Today is a great moment in time to be an investor. It’s been over 13 years since stocks and bonds had to compete for your investment dollars.

If you are searching for a 4% yield, you can now choose between a 30-Year Bond or a blue-chip dividend-paying stock.

However, the answer doesn’t lay in numbers; it is a psychological mindset about how much pain you can endure in the markets. Let’s dive into this great topic.

Passive Income: Royalties vs. Automation

Stocks versus bonds over the last 40-50 years. When inflation raged during the 1970s and 1980s, the Federal Funds Rate was over 10%.

This means that savers were receiving certificates of deposits and treasury bonds over 10%. There wasn’t much reason to dabble in the stock market, especially to chase yield.

However, as each new crisis emerged (the dot-com bubble in 2001, the Great Financial Crisis in 2008, and the Pandemic in 2020), the Federal Funds rate (FFR) went to nearly zero.

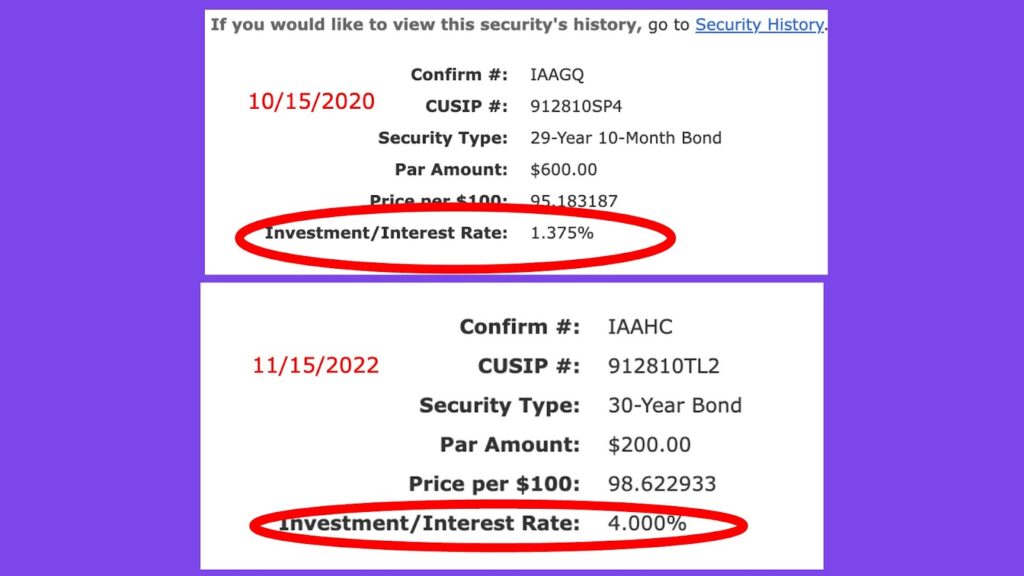

When the rate is that low, the yield on bonds also takes a nosedive. I have a 30-Year Treasury Bond with an interest rate of 1.38% from 2020.

Cash Flow 103: Choose Your Wealth Generator

Of course, with little yields in bonds, investors (and yield-chasers) move to stocks. Growth stocks such as Apple (APPL), Microsoft (MFST), Tesla (TLSA), and Netflix (NFLX) performed well after the pandemic.

Investing for income. However, yield seekers love yield. With bonds as a non-starter, they migrated to blue-chip dividend-paying stocks.

Some of these great stocks are Altria (MO), Phillip Morris (PM), Abbvie (ABBV), Johnson & Johnson (JNJ), Costco (COST), Public Storage (PSA), and Procter & Gamble (PG).

The price increased with so many investors chasing these blue chips for dividends and growth. When the price increases, the yield decreases.

Municipal Bonds: Tax-Free Goodness

With real estate prices also increasing during the pandemic, real estate didn’t offer great returns like during the 2008 Great Financial Crisis.

But things changed in 2022 with the increase of the Federal Funds rate to 4.5%. An FFR over 4% gives savers a chance to grab impressive yields from certificates of deposit, high-yield savings accounts, Series “I” Bonds (because of high inflation), and Treasury Bonds.

The Magic of DGI? So with so many options with zero risk, why would you need to jump into the stock market?

We Make $50/Day in Passive Income

The answer lies in the power of compounding. Dividend growth investing is terrific because of dividends, but there is more than meets the eye.

There are four reasons that make DGI stocks great: (1) dividend reinvestment, (2) increasing dividend payments, (3) stock price increases, and (4) dollar-cost averaging.

Using these four techniques in tandem across 10-20 DGI stocks, you will create a fantastic portfolio that also pays you dividends. It is akin to building a house for rental income.

Don’t count bonds out yet. On the other hand, bonds are boring because they offer fixed income. You can calculate the amount of interest you will receive from the day you buy your bonds.

Mailbox Money: The Power of Rents, Royalties, and Dividends

For example, if I buy a $10,000 30-Year Treasury Bond at 4%, it will pay me (60) semi-annual payments of $200 each (for a total of $12,000) over 30 years.

From the outside, it looks like you walk away with $22,000 after 30 years, but that is only partially the case.

While reading “The Bond Book,” I learned that bond reinvestment is an essential calculation that bond traders factor into their purchasing decision.

Bond reinvestment assumes that you will reinvestment all coupon payments into bonds or other securities that yield as much as your bond.

I Live Paycheck to Paycheck 2

For example, a bond trader would look at my bond above and assume I reinvest the $12,000 in interest into other securities or bonds that yield 4%.

But what if you reinvest those payments into higher-yielding securities like preferred shares, closed-end funds, and business development companies? I call this “High Yield Bond Reinvestment.”

Using simple math, if I reinvested my $12,000 in interest payments at 10%, it would give me a monthly payment of $100. Of course, over 30 years, the power of compounding would make these numbers truly outrageous.

Who do you trust? With bonds and stocks yielding 3-4%, it’s time to decide who you trust. Boring bonds can become exciting with high-yield bond reinvestment.

Run a Property Management Business

DGI stocks offer growth, capital appreciation, increasing dividend payments, stock splits, mergers, and special dividends.

However, DGI stocks take some maintenance and reading to achieve (and maintain) peak performance. You will need to read at least 2-4 hours a week to keep up with your 10-20 companies. Do you trust yourself to maintain good reading habits?

Bonds are fire and forget. You don’t have to spend your interest payments until you want. You can also use your payments to buy Series “I” Bonds or directly deposit them into a high-yield saving account.

Losing Friends? You’re Doing Something Right

Bonds may be your best bet if you don’t trust that a company will be around for 30 years. If you think the US Government will default on your bonds, then the stock market AND treasuries are not for you. You have no faith in the system.

Conclusion. I decided to invest in both DGI and 30-Bonds. I buy roughly $200/month in 30-Year Bonds every month and about $900 in DGI stocks.

However, I read about stocks for about one hour daily. I read books like “The Intelligent Investor” and “Infinity Investing” to ensure I understand buy-and-hold stock market investing.

Pumpkin Spice & Royalties

Bonds can make a run for stocks with high-yield bond reinvestment; however, income investing takes a lot of hard work and education to pull off successfully.

Depending on your situation, a mixture of stocks and bonds can make you feel comfortable during a market crash or recession.

Everyone loves high-flying stocks until they are grounded. I remember looking at my portfolio in March 2020, which was entirely red. However, my bonds looked terrific.

Finally, you can achieve similar results with a dividend ETF like SCHD and a long-term bond fund like BLV. Life is good when you have options. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply