The average person avoids the stock market like the plague. Too many horror stories exist about people losing it all gambling on the stock market.

Investing in the stock market has become a limiting belief, but wonderful alternatives exist.

When the stock market tanks, you will want some assets that can still perform well. Today, I will look at two of these alternative investments: Fundrise and US Treasuries.

Are You a Spender or a Saver?

What is Fundrise? Fundrise (affiliate link) is a crowd-funded Real Estate Investment Trust or REIT. If you need to learn more about REITs, check out my introductory series (Part 1, Part 2, Part 3, Part 4, Part 5).

Fundrise differs from most REITs because it doesn’t trade on the stock market. You invest directly with the company; then, they invest in a real estate portfolio on your behalf.

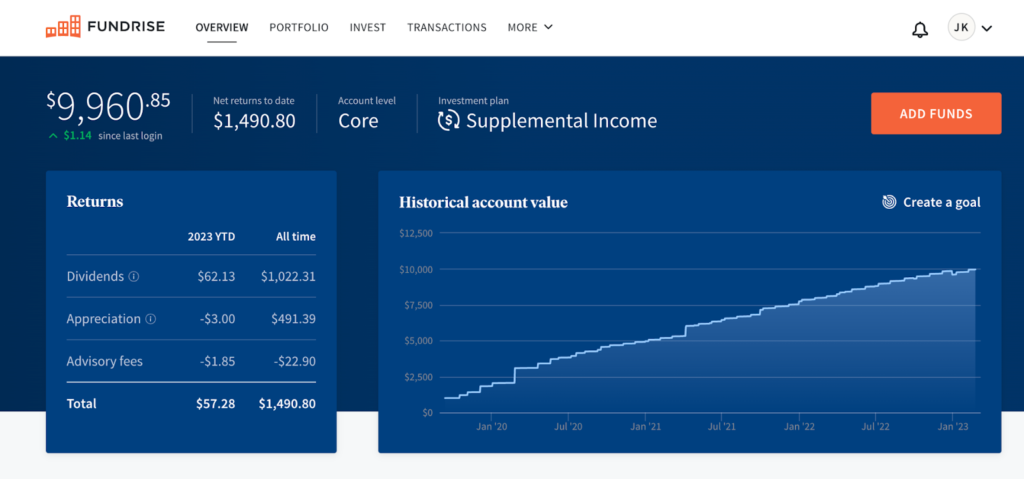

My history with Fundrise. I bought into the company with $1,000 in September 2019. I also bought shares in the company. If the company goes public, my shares might land me a windfall.

I have close to $10,000 in my Fundrise accounts. To be honest, I rarely talk about Fundrise because it is just a solid, quiet performer.

Bond Investing in Your 30s

For the most part, it slowly appreciates upwards. There will be some turbulence because of flux in the housing market, but I expect this behavior.

It is easy to automate your Fundrise investments; I invest $150 per month. They automatically reinvest the dividends, so you don’t need to review your account too often.

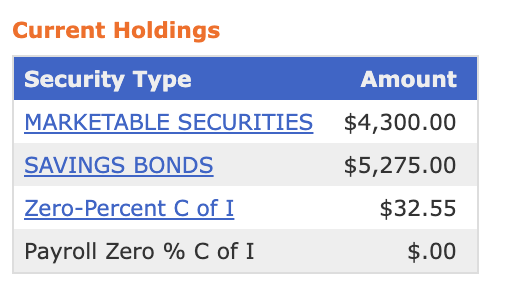

The magic of US Treasuries. The US Government calls the bonds they issue US Treasuries. There are many types of US Treasuries ranging from 1 month to 30 years.

I also like including savings bonds under the US Treasuries umbrella, but that might be hearsay. Between savings bonds, Bills, Notes, and Bonds, you can have your fill of Treasuries.

Bond Investing in Your 30s

Treasuries on your portfolio. You can find the securities that match your need for growth or yield. Series “I” Bonds don’t produce income but compound onto themselves and adjust for inflation. These bonds are genuinely fire-and-forget savings instruments.

Bills, Notes, and Bonds will pay you semi-annually. Currently, the yields are excellent on Notes (from 2-10 years), with most over 4%.

I prefer 30-year bonds because I want to lock in great yields for a lifetime. Again, if you have more time, you can trade 1-year or 2-year Treasuries to your heart’s content.

Many investors jump into short-term treasuries to earn yield while the stock market bleeds. I am a buy-and-hold investor, so I invest for the long term—to each their own.

Create Content Daily 2: The Magic of Compounding Creativity

Fundrise vs. US Treasuries. The money you have to invest can be tight during a recession, so you must choose wisely. You can’t go wrong with either of these securities, but let’s ask some questions to dig deeper.

How long can you lock up your money? If you only want to lock up your money for two years or less, then Fundrise is out of the picture.

Real estate is an illiquid investment, meaning it takes a while to extract your cash. Think of investing in Fundrise as buying a house.

Treasuries offer much shorter timeframes with much higher yields. These will serve you well in the short term.

Financial Independence through Real Estate 4

If you are looking at a 20-year investment horizon, Fundrise, Series “I” Bonds, 20-year, and 30-year bonds are right up your alley.

Do you love automated investing? Both TreasuryDirect and Fundrise offer fantastic automatic investing options. I automatically invest $150 in Fundrise, $100 in Series “I” Bonds, and $200 in 30-Year Bonds.

Do you need cash flow? Treasuries and Fundrise have great options if you are investing for income. You can receive quarterly dividends (Jan, April, July, October) from Fundrise.

You can receive semi-annual interest payments from your Treasuries (February and August)(May and November) which, depends on the month you buy your Treasuries.

The Bear Market is Your Friend

Are taxes an issue? You can find safety inside both securities if you want to reduce your tax bill. Fundrise offers traditional and Roth IRA options.

The US government offers Series “I” Bonds and Series “EE” Bonds which compound tax-free until maturity in 30 years. You pay taxes at the end on your capital gains.

You can also prevent paying taxes on Series “I” Bonds if you use them for qualifying educational purposes. With the other Treasuries, you will pay taxes on interest payments based on your tax bracket.

Which is better for the long term? US treasuries have been around for a long time. Investors consider US Treasuries no-risk investments, and today you receive over 4% interest. This is a fantastic setup and something everyone should leverage.

Investing for Interest 110: Bond Buying is Back, Baby!

Fundrise started roughly 11 years ago. You never know what the future holds, but investors receive higher gains for higher risk.

It’s a tough real estate market currently, so Fundrise may give you a chance to jump into real estate investing without getting burned.

Fundrise offers multiple investing strategies; I choose the dividend-centric model. However, you can invest in capital-gains-focused portfolios as well.

Live Your Best Life with Dividends

Long-term, we know real estate will continue to appreciate. You will always want to have physical or paper assets invested in real estate.

Conclusion. I invest in both products. I mainly chase yield on the stock market through income investing. However, I don’t want to put all my eggs in one basket.

You can’t go wrong with automatically investing in each of these investments. If I had $400/month to invest, it would go like this: $100 to Fundrise, $200 to Series “I” Bonds, and $100 to 30-Year Bonds.

Saving for a House Down Payment #6: Family, Big City

This gives me growth and income and allows me to grow with the real estate markets. I am a massive fan of Fundrise because it is super simple.

Getting started on TreasuryDirect can be a bit more cumbersome, but spending the hour learning is worth it. Here is my guide to investing in bonds on TreasuryDirect.

You may have to step out of your comfort zone on these products, but that’s why I am here. I already did the heavy lifting (testing); you just need to press the buttons. Good luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply