Where you hold your emergency fund is a deeply personal choice that originates from how you feel about money. Ultimately, it’s about whatever allows you to sleep well at night.

Where you hold your emergency fund also depends on how large of an emergency you can expect or how much risk you can accept. The more questions you ask yourself, the better location you can find that supports your needs.

What is an emergency fund? An emergency fund is a lump sum of money you can use in emergencies, hardships, or unknown situations.

Passive Income Road Trip #6: Royalties

However, we should strive never to use an emergency fund. Its purpose is to prevent us from losing our quality of life, not to save us from things we can predict.

For example, if I have a ten-year-old car, there is a chance it could have some maintenance issues. Therefore, I should start a separate maintenance account for my vehicle.

The same goes for owning a home. If I know my roof is fifteen years old, I should prepare to pay for that by creating a home maintenance fund. I don’t want to wait until the roof collapses and use my emergency fund.

The more you try to keep the integrity of your emergency fund, the better solutions you will devise in the real world. Again, it needs to stay intact so you can sleep well at night.

Start a Tutoring Business Toward Passive Income

How much do I need in an emergency fund? You should strive to keep one to two years of expenses in your fully funded emergency fund.

However, you won’t just arrive at this number overnight. You can build it in steps throughout the years. First, start with your first $1,000, as Dave Ramsey suggests.

From there, you can build up to $10,000 (what I call the Elite Savers of America). Finally, you should aim to get $50,000 to $100,000 in your emergency fund.

Where should you invest your emergency fund? We have to be careful when we use the word “invest.” Your emergency fund is not a financial investment. It is an investment in your quality of life.

Advertising vs. Content Marketing

But we also don’t want $50,000 or $100,000 sitting in a standard savings account. We must find a happy medium between safety and yield. That’s where today’s discussion comes into play.

Let’s look at some choices for emergency funds. Ultimately, you will use a combination of these sources to build yourself a high-yield emergency fund.

- High-Yield Savings Account

- Certificates of Deposit

- Series “I” Savings Bonds

- Series “EE” Savings Bonds

- Treasury Bills

- Tax-Free Money Market Funds

- 30-Year Treasury Bonds

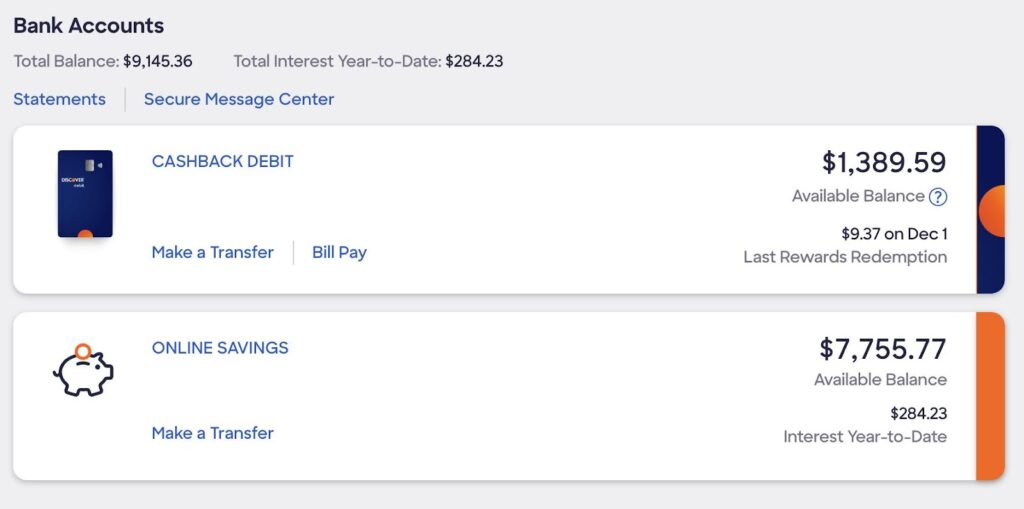

High-Yield Savings Account. Opening a high-yield savings account is your first step to building an emergency fund. I opened my Discover HYSA in June 2019 when I became serious about getting my finances together.

HYSA’s pay rates are very close to the Federal Funds Rate. For example, the Federal Funds rate is currently 5.25% (December 2023), and Discover pays me 5.10%.

My standard Wells Fargo savings account pays me 0.10%. Your HYSA will do a far better good of compounding your money than a traditional bank account.

The Magic of CD Ladders

Most HYSAs are from online banks. They don’t need the physical infrastructure to support their business so that they can pass the savings on to online customers.

You can attach a checking account to your HYSA, allowing you to withdraw your money within minutes of an incident. The Federal Deposit Insurance Company (FDIC) insures HYSAs up to $250,000.

Certificates of Deposit. Physical and online banks offer certificates of deposit (CDs) with high-interest rates when the FFR is high.

CDs ask you to hold your money with the bank for a specific period. For example, the highest yielding CDs are usually 9-month or 12-month.

If you need to withdraw your money sooner, you usually forfeit some of the interest you have accrued. The FDIC insures CDs up to $250,000.

Series “I” Savings Bonds. One of the best products in the world of savings is the Series “I” Savings bonds. You can purchase them directly from the US government.

Staying Debt-Free in Your 20s

The US government will pay you interest on these bonds for 30 years. They index the interest rate to inflation to ensure your money is outpacing inflation, even if just by a little.

The interest payments stay inside the bond, so you will only pay taxes once the bond matures or you redeem it.

The primary issue with Series “I” Bonds is a $10,000 annual limit. However, that is $10,000 per social security number, so you can start investing for your kids early.

Series “EE” Saving Bonds. These bonds are similar to Series “I” Bonds but have one major twist. The government guarantees your Series “EE” bonds will double in value in 20 years.

From Dirt to Dividends: Gardening & Preferred Shares

My rough math equates to roughly a 3.5% annual interest rate—which is pretty darn good for a risk-free investment. They also have a $10,000 annual limit.

Treasury Bills. The US government offers Treasury Bills directly to you at the TreasuryDirect.gov website.

Treasury BIlls come in flavors of 4, 8, 13, 17, 26, and 52 weeks. You can set your Treasury Bills to reinvest into the next treasury offer.

You will earn yields similar to the FFR, but not exactly. Treasury Bills are marketable securities, which means they trade on the open market.

Fitness in the Metaverse

You have nothing to worry about if you buy and hold your Treasury BIlls. If you want to sell them early, you’ll be at the mercy of the bond market.

If you need your money to be liquid (readily available), you can stick with 4, 8, and 13-week variants.

The FDIC doesn’t insure treasury bills; however, you don’t need to pay state tax on these products. HYSAs and CDs are both open to taxation by the federal and state governments.

Start a Passive eCommerce Business

Tax-Free Money Market Funds. Money Market Funds are mutual funds that trade on the stock market. However, they use government bonds to keep their value at one dollar.

If you have a brokerage account, you can find a mutual fund that is right for you. The tax-free variant will pay less interest but also shelter you from paying federal and sometimes state taxes.

If you have a large sum of money you want to hold tax-free, money market funds may be the answer. Remember, the FDIC does not insure these funds.

30-year Treasury Bonds. Investing In 30-year Treasury Bonds can be risky. If the rate on your bond is less than the FFR, you could be in trouble if you sell early.

Read These 10 Books BEFORE Buying a Home

However, if you have a large sum of money, say $100,000, purchasing Treasury Bonds could be a great way to hedge against inflation.

If you can secure a rate above 4%, you would be in good shape versus inflation. The Federal Reserve aims to keep inflation at 2% annually. Therefore, buying some 30-year bonds at 4% could keep you ahead of inflation over 30 years.

30-year bonds would be my last choice to keep my emergency fund, but if rates go back to near zero (like they did for 13 years), having these bonds could be your saving grace.

Putting it all together. How do you combine and allocate your emergency fund using all these tools? The easy answer is that it is entirely up to you. Let’s look at how I keep my emergency fund.

- High-Yield Savings Account – $7,700

- Certificates of Deposit – $0

- Series “I” Savings Bonds – $5,000

- Series “EE” Savings Bonds – $2,000

- Treasury Bills – $0

- Tax-Free Money Market Funds -$5,000

- 30-Year Treasury Bonds – $4,000

- Total – $23,500

Conclusion. How you build your emergency fund is a profoundly personal affair; only you can solve this mystery. Some people like quick access to money, so they use a HYSA as their main savings vehicle.

How We Plan to Retire on Dividends 2

I like to use my credit card for unexpected events because I force myself to pay it off quickly. I only used my HYSA once in 2023, and that was because my retirement pay didn’t come in on time.

If you accept a little more risk, you can keep your emergency fund growing along with inflation. If you value keeping your money safe more than beating inflation, you can stick with your HYSA.

However, once interest rates decrease, your HYSA will no longer be a safe haven where your money compounds. In 2020, my HYSA will go down to 0.4%.

The critical thing to remember is that having an emergency fund puts you ahead of most Americans. You just want to fine-tune it to keep growing, compounding, and building generational wealth for your family. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply