We all love the idea of recycling—turning something old into something new. In our 60s, we can turn our pile of money (401K) into a massive passive income stream.

That’s right. We will forget the 4% rule and earn 9-10% yields on our invested capital.

Do you need a financial advisor to manage your money while they take a 1% cut? I know you can manage your money on your own. Heck, you saved it in the first place.

Can the Military Elevate You to the Middle-Class?

Welcome back to the Stock Market Investing At Any Age Series (20s, 30s, 40s, 50s), where we thrive and survive on income. Let’s begin.

What is the 4% rule? Conventional wisdom states that you can withdraw 4% of your portfolio as long as the stock market grows 9-10%. Sounds reasonable, I guess.

However, in practice, this withdrawal method causes more stress and anxiety than comfort and stability. Here’s why?

You are essentially dismantling the portfolio you spent 40 years accumulating. Each year, you become more nervous about how much you should withdraw by selling shares. The financial industry loves this fear.

Imagine you have 10,000 shares of the Total Market Index Fund (VTI) at $100 per share, for a total of $1 million.

Selling Cash-Secured Puts for Passive Income

In the first year, you sell 400 shares to generate $40,000 in income, leaving you with 9,600 shares. The following year, you need $50,000 in income due to inflation. You sell 500 shares.

After only two years, you only have 9,100 shares remaining. The stock market may have risen to keep your value afloat, but it may have fallen. You never know.

I don’t want to bore you, but this is bad. We never want to sell shares to generate income. Instead, we want to convert index fund shares into income-investing products that pay us passively.

What is income investing? I’m glad you asked. At age 43, income investing is the lifeblood of my portfolio. It represents the best way for the average person to retire comfortably with a steady paycheck—one that they created.

This is Why I Became a Writer

Income investing works because it operates in the world of fixed income. You purchase securities that pay you money. That’s it.

Let’s examine the PIMCO Dynamic Fund (PDI) closed-end fund, which yields 16%. Each share pays $0.2205 every month.

If I invest $1 million in PDI (at $18.85/share), I will obtain 53,050 shares. I now earn $11,697 in monthly dividends, equating to $140,371 annually.

Can you live on $140,000 per year? I know I sure can. That’s the magic of income investing. You aren’t overly concerned about fluctuations in the stock market, only that PIMCO continues to pay you every month.

Inside Our $240,000 Dividend Portfolio

I bought my first share of PDI on April 22, 2020. I paid $20.81 for one share, which generated $13 in income thus far. The longer I hold the shares, the richer I become.

Feeling safe in retirement. Which method sounds better to you? Would you rather sell shares yearly or have the income delivered on a silver platter?

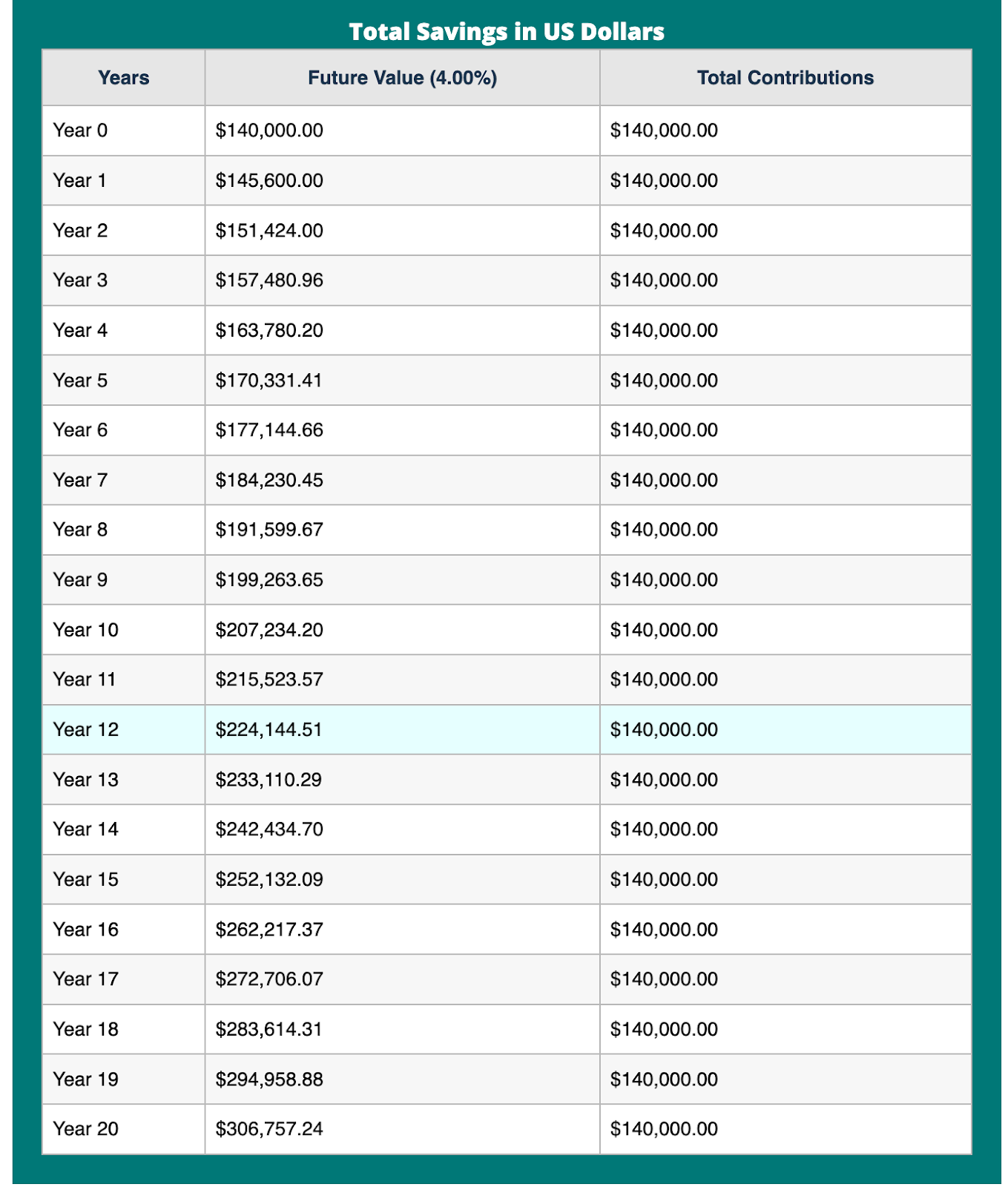

Additionally, the four principles of income investing recommend reinvesting 25% of your income into your portfolio.

Therefore, year one would pay you $140,000 on 53,050 shares. Year two would pay you $145,281 on 54,906 shares. And year three, $150,377 on 56832 shares. Each year you become wealthier.

Does income investing really work? Yes, yes, it does. I began dividend and income investing in June 2019, and today, January 11, 2025, I earn $2,200/month in dividend income.

My dividend income will only continue to grow as I reinvest and add fresh capital to the pot. I expect to earn $10,000/month in dividends by 2035.

Closed-End Funds vs. Dividend ETFs

Income investing as a part of your overall portfolio. Don’t worry; income investing represents 60-69% of your total portfolio, depending on your age.

The rest of our portfolio adds growth and a tiny bit of speculation to our future outlook. Fixed income is just that: fixed. Therefore, we need growth to ensure we continue to beat inflation and cost-of-living increases.

At age 65, we should allocate 65% of our portfolio to income investing. We can use 5% to speculate on cryptocurrencies and young IPO stocks.

We allocate 15% toward index funds such as the Total Stock Market (VTI), S&P 500 (SPY), Nasdaq 100 (QQQ), and Dow Jones Industrial (DIA).

Think of index funds like the equity in your primary residence. It doesn’t mean much until you sell, but it adds to your overall net worth. Index funds represent the same concept.

Financial Freedom vs. Financial Security 2

Banks and lenders will treat you with much more respect when you have substantial capital gains from index funds. They know that you have the resources to repay your loans. Even better, you can become your own bank and lend to yourself on platforms such as M1 Finance.

Finally, we use the remaining 15% to invest in dividend growth stocks. As we age, we want to find higher-yielding products, such as Pfizer (PFE), Verizon (VZ), AT&T (T), British American Tobacco (BTI), and Altria (MO).

These exceptional stocks will grant us current income and a slight chance at growth. We can also invest in faster-growing, lower-yielding stocks like Facebook (META), Google (GOOG), Visa (V), and Mastercard (MA).

Those low-yielders will be great stocks to pass along to family members who can capture long-term returns. We need income.

Passive Income: How Do You Spend Your Free Time

Putting it all together. Investing 100% of our capital into high-yield, fixed-income products like closed-end funds and preferred shares is not wise.

However, 65% is a great number. You still have enough remaining to invest in speculation, growth, and dividend growth.

Under the income investing tab, you can also find low-growth, high-income stocks, such as business development company Ares Capital (ARCC), and high-growth, high-income stocks like asset manager Blackstone (BX).

Ultimately, the definition of wealth is having more income than expenses. There are only two ways to become wealthy: lower expenses and increase income.

As income investors, our income will increase every year. We don’t sell shares to generate revenue; we reinest 25% to ensure we continue to outpace inflation and cost of living expenses.

Turn Your Articles into eBooks

Conclusion. The worst thing you can do in retirement is live on a fixed income. This is not the same as living on a budget.

A budget means that you control your spending. A fixed-income lifestyle implies that someone else controls your spending, such as through Social Security, 401 (k), or a pension.

After spending 40 years depending on a paycheck, why change this mindset during retirement? All you need to do is create your own paycheck through income investing.

Create an eBook Series for Passive Income 2

Can you do it yourself? Of course; I believe in you. The financial industry will try to make this process seem more complicated than it needs to be.

They will use terms like sequence of return risk, inflation, elder care, annuities, taxes, RMDs, social security, and insurance.

All you need to know is that your income must be much higher than your expenses. Find high-paying stocks and lower your expenses, and you’ll be fine. I should know; I retired at age 42. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply