There is nothing cute or funny about being broke in your 60s. It’s not amusing to still have to work a full-time job when you have grandkids.

As a retired 44-year-old, I do not say this to offend people but rather to rally them toward a mission of financial freedom.

Worst of all, if you don’t figure out how to free yourself, how can you help others? Isn’t our goal as parents and grandparents to assist our offspring from falling into certain traps?

As a retiree, I see many people choosing to enjoy today over investing for tomorrow. I see people buying expensive cars, installing pools, and traveling to fancy places aboard—all while not having money in the bank.

- Planning for Retirement in Your 60s

- Real Estate Investing in Your 60s

- Staying Debt-Free in Your 60s

- Dividend Investing in Your 60s

- Bond Investing in Your 60s

- Stock & Bond Investing in Your 60s

- Options Trading in Your 60s

- Stocks, Bonds, and Options in Your 60s

- Stock Market Investing in Your 60s

My plan for my 60s. Here is my monthly financial plan for my 60s: military retirement ($11,000), dividends ($10,000), rent ($6,000), and royalties ($2,000).

That’s $29,000/month in passive income, which is on the low side. I envision having numbers twice as big.

Home Buying for the Average Person 2

I can forecast ahead because I am looking toward the future. I care about my future financial plan; therefore, I am making smart moves today to achieve my goals.

For example, I am going to college on the GI Bill, which pays me $1,800/month. I invest this money directly into high-yield income investing products like preferred shares and closed-end funds.

What are your plans for your 60s? In America, I see many older individuals focused on being consumers. They want to live their best lives, at the expense of tomorrow.

The funny part is that if you get ahead in your finances, you’ll have as much money as you want—to do the things you desire. For example, I just took my entire family to Biloxi, Mississippi, using passive investment income.

Your 60s is not the time to be working a full-time job. At most, you want to work a part-time job just for the sake of getting out of the house.

Using Bonds to Create Safe Cash Flow

If you love kids, wouldn’t it be even better to volunteer at the church or be a bus aide? We can do so much for others once our finances are in good shape.

So let’s talk about passive income. What is passive income? Passive income is revenue that your assets generate. Some assets include dividend stocks, corporate bonds, creative royalties, and rental properties.

The goal of your working life is to collect as many income-producing assets as you can. Somehow, most of us never got that memo.

Instead, we focus on funding our lifestyles AND collecting liabilities with our hard-earned income from our jobs. That’s why we remain eternally on the hamster wheel (or meat grinder).

It’s shocking to see people in their 60s still clinging to the old method of working to eat. It’s an outdated paradigm and something everyone has to change within themselves.

There is simply no excuse for not having savings and investing. I spent 20 years in the military before recognizing that I was on a hamster wheel.

Create Budget and Start Income Investing

I was broke and in debt. Even in 2109, when things were cheaper, I couldn’t afford to take my family to Applebee’s.

I took a hard look inside, found myself lacking, and decided to make a massive change. I stopped buying and playing video games and started reading financial books.

Building passive income streams in your 60s. The easiest passive income stream people can make in their 60s is dividend income.

There are two main ways to invest in dividends: dividend growth and income investing. I do both, but I strongly favor income investing.

More importantly, you can start today by buying stocks on your phone through the Cash App. It’s the easiest platform to invest money.

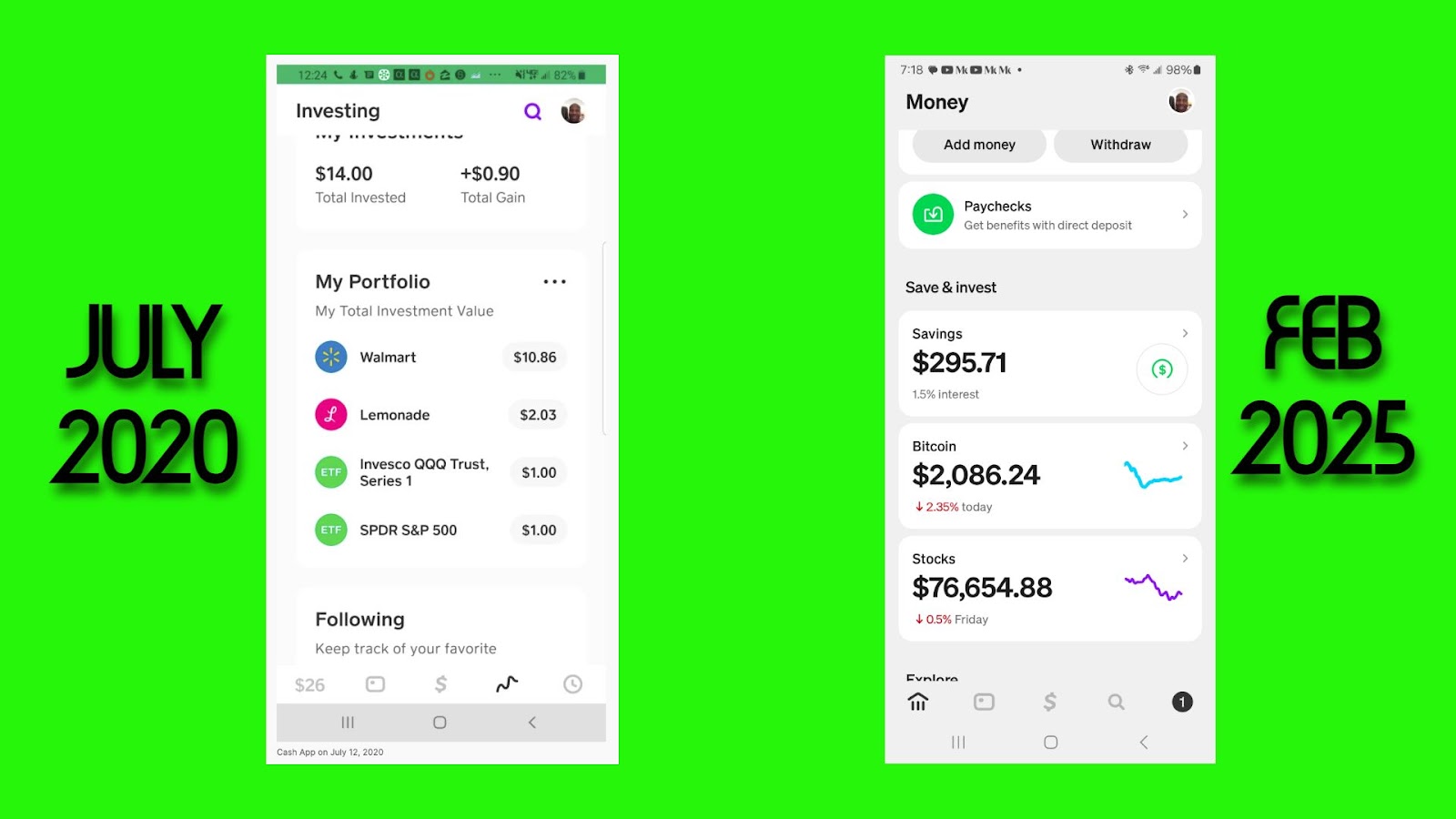

I started investing in Cash App in July 2020 with $12. You can read “What on My Cash App July 12, 2020?” to see exactly where I can come from. Today, February 2025, I now have $76,000 in Cash App.

More importantly, my Cash App pays me $500/month in dividends. That money goes directly to my Cash App balance, which I can use to move to savings, buy Bitcoin, reinvest in more dividend stocks, or spend on whatever I like. Having choices is the magic of dividend investing.

Start with Saving and Interest

If you are struggling to find a way to retire, I recommend you look into dividend investing. Building a robust portfolio takes time, but hopefully, you are a high-earner.

Other types of passive income. As someone in your 60s, hopefully, you own a home. Even better, hopefully, you bought a house 20 years ago.

Now it’s time to reap the benefits of rental income. If you own only one home, it’s time to make hardcore decisions.

How do you earn rental income while only having your primary residence? The first option is to get roommates. My wife and I currently have one roommate that pays us $1,000/month.

Most people scoff at the idea of getting a roommate; however, most people also aren’t retired at age 44.

Having a roommate can expedite your journey toward financial freedom more than anything you can do outside of starting a successful business.

If you don’t want roommates, you can move out of your home and rent it. You have options if you can clear $2,000/month after paying your mortgage.

30-Year Bonds vs. Blue Chip Dividend Stocks

You can move overseas while someone else pays off your home. You can move to a cheaper part of the United States. The idea is to use your home as a wealth generator.

If you have adult children, you could move in with them in exchange for watching their kids. Why pay a random person $2,000/month for child care when you can keep it in the family?

I know these things sound unpopular, but what can I say? My wife and I have had roommates for five years and now have an investment account that is approaching $400,000.

We receive over $2,400/month in dividend income and another $5,200 in rental income. Although we have mortgages on our two rental properties, we will pay those off over the next ten years.

This is to say that we made extreme sacrifices to reach this point. Most people wouldn’t even consider making the sacrifices we did; however, everyone wants to be here—with us.

Building a Solid Retirement Plan

Conclusion. Every day, I wake up to more income. I write a book, do my college homework, and walk the dog with my wife. I have an absolutely great life.

Best of all, we haven’t had to work in 16 months since retirement. Between January 2025 and February 2025 (one month), our investment portfolio increased by $17,000. That’s all without working a job.

The things I am saying work well if you try them. However, many prefer to buy a pool or go to Mexico than invest in dividends.

All I am saying is that it is not amusing or cute to work in your 60s. The workforce is not kind to older people, and it is only accelerating.

If you have something you can leverage to get ahead, what is it? For example, do you own your home, have adult kids, or have high earning potential as a consultant?

Whatever it is, now is the time to change your lifestyle. Unfortunately, there is nowhere to hide when the pink slip comes for you. Start preparing yourself now by building passive income streams. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply