The goal of life is to make money while you sleep; there is simply no other way to get ahead of life expenses. But how do you make passive income?

Some people turn to the stock market to earn dividends while they sleep; others use the options market to create large amounts of passive income.

I use a combination of dividend stocks and options trading to generate passive income. Today, I want to discuss two of my riskier techniques: trading long strangles and buying Mortgage REITs. But first, let’s take a quick dive into how to classify risk.

The 30-Day $1,000 Emergency Fund Challenge

What is risk? I define risk as how much money you are willing to lose. Let’s say I have $10,000 to my name as I head to Las Vegas.

In one reality, I play blackjack with all $10,000. In another reality, I put $9,000 in a high-yield savings account and only gambled with $1,000. Which method is more risky?

As you can see, you control your own risk profile. If you are wise and limit the total amount that you have in the markets, you have a greater chance of success.

These risk mitigation techniques are vital when discussing purchasing high-yield income-investing products like Mortgage REITs or trading long strangles on the stock market. Let’s begin.

Why invest in Mortgage REITs? Most people consider Mortgage REITs too risky for their taste; however, I love mREITs because they trade along the bond markets.

New Car Payments vs. Income Investing

At their core, mREITs are mortgage-backed securities (MBS). Mortgage-backed securities are bundles of home mortgages that banks sell to third parties.

There are many different types of MBS: conforming mortgages (that Fannie Mae and Freddie Mac purchase), non-conforming (jumbo loans), and commercial (office space, etc).

You can find various mREITs to purchase specific MBS to diversify your interests. But my favorite part about mREITs is the income they produce.

Mortgage REITs use leverage to borrow money to purchase mortgages. They then purchase hedges against Treasury Bond prices to protect their downside. It’s very complex stuff, but all you need to know is that they are like massive bonds.

Therefore, you shouldn’t look at a mREIT like a dividend-growth stock like McDonald’s (MCD). They are more akin to a 10-year Treasury Bond.

Living in 1,000 Square Feet as a Family of Four

For this reason, the average person will not want to invest in mREITs. For example, an mREIT may go ten years with no increase in stock price. However, it may have paid 100% of the stock price in dividends.

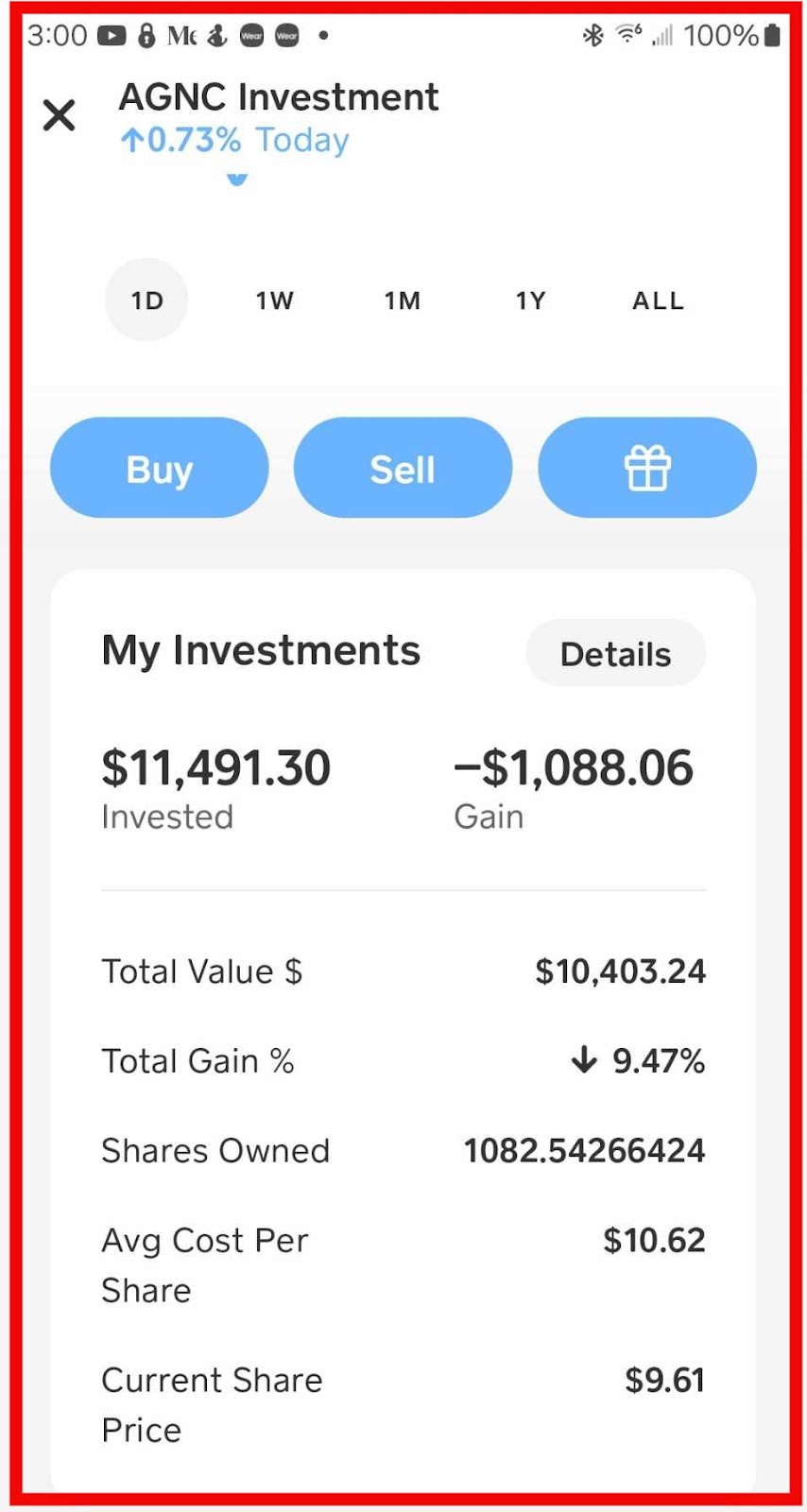

Let’s look at my favorite mREIT position. Inside my Cash App, I have an AGNC position that is $10,403—I paid $11,491 for these 1,082 shares, so I am down 9.47%.

Most people will look at this as a terrible investment; however, this is my favorite stock position in my entire portfolio. Over the last four years, I have collected $2,321 worth of dividends from this AGNC position.

I also know that the stock is down because the Federal Reserve is playing around with interest rates. Once rates come down, my share prices will rise. As I said, Mortgage REITs require a different investing style than standard business stocks.

Becoming an Entrepreneur #7: Generating Leads

Why trade long strangles? On the other end of the spectrum is trading long strangles for passive income. A long strangle consists of buying one call option and one put option to strangle the share price.

Again, here, you are entirely in control of your own risk profile. Let’s take $10,000 and invest in a few long strangles.

The first rule of thumb is only to purchase the amount of options you are willing to lose. So, let’s look at our entire risk profile first.

If you have a $100,000 stock portfolio, you can probably trade $5,000 of your $10,000 options account at once. Conversely, if your entire portfolio is $10,000, you’ll want to trade no more than $1,000 at once.

The 401K Lie: Saving 10% is a Fool’s Errand

You never want to trade 100% of your options account at once, as this will cause much stress and anxiety in your life. Options trading can be an extremely emotional profession.

Let’s say that we decide to trade $2,000 of our $10,000 at once. That means we purchase $1,000 Rivian (RIVN) puts and $1,000 RIVN calls.

My goal is to earn 20% of my playing amount in profits and then sell out of my positions. So, in this case, 20% would mean $400.

When the combined value of my options reaches $2,400, I would sell out of my positions. I would pay my commission fee and gather my profits.

Let’s say I earned $400 every month for an annual yield of 48% ($4,800 / $10,000). That’s an amazing amount of passive income.

Think of Preferred Shares as Gift Cards

Putting it all together. So what do you do with the remaining $8,000 of your options trading account while you trade long strangles?

You can invest that $8,000 in mortgage REITS; however, I wouldn’t recommend it. Chances are that your mortgage REIT shares will be underwater if you need to sell them quickly.

Instead, I would invest the $8,000 in money market funds, dividend ETFs, or index funds. But this raises a good question: How much risk are you willing to take?

Let’s say you have a massive $300,000 index fund and dividend growth portfolio. You decide to create a $10,000 income investing and options trading portfolio.

Renting Rooms to Family Members

With this setup, I can maximize my risk profile. Let’s say I can trade $5,000 per month of long strangles and invest the remaining $5,000 in AGNC, which yields 12%.

My long strangle position could generate $1,000 per month or $12,000 per year. My AGNC position would generate $50 per month or $600 annually.

Together, these two positions would generate $12,600 annually for an annual yield of 126%. Not too shabby. Even better, you can reinvest your long strangles earnings into AGNC to increase your passive income.

Conclusion. It’s important to remember that these are high-risk, high-reward plays. Purchasing Mortgage REITs requires knowledge of the bond markets and the use of leverage.

How to Create, Buy, and Build Assets

Trading long strangles requires patience and strategy. Trading options, in general, is a master class on allocating your position for effective risk mitigation.

This simply means being able to sleep at night. You must know your sleep at night number like the back of your hand. If you have $2,000 in the options trading market and can’t sleep, lower your number.

At this point in my life, I am more of a Mortgage REIT person. I don’t have the need to trade tons of long strangles; I would rather earn $1,000 from renting rooms.

However, I trade the occasional long strangle because I enjoy writing about it and sharing my stories. Therefore, I’ll always keep my toes in the options trading water.

But my favorite financial story of the month is receiving $130 in passive income from my AGNC. Seeing my dividends coming in while I sleep makes me extremely happy. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply