Index funds are vital to our wealth-building journey because they provide a safe approach to investing in the stock market.

Index funds are as reliable as you can ask for something that trades on the stock market. However, we must remain vigilant as passive index fund investors.

The goal of index fund investing is to grow wealth alongside the American economy. Although there are bumps along the way, the market generally goes up over time.

The American Dream Costs $5 Million

The importance of index funds. Index funds are exchange-traded funds that follow a specific index. For example, the Dow Jones Industrial Average index tracks 30 high-powered companies in the American economy.

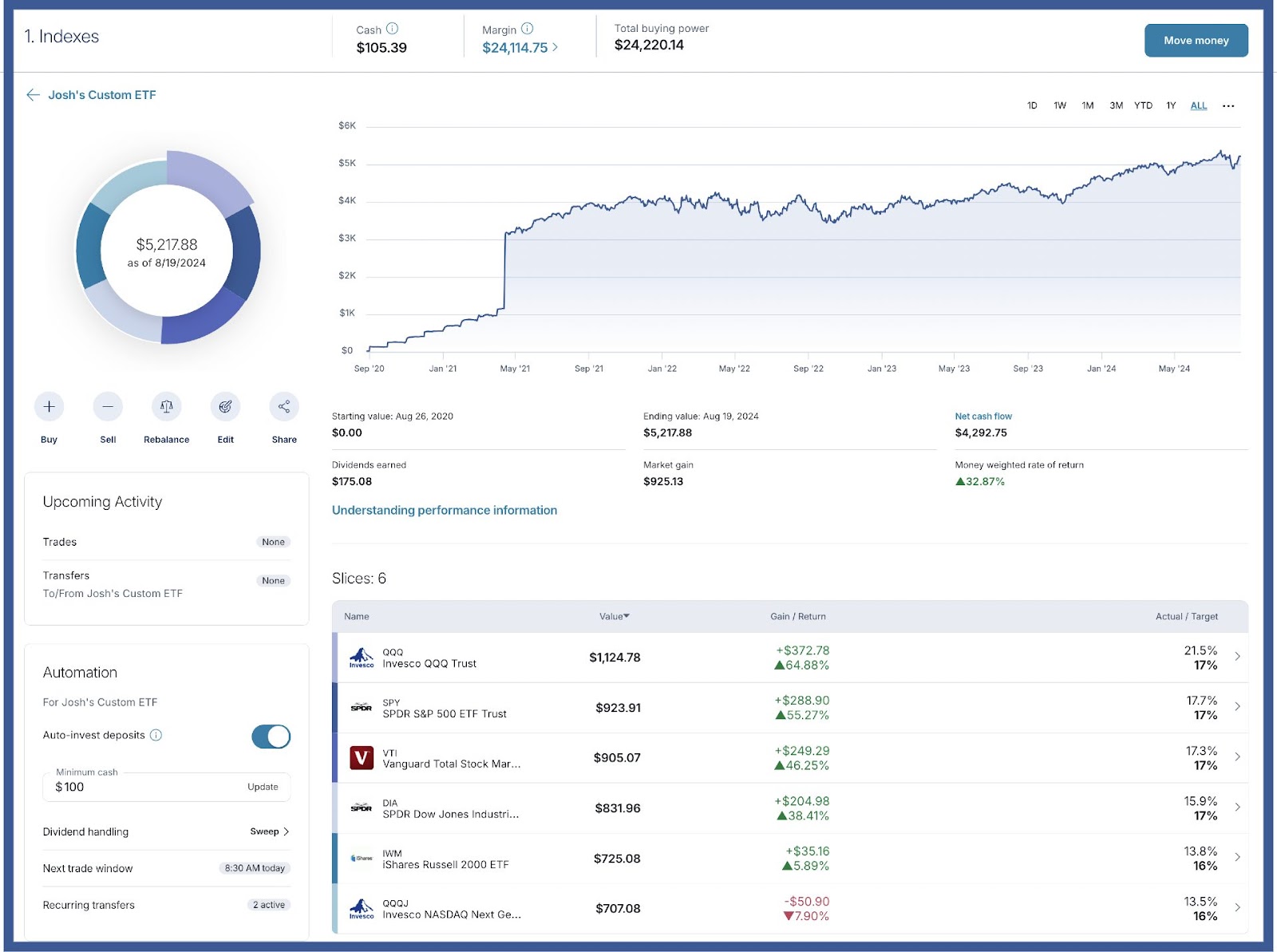

The Dow Jones Industrial ETF (DIA) is an index fund that tracks the Dow Jones Industrial Average. By investing in DIA, we receive all of the long-term growth of the Dow Jones Industrial Average.

Although index fund investing is simple, we still need to follow some principles. These principles will ensure we grow and maintain our wealth for the long haul. The principles are automatic investing, dollar-cost averaging, ignoring markets, and never selling shares.

Series “I” Bonds vs. Roth IRAs

Automatic investing. The best way to invest is to send the money to your brokerage account before it hits your checking account.

Becoming an automatic investor is paramount to saving and investing for the future. Many people call this “paying yourself first.”

Most people attempt to invest at the end of the month once they pay all of the bills. However, as we know, something always comes up in our living situation.

Conversely, the automatic investor allocates index fund investing money as soon as they receive their paycheck.

I like to have my investing money sent directly to my brokerage account via direct deposit. The key is to have rules set in place for your checking account to send to your brokerage account.

Financial Independence through Real Estate 3

I also like to have my checking account at the same bank/brokerage location. In my case, this is Wells Fargo. As soon as I receive my retirement pay, a portion goes to my Wells Fargo brokerage.

It’s better to invest a smaller amount at the beginning of the month than wait for the end of the month, assuming you’ll invest more. Index funds only require your capital, and they will do their best for you.

Dollar-cost averaging. Dollar-cost averaging is similar to automatic investing. It simply means you put the same amount of money into the market, no matter the investing landscape.

The best way to get a strong return from index funds is to consistently invest in the markets, regardless of current advice or guidance.

For example, let’s say I invest $400 per month in an S&P 500 index fund (SPY) and want to keep investing that amount over the long haul.

From Dirt to Dividends 6: Vermiculture vs. Dividend Stocks

If I get a permanent pay raise, I can increase my monthly investment. You do not want to change your investments based on your living conditions.

If inflation hits your budget, you’ll need to make cuts elsewhere to continue index fund investing. I call this living below your means.

Conversely, you can increase your income by getting a roommate or starting a blog. The goal of dollar-cost averaging is to continue investing for the duration, even in retirement.

I am retired but will still invest $600 into the markets on the first of the month. It’s easy to dollar-cost average into index funds because most brokerages allow you to purchase fractional shares.

Overseas vs. Homestead vs. Small Town

Ignore markets. Although I love to follow markets (bonds, stocks, real estate, options, commodities, cryptocurrencies), I never make decisions about my index funds based on what happens in them.

If you cannot stand to see your investments plunge by 30-50%, then you must ignore markets. Index funds are not short-term investments; they work best over 30 to 40 years.

If you do not have the stomach to check the stock market every day, simply set your account to automatic investment and dollar-cost average while ignoring the daily minutiae.

Trust me; it feels good when your index funds are performing well—you want to tell the world. However, it can hurt when they drop by 50%.

The good part is that you purchase more shares when the price is low. Index funds also pay dividends that will buy shares on your behalf.

Debt-Free Society: Beat Credit Card Debt

Following the stock market is not for everyone; however, everyone must purchase index funds. There is no more straightforward way to build wealth; even buying a home is more complicated than passive index fund investing.

Never sell shares. This principle will be controversial. You never want to sell shares of your index funds. This stance goes against every financial advisor in the country. Hear me out.

Selling shares is part of the 60/40 investment advice that says you should allocate 60% of your paper wealth to stocks and 40% to bonds.

When you reach a certain age, presumably around 60, you will start to dismantle your portfolio by selling shares of your index funds. The bonds produce income while keeping your principal intact.

Now, let’s play this out. Let’s say you have $500,000 in index funds across 5,000 shares. That means each share is worth $100.

Top 15 Financial Books of All-Time

You need to generate $20,000 in your first year of retirement and sell 200 shares. At the end of the year, you now have 4,800.

If you continue doing this over 20 years, your share count will decrease significantly. The 60/40 (and 4% rule) rule assumes that the stock market will continue gaining 8-10% and that each share will grow in value.

But what if there is a downturn, and each share now drops to $80? Your initial wealth is now $400,000. You would need to sell 250 shares to generate that same $20,000. This is scary stuff.

It’s better never to sell shares. I complement index fund investing with dividend growth and income investing portfolios. Together, these accounts ensure I have more shares at the end of each year.

My Seven Principles of Wealth

In addition to paper assets, you can generate income by renting rooms, starting a business, or creating content—I call it Happy Cash Flow Retirement. Don’t think that only your paper assets create income during retirement; take a holistic approach to creating income streams and building wealth.

Conclusion. Passive index fund investing aims to grow your wealth by compounding along with the American economy. You do not want to interrupt the power of compounding by selling shares later in life.

As you determine that you’ll never sell shares, you will need to adjust your investment approach to accommodate this lifestyle.

Will the Housing Market Crash?

Many people invest in index funds without knowing how to generate income from these products. However, with a little shift in mindset, you can use your index fund as a fantastic wealth-creation tool.

I use all of these principles to grow my wealth with index funds. Index funds are part of my larger paper asset portfolio, which comprises dividend-paying stocks and income-investing products.

Index funds are simple but can be difficult to sell later in life. You will become quite worried about markets as you try to dismantle your life savings for income. There is a better approach to generating revenue, but index funds are still necessary for growth. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply