A few improvements to investing have changed the game for the average middle-class investor. These are fractional shares, zero commission fees, and automated investing.

Today, we can invest $5/week into our favorite index funds and dividend ETFs to slowly grow our portfolio. Plus, we can still go all in with $5,000 when we get our annual bonus.

So, it’s easier to invest than ever before; what’s the problem? There are more choices at our fingertips, which can leave many people with analysis paralysis.

Staying Debt-Free in Your 60s

Why are you investing? We invest in index funds and dividend ETFs for two completely different reasons; therefore, we must understand our long-term goals before choosing.

We invest in index funds to grow our portfolio quickly with the market. Most of your gains will be from capital appreciation (roughly 8% gains, 1.5% dividends). The end state is you selling shares of your index fund to generate income.

We invest in dividend ETFs to grow our income. Most of the gains will be from capital appreciation, but a significant portion will come from dividends (roughly 5% gains, 3.5% dividends). The end state is us keeping our shares and living off of the dividend income.

Advertise Your Books for Free

What are your financial goals? Do you have a plan to reach $1 million in ten years? Or do you aim to reach $40,000/year in dividend income?

If you aim for a large pot of money, index funds will get you there the fastest. Many F.I.R.E. (Financial Independence Retire Early) advocates push index funds on their followers.

It sounds sexy to reach $1 million before you turn 30 and retire. There is only one problem—you will start selling shares immediately.

Let’s say you start with 5,000 Vanguard Total Stock Market Index Fund (VTI) shares. To achieve $40,000 in income, you would need to sell 200 shares.

Staying Debt-Free in Your 50s

The following year, you would start with 4,800 shares of VTI. The problem is using the “hope” strategy.” You will hope (and pray) that the market increases enough to boost your 4,800 shares back to $1 million overall.

Index fund dividends. Can you imagine doing this charade from age 30 until 90+? It’s not a game I would want to play. Index funds do pay dividends, but not enough to support a lifestyle.

VTI currently has a yield of 1.58%. Your $1 million would pay you $15,800 per year or $1,316 per month—not a very comfortable retirement.

5 Takeaways from “Manage Your Day-to-Day”

More dividends, fewer problems. Now, let’s say our goal was to achieve $40,000 in dividend income before we retire.

This will take longer than using index funds and the capital appreciation method. The main difference is you wouldn’t be selling shares to produce income.

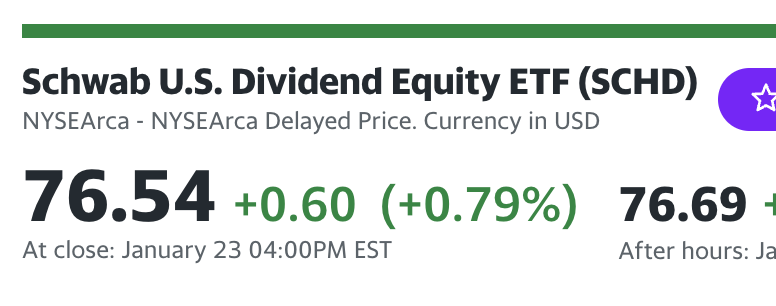

Your portfolio would pay you. One of the most popular dividend ETFs is Schwab U.S. Dividend Equity ETF (SCHD). It currently has a dividend yield of 3.37%.

We still get capital appreciation. A central point of investing in dividend ETFs versus closed-end funds is that dividend ETFs still offer capital appreciation.

Publish to the Widest Possible Audience

Dividend ETFs usually have a collection of blue-chip dividend-paying stocks like AT&T (T), Verizon (VZ), Johnson & Johnson (JNJ), Kinder-Morgan (KMI), and Pfizer (PFE).

The composition of each dividend ETF is what makes them unique. Some focus on dividend growers like Visa (V) and Mastercard (MA), and others on high dividend-yielding payers like AT&T (T) and Altria (MO).

However, these companies have strong balance sheets and outstanding track records, so they tend to increase over time. That means dividend ETFs will also grow along with these companies.

Dividend ETFs like SCHD also grow their dividend payout over time to coincide with the companies’ dividend raises. Dividend ETFs are great for those who love dividends but don’t have time to pick (and follow) individual stocks.

From Broke to Saver to Investor

You’re missing the high flyers. The biggest difference between dividend ETFs and index funds is growth stocks—or lack thereof.

Many of the fastest-growing stocks don’t pay dividends, including Tesla (TSLA), Nvidia (NVDA), Adobe (ADBE), and Amazon (AMZN).

An index fund that follows the NASDAQ 100 (QQQ) will have these high-flying stocks as its main appeal. They can shoot for the moon or quickly burn in the atmosphere.

Dividend ETFs tend to be more defensive because these older blue-chip companies don’t crash and burn or fly high daily.

Art Edition: The Biggest Book on Passive Income Ever 2!

This scenario means they have a low beta (don’t fluctuate too much). If you want to achieve financial freedom via a large portfolio, QQQ might get you there quickly.

However, don’t be surprised if that number disappears during a rising interest rate environment. Again, it is vital you understand the composition of these index funds and dividend ETFs.

Some dividend ETFs have stringent rules before they purchase a stock. For instance, they may say companies must have 20 consecutive years of dividend payments. A company like Apple (APPL) may not qualify because they haven’t paid a dividend for that long.

Struggle-Mania: 12 Reasons You Love Being Broke

Conclusion. Having choices is always a good thing, but you must be decisive. I invest in index funds (VTI, SPY, QQQ, DIA) and dividend ETFs (SCHD, SPHD, DHS).

I don’t ever expect to sell my shares of my index funds. I use them to balance out my income-investing portfolio.

I use dividend ETFs as growth vehicles because I love high-yielding securities like preferred shares and closed-end funds. Income funds tend to have a flat capital appreciation metric, which dividend ETFs can mask.

However, it is nice to have index funds and dividend ETFs consistently growing along with the markets. With these two securities, you don’t have to follow the news or the markets.

It’s Raining Money: How Dividends Can Change Your Life

They are buy-and-forget style investments. Just understand your long-term game plan before investing.

If you want to retire and sell shares (not recommended), index funds will help you achieve big numbers sooner.

If you want to live on dividend income (income to the moon), then dividend ETFs will give you stable and rising dividends.

You can choose both to have great results via capital appreciation and dividend income. That’s how I like to roll. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply