Do you want to have the chance to retire in this lifetime? Even better, do you want to retire early, perhaps in your 40s or 50s?

There has never been a better time to create a Happy Cash Flow Retirement, but it will take sacrifice. Your company no longer gives you a nice pension with unlimited medical benefits and inflation protection.

So, what type of sacrifice is in the cards for you? Sacrifice comes in all shapes and sizes; it may be moving to a small city, working an ungodly amount of hours, starting a business in your spare time, or becoming a content creator. Let me share my story.

Pursue Your Creative Career with Dividends as a Backdrop

How and why we retired in a small city. I wrote an article titled “Retiring to a Small City and Living on Passive Income” over a year ago. At the time, I was just starting the retirement process from the United States Marine Corps.

Now that my wife and I have been fully retired for over seven months, I want to examine our passive income and budgets in our small city, Pensacola, Florida, in more detail.

We have made many sacrifices over the years to get to this point. First, I was in the Marine Corps for 24 years, doing the Lord’s work.

I was born in the expensive city of San Diego, California, so traveling the world showed me how the rest of the population spent their money.

I fell in love with small cities such as Pensacola, Florida; Beaufort, South Carolina; and Yuma, Arizona. I knew I wanted to retire somewhere affordable and less busy.

Income for Retirement: Preferred Shares

I was gone for nine of my 18 years of marriage—that was our initial sacrifice to earn a military pension. However, we had to do even more to achieve financial independence.

In 2019, we struggled with debt, so we decided to get roommates. We had roommates for over four years, and it wasn’t fun. However, it allowed us to clear our debt and build a dividend portfolio.

After serving over ten duty stations in the Marines, we are settled comfortably in our Pensacola home. Now, let’s examine our passive income streams.

Build your passive income before you retire. The best time to build passive income streams for retirement is before you retire. The sooner you get moving, the more mature your streams will be before retirement.

How to Determine Your Bare Bones Budget

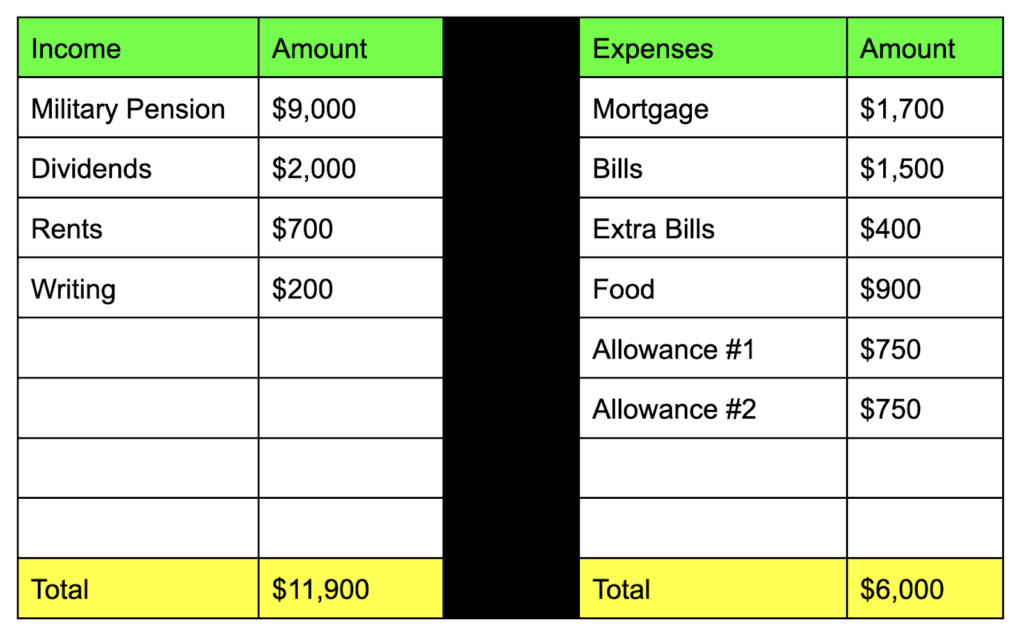

Our number one income stream is our military pension. This income stream took us 24 years to build—24 tough years. However, I look back fondly on my military service; it was well worth the time investment.

My military provides my family with $9,000 per month. In some places, this may not be a lot; in others, it could be considered “F*** You money.” Here in Pensacola, it is more than enough to live a comfortable lifestyle.

If you are young enough to join the military, I recommend you look deeper into it. It can provide all types of resources for your family and give you a higher purpose in life.

Our second income stream is dividends. I started dividend investing in 2019. I love dividend growth investing with companies like McDonald’s (MCD) and Coca-Cola (KO). Also, new companies like Google (GOOG) and Facebook (META) are joining the DGI party.

Who is a Better Steward of Your Time?

But my heart belongs to income investing. Income investing is the art of purchasing securities from the stock market that pay a high dividend yield. I love buying income products!

In total, we earn about $2,000 per month from dividends. We reinvest many of our dividends to ensure the portfolio outpaces inflation.

During our many years in the military, we purchased three homes. We rent two of our homes (one in Pensacola, one in Yuma) to tenants. After paying the mortgages on these properties, we collect a total of $700.

Finally, my most fun passive income stream is writing. It doesn’t pay much because I’ve only been at it for three years, but it keeps my mind sharp. I earn about $200 monthly from writing and selling books on Amazon.

Your Wealth is Your Choice

We also have more ways to make more money if needed by going to college using the G.I. Bill or trading options. But for now, I’ll just focus on our top four choices. As you can see, we earn about $12,000 a month in passive income.

Budgeting is key to success. Having passive income is irrelevant if you spend more than you earn. Spending much less than you earn is imperative to keeping a healthy cash flow in your system, especially during retirement.

Our number one expense is our mortgage, which is $1,700 per month. We bought our current primary residence in 2020 for $340,000. It is a large property (2,500 sq ft) on 3.3 acres.

Over the years, we reduced our interest rate to 2%. The magic of buying a property is that your mortgage can be a hedge against inflation.

Florida has been going through a homeowner’s insurance crisis, so having our dividend portfolio to help outpace housing inflation has been vital to our success.

Writing: I Retired to Start My Dream Job

Our other bills total about $1,500 monthly. This includes utilities, cell phones, and streaming services. We also like to keep another $400 monthly available for annual bills like car registration, Amazon Prime, and termite services.

Our food bill is a place where we like to control our spending. Food prices can get out of hand, so having a firm budget for the month is vital. We give ourselves $900 a month for our family of four and a dog.

For the most part, we stay within our budget. Sometimes, we can go over, and sometimes, the stars align, and we stay under. The important part is that we don’t go to Walmart and begin spending emotionally.

Side Hustle: Gig Economy vs. Entrepreneurship

Finally, my wife and I each have a $750 monthly allowance for personal entertainment, shopping, and beauty spending. I like to divide my allowance into a $25 daily budget, but my wife spends differently.

Now, let’s compare our income and expenses side by side to see how much money we have remaining each month. We call this “extra” money cash flow, and it is the most important part of our retirement program.

The magic of cash flow. As you can see from the table above, we have an additional $6,000 per month that we can save and invest.

Our monthly goal is to have a higher net worth than the month prior. Sometimes, the stock market doesn’t cooperate, but at least we can own more assets every month.

Conclusion. The key to our Happy Cash Flow Retirement is living in a city where our housing costs are less than 25% of our total income.

To Change Your Life: You Must Change Your Life

As long as we stay on budget and on script, we should increase our income every year going into the next. Our dividends will continue to grow at a pace faster than inflation, ensuring our retirement becomes more comfortable each year.

Remember, we got here by sacrificing much of our time and space. We had roommates for five years; I was in the military for 24 years.

I see many people attempting to retire in places like San Diego and New York City. This requires more than financial magic; it requires a massive wealth generator (like a big business).

Make $100 per Month in Passive Income

In big cities, tax rates are higher, and inflation spikes are faster. You work more for a smaller percentage of your income.

I like the slow pace of Pensacola. We are in complete control of our finances. Yes, Florida is annoying because of homeowners and property taxes, but we can plan for these expenses.

If you are considering retiring, now is the time to jump into a small city. Even if you live in a big city, you can still purchase a home in a small town that will be there when you retire. That’s what we did. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply