No matter your retirement plans, dividends can help you get there. More importantly, dividends can help you stay there (retired).

Recently, I have read many stories about retirees going back to work because their incomes cannot keep up with inflation and cost-of-living increases. This is sad.

Most people have never learned how to invest for dividends, even though this amazing source of income has been around for over 400 years.

Your Income Should Increase Every Year

It is imperative we take matters into our own hands if we want a successful retirement. You ultimately decide your own fate, and dividends should be part of the conversation.

Why dividends? There are many ways to retire: company pension, government pension, social security, 401 (k), annuities, Roth IRA, and treasury bonds come to mind. Let’s look at some of these more in-depth.

- Company pension– You’ll need to serve many years to earn a pension. Plus, you will be entirely dependent on the company for resources.

- Government pension– The government is a little more reliable than a company, but only a little more.

- Social security– this should be the last option for retirees. Cost-of-living adjustments will not outpace inflation.

- 401 (k)– these accounts rely on the stock market for capital gains. You must also use the 4% to dismantle your account over time.

- Annuities– these instruments require lots of money to generate 3-4% returns, plus you’ll need to pray the insurance company stays in business.

- Roth IRA– These are good sources of tax-free money, but you can only buy in $6,000 per year. Therefore, it’ll be tough to build a $1 million portfolio.

- Treasury Bonds– it would be great to retire on interest from Treasuries, but you would need millions upon millions to be so.

All of these retirement methods have pros and cons, so it’s a good idea to include them in a retirement plan. However, you must dream bigger.

Single Ladies, What Are Your Retirement Plans?

Dividend investing allows you to build a plan that can grow exponentially over time. Even better, you can use dividends to supplement your dream retirement.

When to start dividend investing. You should begin dividend investing when you turn 18 and can open a brokerage account. However, most of us were not that lucky. Instead, you should start investing today.

Dividend investing is perhaps one of the most addicting things one can do for themselves. The sooner you start, the faster you fall in love with the process.

I started dividend investing in 2019 at the age of 38. I have never done something as exciting and rewarding as investing in dividends, and I was a US Marine for 24 years.

I am a retiree (at age 43) and receive a fixed income from the military. I currently receive $9,000 monthly from my government pension and $2,100 monthly in dividends.

I promise you that my dividend income will surpass my pension income in the next 20 years. Why? Because I can control the power of compounding inside of my dividend portfolio. Let me explain.

The Dividend Debit Card

I do not possess the ability to increase the size of my government retirement pension. Every year, the government increases my pension by the same cost-of-living adjustment that Social Security uses.

Typically, this amount is between 2% and 3% annually. Over the next 30 years, I will see a massive bump in my retirement pension.

However, my dividend portfolio will increase exponentially faster than adjustments to the social security cost of living. Plus, I control the narrative within my dividend portfolio.

Dividends versus inflation. There are three ways to increase your dividend portfolio’s income: dividend reinvestment, dividend increases, and adding new capital.

How to Use Credit Cards

Dividend reinvestment is vital to the overall success of your dividend portfolio. At a minimum, you should reinvest 25% of your dividends. However, reinvest your dividends if you don’t need to use them.

I like to keep a checking account or brokerage fund with roughly $1,000. If I need something, I can tap into this cash. I then let my dividends refill this account. Once I am at $1,000 again, the dividends begin to reinvest themselves.

As a dividend investor, you’ll soon learn the magic of dividend raises from the company or fund. Dividend growth investors will see the most dividend increases and capital gains. Income investors will see more supplemental and special dividends.

Dividend increases, along with supplemental and special dividends, will act as a secondary force to push your income over the top each year.

Finally, you can add more capital to your dividend portfolio to increase your income every year. This is perhaps the best part of dividend investing.

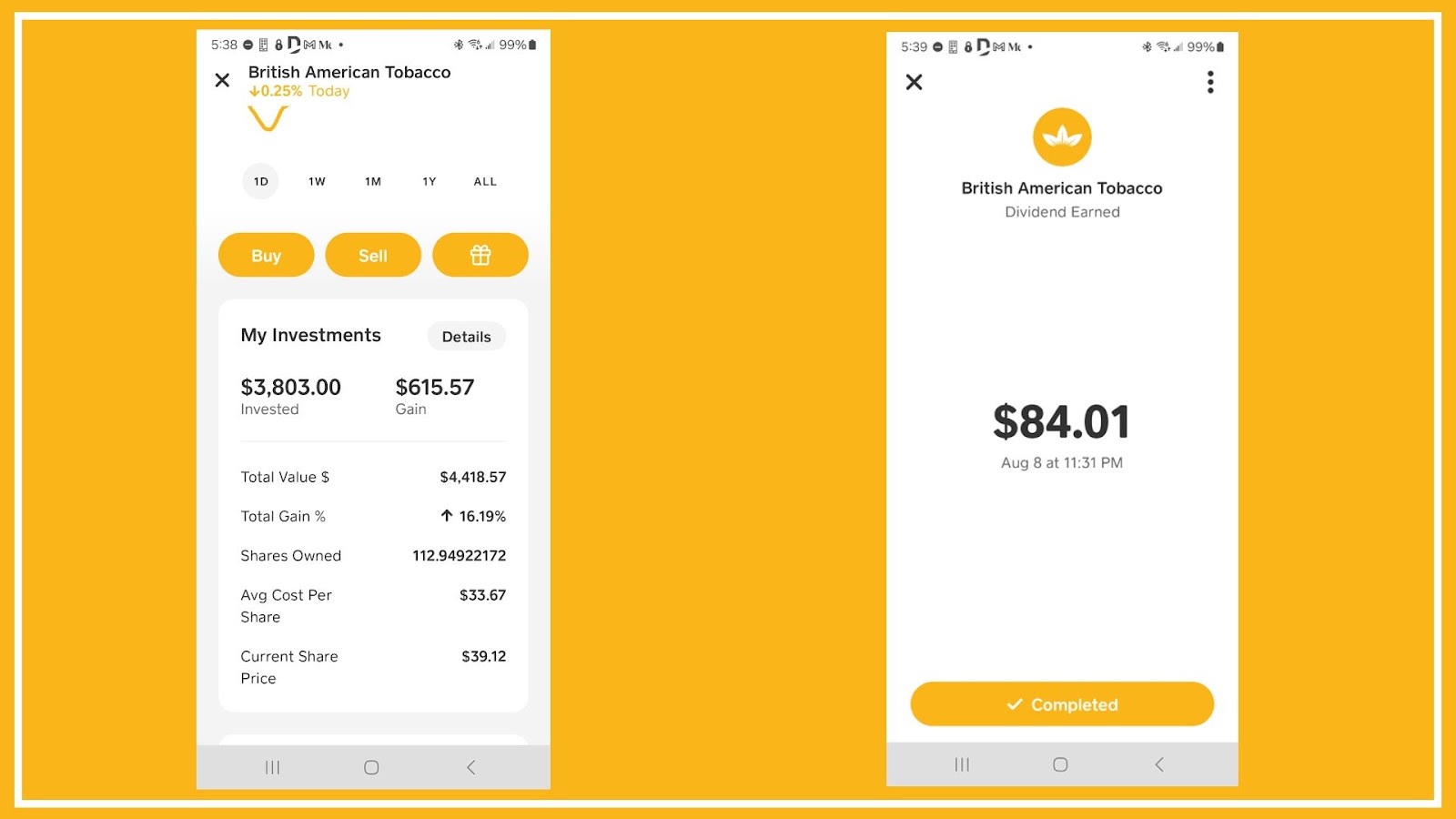

There is nothing like adding a massive lump sum to your dividend portfolio. I remember getting a $3,500 lump sum and purchasing British American Tobacco (BTI) at a discount.

Become CEO of Yourself 2

Now, every three months, I receive a $80 dividend directly on my Dividend Debit Card on the Cash app. I am even more excited to see BTI’s price increase over the last three months.

I recently started going to college using a program similar to the GI Bill. I receive $1,700 per month tax-free to attend school. I literally roll that money directly into my Wells Fargo brokerage account every month. Can you imagine when I do this for four straight years?

Building your own way. I don’t particularly want to go to college because I am retired. However, the idea of investing $1,700 per month into my dividend portfolio is just too powerful.

Additionally, my wife and I have a roommate who pays us $1,000 monthly. That money flows into our dividend portfolios. I also trade options on the side to generate some decent returns.

What is Fixed Income?

The key to all of this fresh capital is to send it directly into our dividend accounts. The true power of dividends is a way to keep generating new income passively.

“The Millionaire Fastlane” clued me into how life works. It doesn’t matter what legal way you make money; it just needs to flow into your money system, which includes your emergency funds, bonds, and dividends.

You can be an entrepreneur, writer, plumber, or basketball star, but the person with the best money system wins. Even in retirement, you should aim to keep adding to your money system.

My wife and I can live comfortably on our military retirement, but we always find ways to add fresh income to our dividend portfolios. We have a roommate and rental properties. I also go to college and trade options.

We are hyper-focused on what is important: generating dividend income to ensure we create a better life for our kids.

The Biggest Book on Passive Income Ever 4!

Conclusion. Don’t you want to travel to Europe with your kids and grandkids? Don’t you want to eat at nice restaurants without worrying about the cost?

If you are to live big, you must dream big. Although my wife and I are retired, we are still working hard to grow our passive income.

Can you imagine in 20 years when we earn $15,000 monthly in dividends? That’s where we are heading. That’s when we can travel the world on dividends alone.

I want to live a life of abundance while remaining a good person. I don’t need to sell my soul or become famous, I just need to invest in dividends.

In the end, we are doing this for our kids. My wife and I already have enough abundance, but we cannot predict the future.

The more resources we have, the more we can help our kids and grandkids. Plus, I want to have an all-expenses-paid trip to Europe courtesy of dividends. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply