Certificates of deposits used to be one of the safest investments in town. However, we had a troubling turn of events in March 2023.

Three large banks failed in about a week: Silvergate Bank, Silicon Valley Bank (SVC), and Signature Bank. Silicon Valley was the 16th largest bank in America (by deposits).

These bank failures sent tremors through the savings and banking communities. Is your money safe in your regional banks?

Counting on Crypto 2

The Federal Deposit Insurance Corporation (FDIC) and the Treasury Department quickly came to the rescue. They clarified that your money is safe under (and sometimes above) the $250,000 deposit coverage.

Making tough decisions. Still, this tragedy adds another wrinkle to our investing thesis. At the very least, we want to ensure the banks where we purchase CDs are on solid ground.

The conversation between treasury bonds and CDs just became a little more nuanced. We must add the “safety of our principal” to the equation.

Why I Became an Income Investor

Today, I will focus on the five-year variants of Treasury Notes and Certificates of Deposits. Now is a great time to be a saver; however, we must still consider safety, taxes, market forces, and required capital.

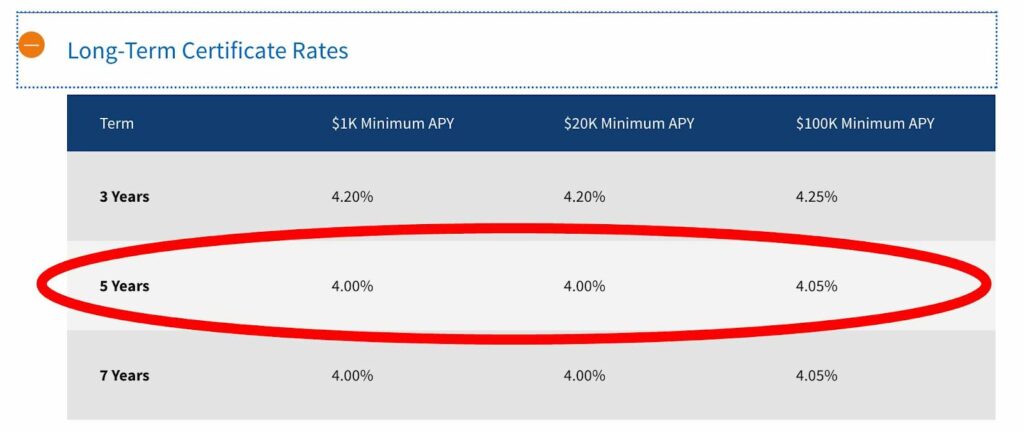

Interest rates are amazing. Let’s start our journey with interest rates. With Navy Federal Credit Union, the 5-year CDs earn roughly 4.00%.

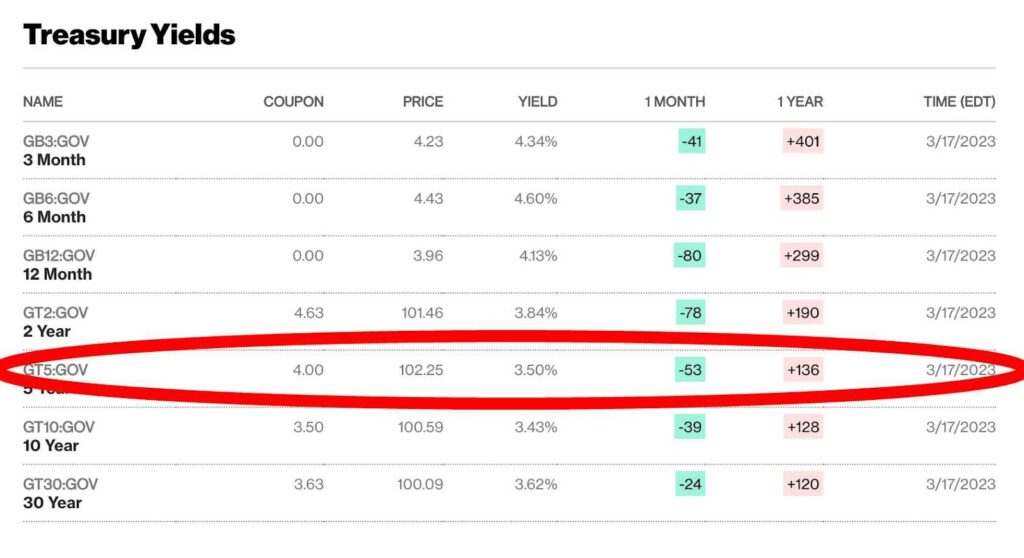

The 5-year Treasury Note yields 3.50% currently, although the coupon is 4.00%. Remember that treasuries trade on the bond market. The coupon and the yield can vary based on the price you pay. This is an important distinction for later.

Safety of principal. Typically, this wouldn’t even be a consideration, but it is relevant in light of recent events.

Your capital is safe if it’s under $250,000 in one bank. You can receive FDIC protection across multiple banks if your deposits stay under $250,000 at each institution.

A High-Value Person: Earns $100,000/year Passively

Pick a major regional bank or credit union, and you’ll be fine. Treasuries are more secure, however. If the federal government needs more money to pay your interest, it will just print more. This is where I insert a sad face emoji.

Required capital. The Navy Federal CD requires a minimum of $1,000—making things interesting. A large deposit can be a burdensome requirement, especially if you want to ladder your CDs.

Treasury Notes require $100 to purchase at auction. However, the auctions only go about once a month. Waiting can be a bummer, as you have to hold your cash until the auction.

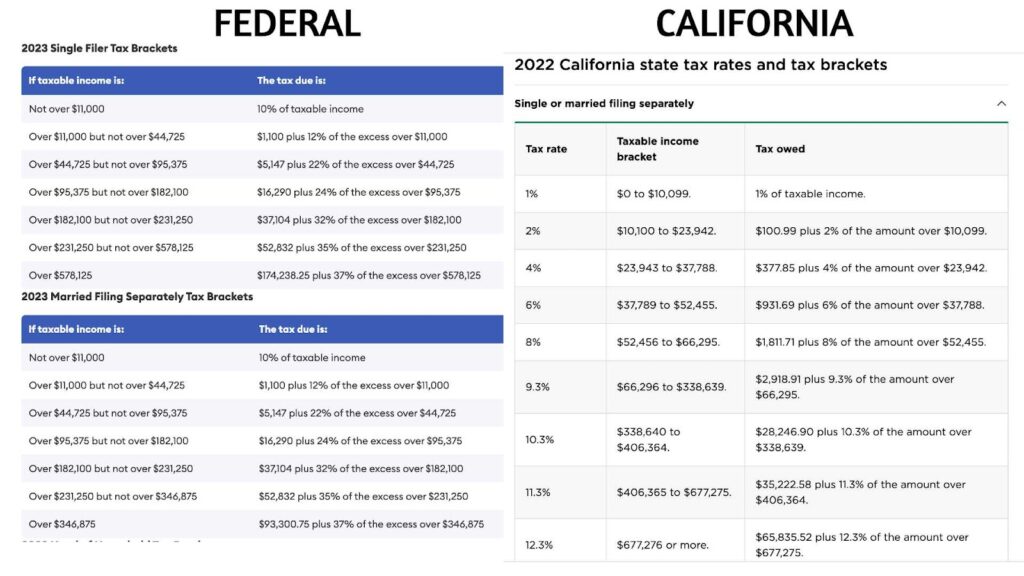

Survey your tax situation. Certificates of Deposit can receive double tax treatment. The federal and state governments can tax them at your nominal tax rate.

The Beauty of Rental Income

This can be a massive hit if you live in a high-state-tax area like California. For example, let’s say you earn $100,000 annually in California.

On a ($10,000) 5-Year CD at 4.00%, you will earn $2,000 in interest. The federal government will tax you at 24% and California at 9.3%. Doing simple math, you could pay $666 in taxes.

Treasuries are exempt from state tax. In this case, this can save you $186. Taxes may play a smaller factor if you live in a no-state-tax area like Florida.

Getting reasonable interest rates. Treasuries trade on the bond market every weekday. You can always buy them from the secondary market if the rates are superb.

Use Dividends as a Safety Net

I do not recommend buying from the secondary market for the average person. You will pay more fees and will need a broker.

If you want to learn more about the nuances of buying from the secondary market, read “The Bond Book.” You’ll learn a lot over the 400+ pages of the book.

Selling at a profit or loss. Certificates of deposit make it easy to get your money early. You’ll keep your principal but lose some interest income.

You could get burned if you attempt to sell your Treasury Notes early. You’ll sell through the TreasuryDirect website at auction. Your bonds could be attractive or ugly to investors depending on the current rates.

You’ll take a loss if you have a 4.00% bond and current rates are 6.00%. If you have 4.00%, and the current rate is 2.00%, you’ll be in heaven.

Transfer of Wealth in the Metaverse

The best way to invest in bonds is to buy and hold. If things take a significant swing in your favor, you may consider selling, but I wouldn’t plan on it.

Making a 5-year commitment. Five-year notes and CDs are the sweet spots between short and long-term investing.

Ensure you have your liquid emergency fund before investing in these products. You want to avoid finding yourself selling Treasuries in an emergency.

For example, I have some horrible 1.6% 30-Year treasury bonds from April 2020. It wouldn’t be pretty if I sold those today in a 3.5% world.

Create an Online Course for Passive Income

Treasuries are more complex than they seem. Everything trades off of Treasuries, so they are vital to the economy and commerce.

Your CD is more of a local hero. It puts in work quietly, without many people noticing. With the recent bank scare, you’ll need to do a bit of research on your regional or online bank.

Conclusion. Five years is a long time for most people. However, it is the sweet spot for locking in good rates.

Your First Five Dividend Stocks

5-year CDs and Treasury Notes can serve as the top or bottom of your ladders, depending on your investing window.

I love long-term, buy-and-hold investing. I would use 5-year Treasury Notes as my lowest duration products.

I would buy 5-year Treasury notes over CDs because I heavily invest in the TreasuryDirect ecosystem. I have all my 30-Year, Series “I” and Series “EE” Bonds in this portfolio.

If you don’t have a massive presence in TreasuryDirect and aren’t concerned about state taxes, you may find CDs a better choice.

Whichever you choose, you are investing in yourself and your family. You could have easily spent this money on something more entertaining, but you chose wisely. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply