The most challenging aspect of becoming financially independent is making the leap from a saver to an investor. It’s nearly impossible to save your way to financial freedom.

As much as we love the comfort of having our money in savings, earning 3-4% on your cash won’t net you enough to retire.

How do we leap from being a saver to becoming an investor? The most critical juncture is reaching the high point of savings (Series “I” Bonds) to dropping to the lowest risk investment vehicles (index funds).

What Limiting Beliefs Do You Have About Money?

The magic of Series “I” Funds. Congratulations if you have bought a Series “I” Bond. You have done more toward your financial well-being than most will ever achieve.

Series “I” Bonds allow the government to grow your money along with inflation. There are two main issues with Series “I” Bonds: annual limits and taxes.

The annual limit you can put into Series “I” Bonds is $10,000 per TreasuryDirect account. You will need to invest much more than this to become financially free.

Additionally, when you redeem your bonds, the government taxes your (interest) capital gains at your overall income level (10-37%). You CANNOT purchase Series “I” Bonds in a traditional or Roth IRA.

The Pros and Cons of Dividend ETFs

The magic of index funds. Index funds allow the American economy (vice the government) to grow your money along with inflation.

In most cases, your money will grow above inflation when investing in index funds. However, your index funds will take a beating when the economy dips into a downturn or recession.

There are no annual limits on index funds in a standard taxable brokerage account. You can also invest in index funds inside a Roth IRA, giving you the ability to avoid capital gains taxes.

Even better, you can borrow against your index funds with a brokerage like M1 Finance (affiliate). This way, you don’t have to sell shares and can take a loan at 3-6% (depending on the Federal Funds Rate).

The Magic of Cryptocurrencies

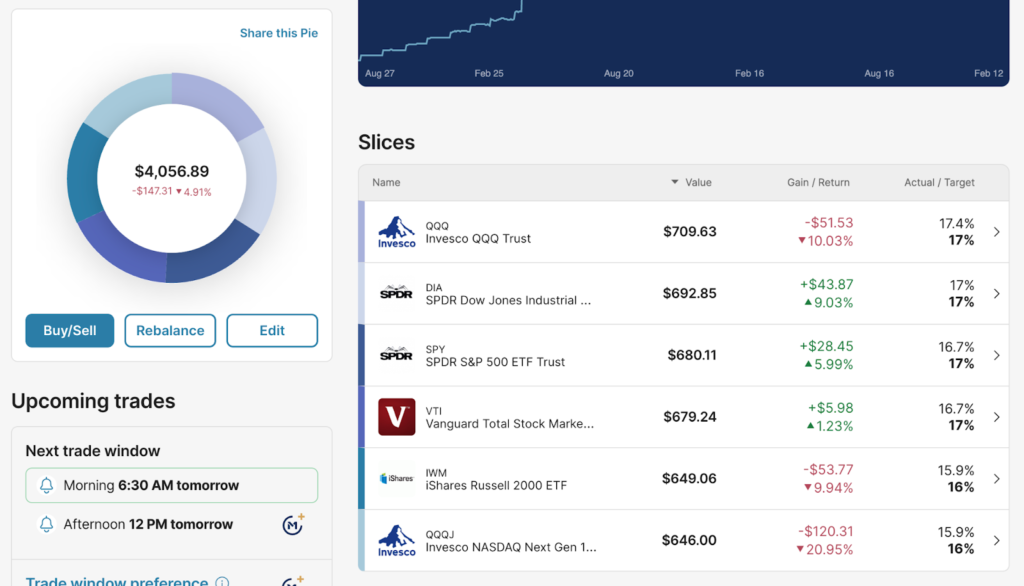

In my M1 Finance pie above, I have $4,000 in index funds. I can borrow roughly $1,500 against this amount at 6.5%. Much better than the long-term capital gains rate of 15% or 20%.

Making the leap to index funds. How do you go from buying bonds on the TreasuryDirect website to investing in index funds? The short answer is slowly.

The best way to purchase index funds is by dollar-cost averaging. I recommend starting with a “starter” brokerage like the STASH app (affiliate) because they will hold your hand along the way.

Don’t Gamble with Retirement 4

Just download the app, answer the mandatory investment questions, add a checking account, and set up a weekly (say $5) amount to invest.

Remember, I recommend four index funds above all: Total Stock Market (VTI), S&P 500 (SPY), Nasdaq 100 (QQQ), and Dow Jones Industrial Average (DIA).

Will you lose money in the stock market? Perhaps the question I hear the most is, “Will I lose money in the stock market?”

The answer is yes—if you lack conviction. This statement means you’ll need to understand why you are investing in the stock market.

Why Gold & Silver?

Let’s compare 30 years between Series “I” Bonds and index funds. We will give the Series “I” Bonds a 4% annual return and the index funds 9%.

Comparing the bonds and index funds. Let’s see if we invest $10,000 into each category for 30 years. I like to use the Investor.gov compound interest calculator.

The Series “I” Bonds total $32,400, while the index funds give us $132,600. It’s important to understand that the Series “I” Bonds stop compounding after 30 years.

If you continue to let the index funds compound until 50 years, you are looking at $743,500. That’s the power of compound interest.

Can You Live the Laptop Life?

What if you invested $10,000 at the start of your grandkid’s life? At age 65, they would have $2.7 million.

Use both Series “I” Bonds and Index funds in tandem. These securities work better together because they serve two distinct purposes.

Series “I” Bonds work great in Tier 2 ($10,000) and Tier 3 (six months of expenses) emergency funds. You keep these on hand, so you don’t have to liquidate your index funds in an emergency.

Series “I” Bonds allow you to sleep peacefully at night, while index funds will enable you to enjoy your daytime.

Mortgage Positive: Make Cash Flow from Your Primary Residence

Don’t get caught in the minutiae of daily stock market investing. If you wait for bad news, you’ll be on-hinge every day.

Simply put, fear sells. It is easier to get your attention with bad news than with good. If you become overly concerned with stock market news, you’ll sell your index funds instead of doubling down and buying more.

Can you make the leap? Most people need help to make the leap from consumer to saver and saver to investor. Congratulations on at least reading about the process.

I leaped broke to saver to investor in two weeks. I simply became fed up with having debt and struggling financially. My family deserved better from me, and I decided to step up and become a great provider.

You’ll Need $20,000/month in Passive Income

Conclusion. How has it all worked out for me? I have no consumer debt, and we have $300,000 in savings and investments.

Most importantly, we don’t worry about the future. My wife and I will retire this year—both under the age of 43.

I wouldn’t be able to retire early with just Series “I” Bonds. However, I wouldn’t be able to retire comfortably with just index funds.

Pay for College with Real Estate 104: Cash-Out Refinance

Savings are for today, and investments are for tomorrow—debt is a product of the past. As you pay off debt, think about today and tomorrow.

I understand that it is terrifying to place your money in the markets; however, it’s also scary to retire on a fixed income.

If you want to live the lifestyle of your dreams, you’ll have to build it—brick by brick. Series “I” Bonds and Index Funds are part of your solid financial foundation. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply