest from high-yield savings accounts is good, and slowly work your way forward.

Welcome to the Middle-Class Investing 101 series (101, 102, 103, 104, 105, 106, 107, 108), where we get rich in the middle.

Selling Covered Calls for Passive Income

Why become an income investor? Income investing is the concept of buying securities only for income. It is akin to purchasing fixed-income products like bonds.

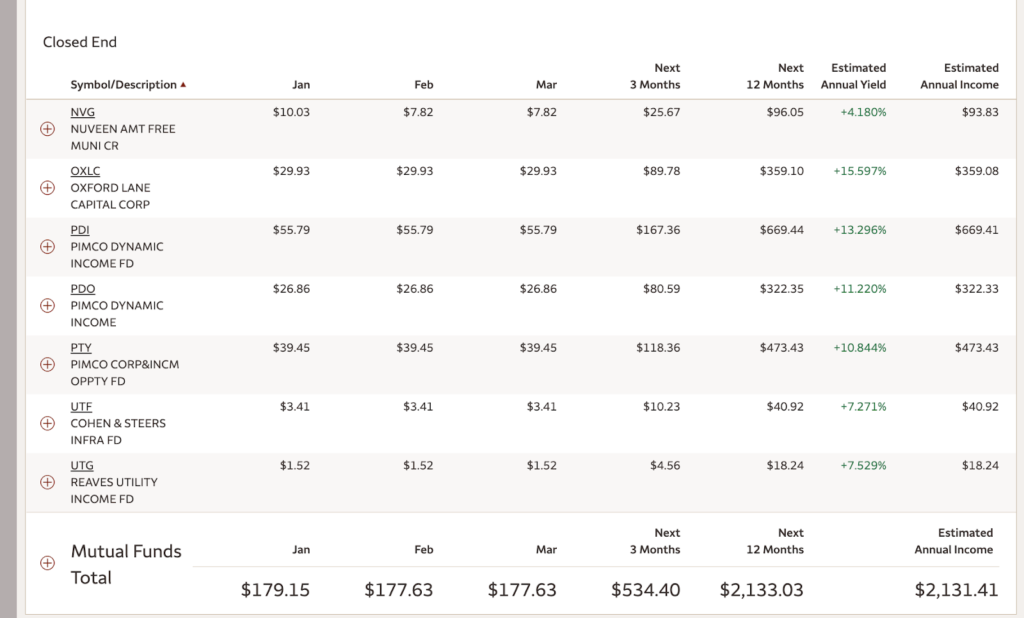

I became an income investor because math attracts me. Let’s say I have $1,000 to spend. I know I can invest it into a monthly-paying closed-end fund like PDI.

If I buy PDI when it yields 11%, I can determine how much I will receive every month. In this case $9.16 per month.

I can also use the rule of 72 to determine that it will take 6.5 years to get my initial investment back via the dividends.

Retirement Planning for the Average Person 2

Keep buying more income. Once you begin to get your dividend train moving, you reinvest into more income products.

If you receive $1,000 per month in dividends, reinvest 25% or $250 back into more products such as preferred shares, closed-end funds, and mortgage REITs.

Life is good as an income investor because you can immediately use your dividends to assist you through life.

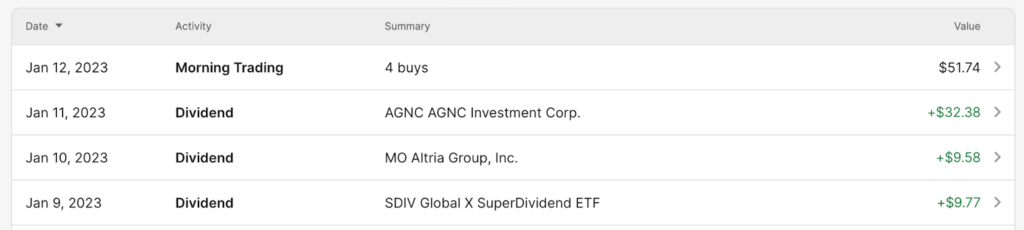

How I use my dividends. I spend my dividends via my Dividend Debit Card—a Cash App card tied to a brokerage account.

Should You Manage Your Own Rental Properties?

My wife also has a Dividend Debit card, and she loves it. Every month she invests $1,000 into more dividend stocks to grow her paycheck constantly.

I use my Dividend Debit card for fun things like fast food and little trinkets. The best part is that I don’t have to document the spending on my $50/day budget.

Income investing is so fun because you don’t need to wait 50 years to enjoy your dividends. You have your index funds and dividend growth portfolios for the long term.

Income investing is all about today. However, your portfolio will also serve you well going into retirement.

Living Overseas on Passively 103: Retirement Income

Wouldn’t it be nice to go into retirement with a $5,000/month income investing portfolio? My goal is to build my portfolio to $10,000/month before I turn 50 (I’m 41 now).

Getting started with income investing. So how do you start income investing? The first step is to pick a platform.

Your platform will determine which income products you can purchase. For example, Cash App doesn’t offer preferred shares or closed-end funds.

As much as I love Cash App, I would start at a major brokerage like Charles Schwab or Well Fargo. In fact, Well Frago has the best income calendar in the business.

With the Wells Fargo income calendar, you can see exactly your monthly dividend numbers. It helps to right-size your monthly totals.

Create a Stream of Never-Ending Content 2

Once you have a platform, it is time to create an automated income investing schedule. Income investing is fire-and-forget.

However, deciding how you reinvest your dividends will determine your daily involvement. It is nice to have multiple brokerages to tinker with various reinvestment styles.

Buying more income products. Perhaps the most fun inside income investing is using your dividends to buy more dividends.

What is Passive Income?

You can do this in three significant ways 1) reinvest into the same stocks, 2) let the cash build, and 3) let the cash build and auto-reinvest.

I reinvest in the same stocks on Charles Schwab. I like to grow a position like PFFA by letting it make itself bigger through reinvestment.

I let the cash balance build in my Wells Fargo brokerage account. If I wait a month, I will have $300 to spend. It is fun to look at current yields and make decisions on the spot.

Finally, M1 Finance lets your cash build to a certain point, then automatically reinvest it across your portfolio. This way is excellent for capturing the best-yielding products autonomously.

The Wealth Accumulation Phase

Is income investing right for you? Most people cannot become income investors. Learning the various markets (housing, bonds, stocks, Treasuries) takes time.

Your principal will fluctuate more than dividend growth investing because you are dealing with leveraged products.

Leverage is good during good times and bad during bad times. Leverage magnifies your gains or your losses.

Orange You Glad You Have Passive Income?

That’s why it is a great idea to understand income investing before jumping the gun. The Middle-Class Investing series helps you work your way up to become an income investor.

The best income investors. The best income investors have an entire plan. They have an emergency fund and a retirement plan (DGI and Index funds), and they follow the markets.

There are no get-rich-quick schemes, only the information. Last month, my wife and I earned $1,850 in dividends.

Why You Should Learn Creativity & Design

This kind of income can change your life. It’s even scarier knowing I will earn more this year. However, we did the slow work to build our portfolio from $0.25 in August 2019.

Conclusion. I know that income investing is a step too far for most middle-class Americans. However, my job is to present you with the answers to your questions.

Do you want to have more cash flow? Do you want to control your retirement planning? Do you want to feel more comfortable about your finances? Do you want to have guilt-free spending?

Real Estate is a Mindset (Advanced)

I present income investing as the answer to all your questions. But it will take work to create the right portfolio for your risk tolerance.

I absolutely adore income investing, and it has changed my life. There is nothing like receiving a nice fat dividend to make your day.

Even better is treating yourself to McDonald’s (MCD) or Starbucks (SBUX) with your dividends. This is the way life should have been from the start. However, no one gave us the information.

Now that you have it, it’s up to you to leverage it to improve your lifestyle. I am on the other side, and boy, it feels incredible. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply