Going into retirement, the worst thing you can do is put yourself on a fixed budget. Conversely, establishing a budget is the best way to prepare for retirement. What’s the difference?

When you live on a fixed income, someone tells you how much you have to spend. When you create a budget, you tell yourself how much you get. Being on a budget creates cash flow.

Cash flow is the difference between income and expenses and is necessary to build wealth. Whatever income comes in, we must create a standard of living below that amount.

Real Estate Investing in Your 70s

Unfortunately, too many seniors rely on a fixed income from Social Security. They do not know how to generate more income, so they are forced to make do with what they receive. Is there a better way?

Let’s create some income. My mom lives on a fixed income consisting of a small California pension, some rental income, and social security.

On January 1, 2024, she gave me $5,000 to grow in the markets. I set my goal to earn 10% each year on this money. On Aug 24, 2024, I crossed the $5,500 mark. Therefore, I have another four months to juice my returns on this account.

I grew this account using a combination of index funds, dividend ETFs, long strangles, covered calls, and cash-secured puts. It’s fun to play around because I know what I’m doing.

505 Takeaways from 101 Books

Most seniors do not have a son or daughter who is savvy in the markets. In fact, most seniors will not become hardcore options, day, or swing traders. However, you have time to learn if you are in your late 40s and 50s.

We do not want to enter our 60s and depend solely on Social Security. Relying on selling shares in our 401 (k) will not be ideal, either.

The key to life is income and cash flow. Wealth is having excess income versus expenses. With that definition in mind, we can become wealthy in retirement—if we do the math.

The math of social security. How much social security will you receive? You can go to the ssa.gov website and see their prediction.

My Social Security prediction is high, but it will not be accurate. It assumes I will work full-time for the next 20+ years, but I am already retired (now age 43). I wrote four years ago, “No Freakin’ Way I Will Work Another 25 Years.”

Inflation Ate My Paycheck 103

Let’s assume you will receive $2,000 per month in social security, and your spouse will earn the same. $4,000 per month is a decent chunk of change, especially if you don’t have a mortgage payment.

However, we can never fall into the trap of saying we have enough. Inflation is the cost of being alive; therefore, someone is always coming to take your resources.

Even if you do not have a mortgage, property taxes, maintenance, home insurance, and HOA fees are completely ridiculous right now. We must continue to increase our cash flow, which will, in turn, increase our savings and investments.

Selling covered calls to the rescue? There is a way to generate decent returns (20% to 30% annually) at home by selling covered calls on the options market.

TSP vs. Dividends

However, you must take many steps to protect your resources before entering the high-stakes options market. The best way to protect yourself from the world of gambling (options) is to not insert your money into the pit (I’ll explain).

Step one is to create an emergency fund. As a future retiree, you will need at least one year’s worth of living expenses in your high-yield savings account (HYSA).

If you are savvy, you can keep 10% to 20% in an HYSA and shuffle the other amounts between Series “I” Bonds, Treasury Bills, Money Market Funds, and Certificates of Deposit.

I would prioritize Series “I” Bonds because the government bases its payments on inflation, not interest rates. The other savings instruments are a product of interest rates set by the Federal Reserve. I digress.

Save for Your Down Payment Fast!

Allocate your investment accounts. Now that you have your $48,000 emergency fund, you need to set up your investment account to handle covered calls.

Options trading should be a small percentage of your overall investments. You do not want to play around with your “real” money. Trading options is a highly emotional affair, similar to being married. You can lower your stress by reducing your risk.

Let’s first start by deciding how much you need in your options account. I follow my own rule of 40 to determine this number.

Let’s say we want to generate $1,000/month in income from selling covered calls. Using my rule of 40, we would need $40,000 in our options account.

You want to have at least double (if not triple) the resources in your investment account as your options portfolio. Let’s go with triple. We will need $120,000 in our investment portfolio.

Use Dividends to Supplement Your Retirement

What’s in our investment portfolio? We have index funds, dividend-paying stocks, growth stocks, and income products like closed-end funds. This portfolio is our bread and butter and should generate $600 per month at a 6% yield.

Now that we have $48,000 in our emergency fund, $120,000 in our investment portfolio, and $40,000 in our options account, it’s time to sell some covered calls.

We only want to allocate some of the $40,000 to buy stocks inside our options account. Remember, the more money you have in the markets, the more stress you create.

Let’s look at a stock like Rivian (RIVN). They have a good price and nice “options premiums.” RIVN sells for $14.11. We can purchase 1,000 shares for $14,110.

No Freaking’ Way I Am Working Another 25 Years Part 2

With 1,000 shares, we can sell ten covered calls at the $15 strike price and earn $660. That’s not the $1,000 we desire, but we are in a safe space. We are only using $14,000 out of $40,000.

We can keep the remaining $26,000 in a money market fund or index fund. We can even try a covered call ETF like JP Morgan Equity Premium Income (JEPI).

Social security + covered calls. Selling covered calls gives you financial options outside of a receiving government check.

As you can see, it takes a lot of money to trade options safely. Most people will never view money as an asset to exploit.

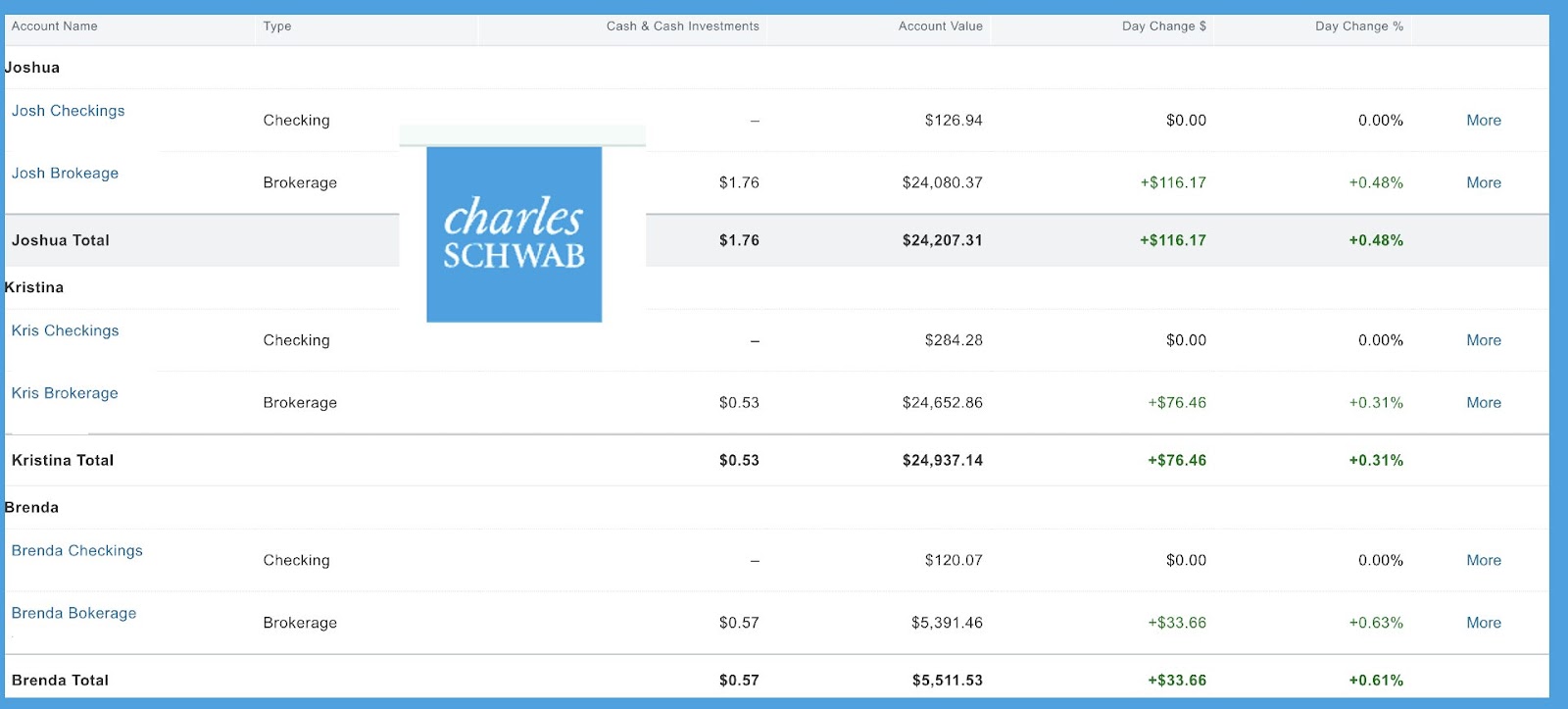

Here is a picture of my options trading portfolio, split between me, my wife and my mom. We all have brokerage accounts linked to checking accounts (and debit cards).

I can generate a large amount of money from dividends, covered calls, cash-secured puts, and long strangles. I can then transfer that money to my options trading debit card and spend it. I can create my own income whenever I choose.

A Life Worth Living is Worth Recording

Conclusion. I have been studying options trading and dividend investing for five years and learn something new daily. You always want to keep learning.

Trading options may sound daunting, but life is full of challenges. The average person should avoid trading options at all costs; they are better off renting a room.

However, if you are reading this, you are not the average person. I cleared $15,000 in profit as a part-time options trader. I never had more than one trade going at once.

If you put the proper controls in place, you can seriously make as much money as you desire. You don’t want your resources tied into one stock. If my 1,000 shares of RIVN tank by 50%, I cannot sell covered calls until they recover.

Inflation Ate My Paycheck 102

However, I would still have $24,000, which I could use to sell cash-secured puts or invest in dividend-paying stocks while I wait.

Life is about cash flow and options. Social security should be one of many passive income streams you create for yourself and your family.

Learn how to make your money work for you now. Don’t wait until you are financially vulnerable to start trading options; it’ll be too much of a risk.

If I can trade options, you can too. The most challenging part is understanding the context of where your options portfolio sits in your broader income plan. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply