The Investing for Interest Series (101, 102, 103, 104, 105, 106, 107, 108, 109, 110, 111) is one of my favorite series.

I love this series because there is always something new to review or compare in the world of fixed income.

Bonds don’t receive as much love as stocks, but our fondness for bonds grows as we pivot to capital preservation.

Retirement Plus: Use Dividends to Supplement Your Retirement

Today, I want to compare two of the most accessible methods for savings, Series “I” and Series “EE” bonds. Hopefully, you can better allocate your cash after this article.

A quick comparison. Let’s get down and dirty with the facts: Series “I” Bonds help protect your cash from inflation. On the other hand, Series “EE” bonds guarantee your money will double in 20 years.

A deeper look at Series “EE” bonds. I talk about Series “I” bonds all the time, at the expense of “EE” bonds. However, let’s dive deeper today to lay out the facts.

The US government promises to double the face value of your “EE” bonds in 20 years. While you wait, you will earn a small interest rate on your cash. Currently, the interest is 2.1% compared to Series “I” Bonds’ rate of 6.89%.

No Freakin’ Way I Am Working Another 25 Years part 2

For reference, the interest on my favorite high-yield savings account is 3.6%, and I didn’t have to lock up my money for 20 years.

Let’s be honest; Series “EE” bonds are a bet against yourself. The government is betting you will withdraw the cash out before 20 years.

Doing the math on “EE” bonds. Using the rule of 72, what is your interest rate if your money doubles in 20 years? My math shows me an interest rate of 3.5%.

Therefore, holding your “EE” bond for 20 years effectively earned 3.5% on your cash. To be honest, that’s not a bad amount considering you incurred zero risk.

Press Recod: A Life Worth Living is Worth Recording

A risk-free 3.5% -yielding product over 20 years is decent. However, if you pull your money out early, you will incur opportunity loss.

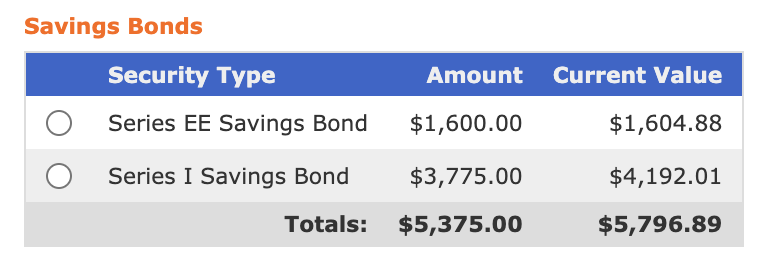

Let’s look at some examples. Luckily, I have invested in Series “I” and Series “EE” bonds so that we can look at the numbers. The best part of math is that numbers never lie.

As you can see, my Series “I” Bonds are destroying my “EE” bonds in the interest I receive. But let’s play the numbers out 20 years from now.

In 20 years, my “EE” bonds will double to $3,200. If my Series “I” Bonds average 2.0% annually, they will reach $5,610—that is not double.

10 Creative Ways to Beat Inflation

For my Series “I” Bonds to perform well, inflation must be very high—which is a catch-22. Series “EE” bonds are guaranteed to perform at 3.5% over 20 years, but the bet is against you.

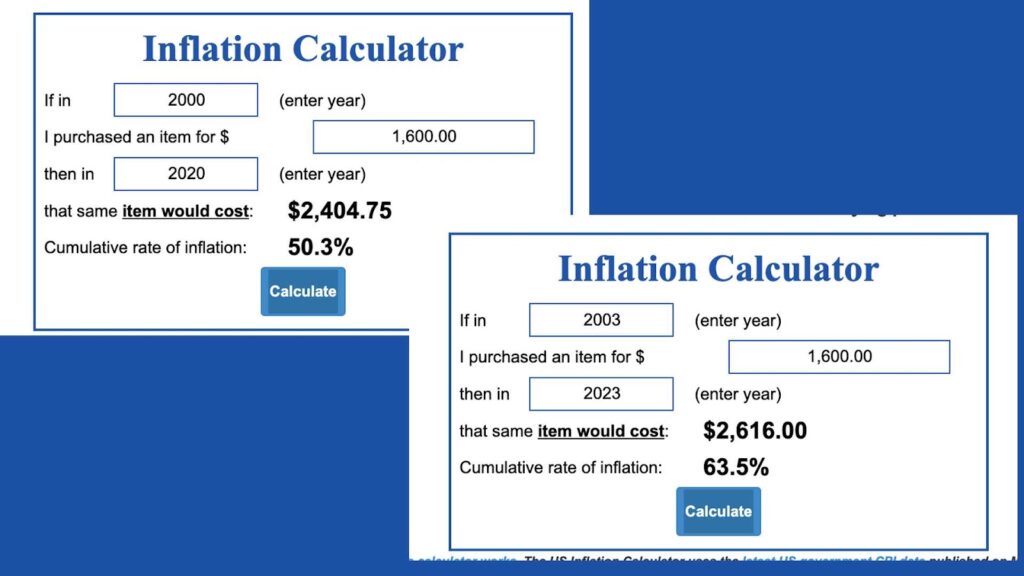

A trip down memory lane. Let’s look at inflation from the year 2000 to 2020, before the pandemic. I will also compare 2003 to 2023 to capture some of the current madness.

As you can see, my $1,600 in “EE” bonds would net me $3,200 in 20 years. That handily beats inflation over both time periods.

Now, with this new bout of inflation, we may not be so lucky. But, an average of 3.5% over 20 years, risk-free, is a good deal.

When to buy “EE” bonds over Series “I” Bonds. It’s hard to recommend Series “EE” bonds over Series “I” Bonds.

You can see the numbers comparing the two. If you have any sort of emergency over 20 years, your Series “I” bonds will be the better performers. It is not even close.

What is Financial Independence?

There is one silver lining with “EE” bonds though—you can purchase $10,000 annually. Therefore, you can buy $10,000 per person per year in Series “I” Bonds AND Series “EE” Bonds.

For a family of four, I can purchase a total of $40,000 per year in Series “I” Bonds and another $40,000 in Series “EE” Bonds. That is $80,000 per year in savings bonds, which is not bad.

A good rule of thumb. If you can max out your Series “I” Bond contributions yearly, I would move into “EE” bonds next.

As cool as “EE” bonds perform, they are like a 20-year certificate of deposit. However, you are not receiving enough interest for an extreme amount of duration risk.

Crypto Investing 101: What Type of Investor Are You?

“EE” bonds for the kids. Series “EE” bonds may be the perfect investment for young children. They will not spend their money until they are in college.

It would be cool to invest $100 per month into “EE” bonds during childhood, then the bonds mature during college at $200 per month.

However, Series “I” bonds still outperform over 30 years because they keep earning interest. After 20 years, the “EE” bonds interest rates reset to the new fixed rate for the last ten years. You have no idea what that will look like until it happens.

Real Estate Investing in Your 60s

Is there a place for “EE” bonds? I believe “EE” bonds are a fantastic, underutilized product. However, you must have a large emergency fund to leverage these effectively.

As soon as you withdraw your “EE” bonds early, you have accumulated a large amount of opportunity cost. You locked your money away at a low rate versus investing in higher-paying securities or accounts.

Series “EE” bonds will be a great addition if you have all your other ducks in a row. However, I wouldn’t make them the main star of your show.

Easter -NEST- Eggs: Build a Dividend Growth Nest Egg

Conclusion. We don’t like when people bet against us. That’s what the government is doing with Series “EE” bonds.

In all respects, Series “I” bonds are the better product simply because they allow life to happen. We have no control over the randomness of life, and locking your money away for 20 years is risky.

The problem is you need to receive more interest for this amount of duration risk. If you have 6-12 months of expenses in an emergency fund and max out your Series “I” bonds yearly, Series “EE” bonds may be an option.

However, at that point, you can invest heavily in index funds, dividend stocks, or income-investing products. If you are hell-bent on investing $20,000 in savings bonds annually, “EE” bonds may be of service. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply