How is your retirement looking? Do you have cash flow that also increases with inflation? Do you depend on the government to supplement your 401K with social security?

How much money do you need the day you retire? Does that amount look the same 20 years into retirement?

Retirement is a sensitive subject for most Americans. It’s hard to say that you did not prepare for the most crucial part of your future.

The Magic of Income Investing

How did we get here? In 1978, Congress passed the Revenue Act of 1978, which created the 401K. At that moment, Americans became responsible for their retirement planning and saving.

Up until then, companies and governments would give long-term employees pensions. These pensions would provide income, healthcare, and inflation protection.

Pensions are extremely hard to come by today, mainly only used in the military and government sectors. So, how are Americans doing with planning their own retirements? In a word—horrible.

School doesn’t teach us anything about financial education; thus, the 401K program is more a savings account than an investing solution. Many people contribute to the 401K with no knowledge of the stock market or basic investing principles.

The Magic of Marriage

How does the traditional retirement look? Let’s look inside an above-average retirement. The Coopers have $500,000 in 401K savings. Each will receive $2,500/month in social security benefits at age 66.

They paid off their mortgage and cars right before turning 66. Using the 4% rule, they can withdraw $20,000/year from their 401K. That amount equals $1,666/month in income (they must still pay taxes).

So in total, they will receive $6,666 in social security and 401K income. Their expenses total $3,000/month between utilities, adult children, and vacations.

Vacations for the win. Remember, the Coopers worked from age 18 to 66. They grinded away their youth so they could enjoy their late years. Now, how much can they enjoy life with $6,666/month in revenue?

More Content, More Cash Flow

Let me be clear—the Coopers are better off than 90% of Americans. They have income, social security, and a paid-off home. They are intelligent and not mega spenders. But do you think they can travel a lot with this nest egg?

The problem with the unknown. The problem with retirement is the unknown. Since the Coopers spent their adult lives working, that is the only way they know how to earn money.

Once they stop working, they will be fearful of the future. If an emergency happens, they can no longer work to close the gap in their emergency fund.

Renovate & Rent vs. Fix & Flip

The chances are that they will remain in their homes, living in scarcity, and apprehensive of the future. They want to ensure that their 401K will last them until the end. They also want to leave a little to their children if possible.

Dividends equal abundance. On the opposite end of the spectrum are dividends. Dividends bring abundance into your life—allowing you to improve your circumstances.

Let’s look at an alternate reality for the Coopers to ascertain how dividends could supplement their $6,666 retirement.

At age 40, they read the fantastic book “How We Plan to Retire on Dividends 2 (pdf)” by Joshua King (yours truly). With this newfound motivation, they decide to rent a room in their house for $800/month to fund their income portfolio.

Passive Income in DeFi 105: Crypto Rewards

Their goal is to reach $2,000/month in dividend income and stop renting their room and investing in dividends.

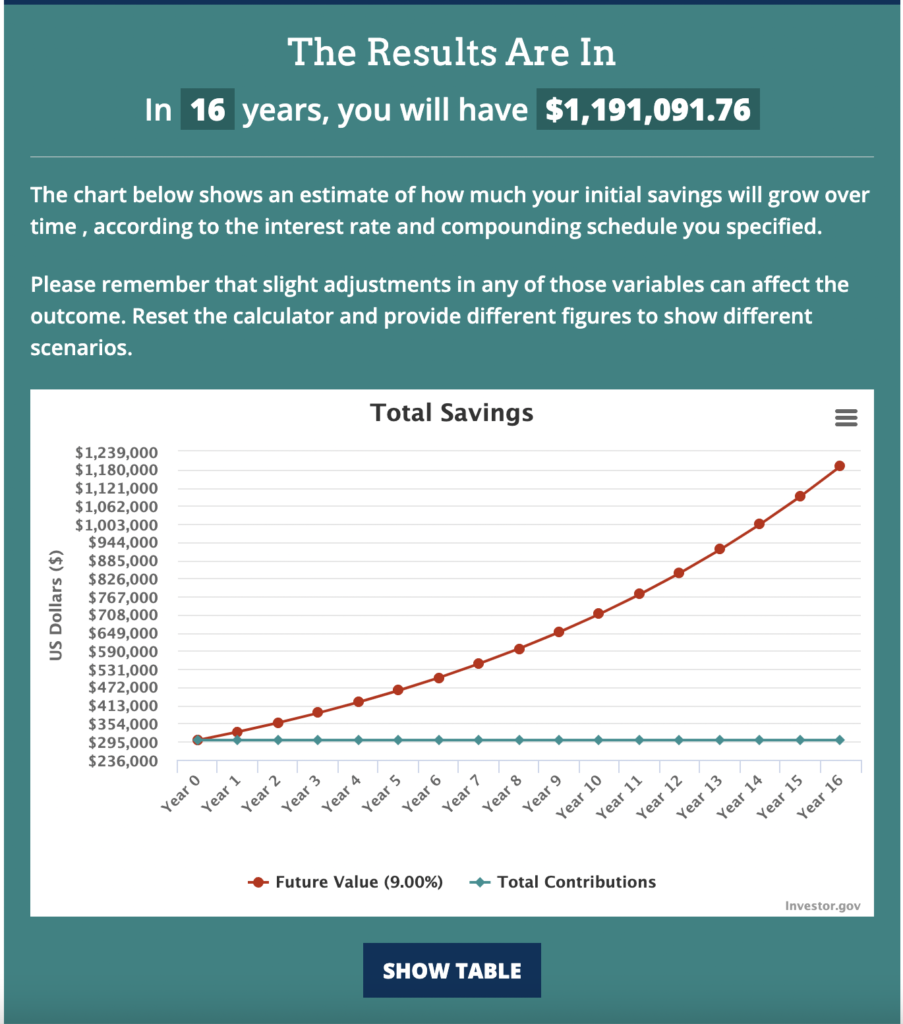

It takes the Coopers roughly ten years to reach their goal of $2,000/month in dividend income inside their income portfolio. Their total portfolio is approximately $300,000 and consists of mortgage REITs, business development companies, high-yield blue-chips, closed-end funds, and preferred shares.

Dividend Growth Investing vs. Income Investing

The magic of dividends. Thus at age 50, the Coopers have an amazing additional income stream. They completely stop renting rooms and investing in dividends. Do you know what happens to their income portfolio? It continues to grow and compound.

From age 50 to 66, at a 9% return, their $300,000 portfolio climbs to $1.1 million. More importantly, it would produce $108,000/annually or $9,000/monthly income.

You read that right. Yes, they would have created an income stream of $9,000/month for their retirement. They lived below their means for ten years, and now they have more income coming in than they can spend.

We Make $650/month in Passive Income

That’s impossible. “That’s impossible!” you say. Well, it’s not. It’s actually pretty straightforward. My wife and I are very similar to the Coopers. Luckily, we stumbled upon dividends at age 38.

We have amassed $200,000 in our dividend growth and income portfolios over the last three years. We are currently getting a yield of roughly 6%. I am age 41, and we have close to $1,000/month in dividend income.

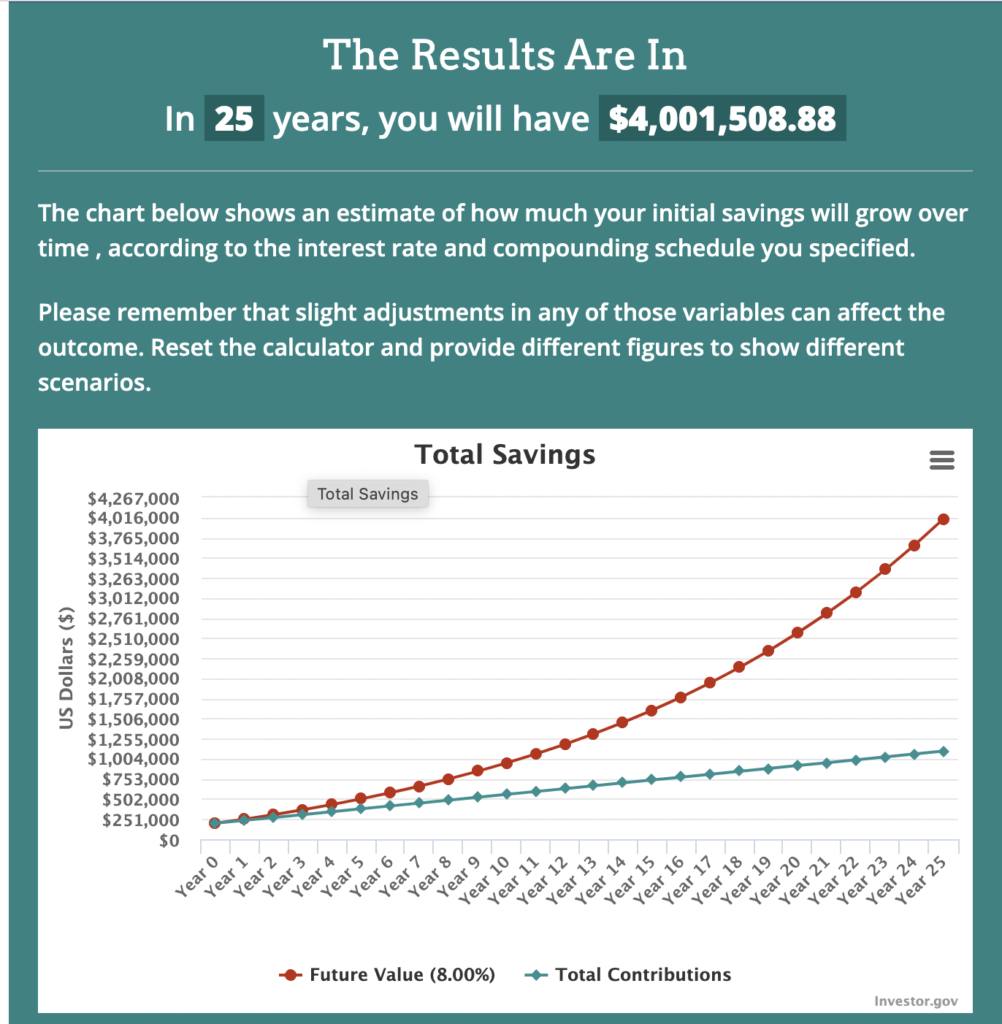

Let’s be extremely conservative and say we invest $1,000/month from now until age 66. We will give ourselves a 7% yield. That gives us $1.8 million, with an income of $10,500/month.

Our more likely scenario is investing at least $3,000/month until age 66. Let’s step up our yield to 8%. This gives us $4 million, with an income of $26,000/month.

Living Overseas Passively on Rental Income

Dividends to the rescue. Do you see the magic of dividends? The best part is that you can use your dividends between 40 to 66. The government doesn’t lock them behind the 401K or social security age restrictions. You can use them as a safety net, pay for vacations, or fund college.

The moral of the story is to start building dividends now for a beautiful supplement to your retirement. Building a dividend portfolio works best when you can increase your savings rate.

Pumpkin Spice & Royalties

The best way to increase your savings rate is to create an additional income stream. In our example, the Coopers started house hacking. What if they continued house hacking from age 40 to 66, and the rents increased 3% every year?

What if they built a dividend income stream of $10,000/month, plus had a room rental of $2,000/month as well? Do you see the power of thinking outside the box?

Conclusion. To get the retirement of your dreams, you’ll have to live below your means. (Hey, that rhymes). You’ll have to do things differently from your friends and family.

My 60-Day Pre-Retirement

The “dividend snowball” is real, and it moves faster than you can imagine. We started three years ago with our first month of dividends yielding $0.25 (25 cents). Next month, we will get a dividend of over $1,000. How crazy is that?

Again, I am only 41 years old. Can you imagine what our dividends will look like when we are 66 or 76? You, too, can jump on the dividend train to supplement your retirement. Chances are, your dividends will completely eclipse your other retirement plans. Hey, life is incredible!

- PDF of the Month: Don’t Gamble with Retirement 6 (Free 409-Page PDF)

- Free PDF Downloads: Download FREE PDF books here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 5 (Free 431-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 54 Takeaways from 54 Books (book)

- Writing: Can Grammarly Make You a Better Writer?

- My Favorite Chromebook: The Ultimate Chromebook (direct)

- Follow us: On our Facebook Page and Join our Facebook Group

- Monthly Dividend Tracker (XLSX): Check it out on Etsy

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply