Owning a home has become increasingly difficult. Most people view homeownership as the simplest way to build wealth, but those days may be over.

Further, owning multiple properties and becoming landlords allowed people to grow their net worth, increase their passive income, and build generational wealth.

However, purchasing a primary residence is challenging enough; how should people buy an additional property to rent?

The Bait Resignation: Should You Quit Your Job?

The magic of leverage? Purchasing a home is so powerful because buyers can use leverage. In this case, leverage means the buyer can invest 20% of the purchase price, and the bank will give them a loan for 80%.

However, with high home prices, saving the 20% down payment can challenge most average Americans. However, we can use leverage in other parts of the financial market, such as options trading.

Today, I want to evaluate how the average person can use leverage to purchase a rental property or trade options (specifically long strangles).

Each path has pros and cons, but the overall goal is to build wealth slowly; therefore, we will make decisions with that as our primary objective.

Join Up! Time to Sign Up for the Military

Let’s start with our primary residence. Before you purchase a rental property, you’ll want to buy your primary residence. I recommend buying something small, cheap, and safe first.

Your primary residence is your launchpad for all your future real estate ventures. You can take multiple paths once you purchase your primary residence.

Wait until rents equal your mortgage. Once the rental value of your primary residence equals your mortgage, it’ll be easy to move and rent your current home. You may need another down payment.

Use a cash-out refinance. Once you have enough home equity, you can use a cash-out refinance to obtain the down payment for a rental property. Your mortgage may increase, but getting a roommate can offset the cost.

Invest with a family member. You can obtain an equity stake with a family member by helping with the down payment. Investing with your children, siblings, or parents is a good way.

Growing your down payment. Let’s discuss how you can save for a down payment. It’s safe to say that you need to grow your wealth by over 20% per year to outpace inflation and housing costs.

Inflation Ate My Paycheck 106

This statement means that you can’t simply save your money in a high-yield savings account at 5% and believe that you’ll ever catch up to prevailing costs.

Nowadays, you have multiple housing expenses, all growing independently, such as home prices, interest rates, insurance premiums, property taxes, maintenance costs, energy bills, and housing association fees.

Using a government program is an excellent way to lower your down payment on your first home. If you are young, I would join the military and use the VA Loan (I did).

Other programs include FHA, FannieMae Home Ready, FreddieMac Home Possible, and USDA direct loans. I wrote about these programs in my article “Maximum Leverage 2: Buy Homes with No Down Payment.”

Your 401K vs. A Recession

Taking matters into your own hands. Outside of getting a government sponsorship, the most accessible way to grow your down payment is with options trading.

I think it’s safe to say that you can double your money every year with options trading if you learn the ropes, take it seriously, and don’t get greedy.

The key to successfully trading options is finding the best formula for your temperament and goals. I use two plays: the options wheel (selling covered calls and cash-secured puts) and long strangles.

I cannot use leverage with the options wheel strategy because you need to own the stocks or have money to purchase the stocks. However, I can use leverage when trading long strangles.

Using leverage to maximize wins (and losses). Leverage is a two-sided sword: it’ll increase your earnings as you win and accelerate your losses when things go wrong.

Start a Blog for Passive Income

Trading a long strangle involves buying one put and one call to “strangle” the stock price. For example, if Palantir (PLTR) trades for $30, I would buy one call at the strike price of $31 and one put at $29.

I can win regardless of the direction of the stock price as long as the movement is volatile enough. To be profitable, you need at least a movement of 10% in either direction; that’s why I trade strangles around earnings calls.

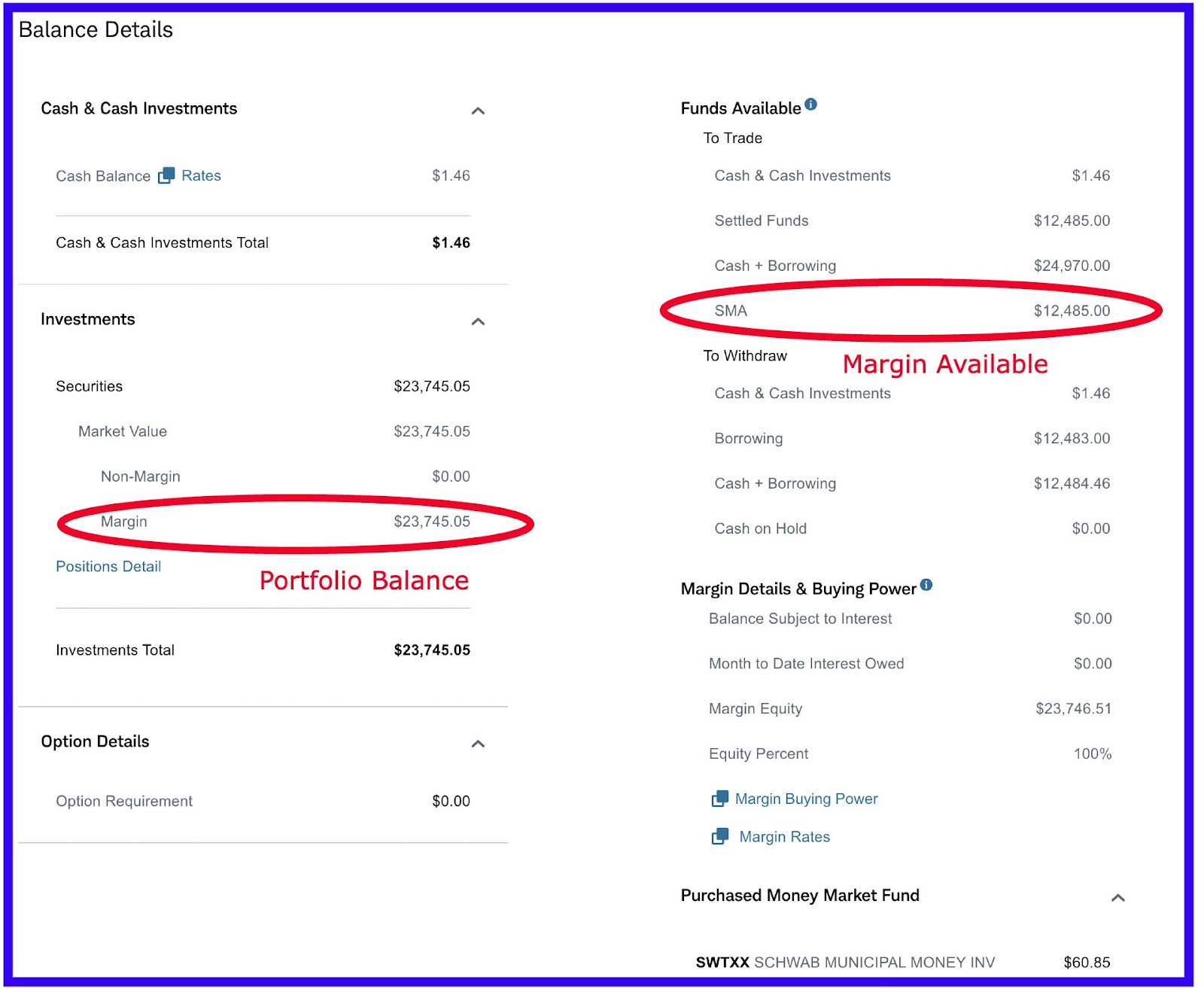

Now, let’s see how we can use leverage to magnify our gains. We can use a margin loan against the holdings in our portfolio.

Let’s say we have $50,000 invested in our options portfolio; our brokerage will probably give us $20,000 to $25,000 in margin.

How Much Do You Need in an Emergency Fund?

This is how I would structure a $50,000 options portfolio. First, I decide how much I want to risk at one particular time. In this case, I would say $10,000.

I would invest $10,000 in a money market fund, which currently earns 5.1%. The other $40,000 would be invested in the closed-end Pimco Dynamic Fund (PDI), which has a 14% dividend yield.

My PDI position would pay me $466 in monthly dividends. Alternatively, I could invest my $40,000 in an S&P 500 index fund (SPY) that grows at 10% annually. I personally just love dividends.

I would trade long strangles against Palantir (PLTR) every three months using margin. Trading $10,000 at a time, I could safely earn $2,000 per trade.

Being Broke Isn’t Cute, part IV

Therefore, my $50,000 portfolio would annually generate $510 in interest income from my money market fund, $5,592 in dividends, and $8,000 from options trades (minus margin costs).

I would have $64,102 at the end of the year. I could take the $14,000 off the table or use it to grow my portfolio faster. Of course, you could increase your options trading allocation, adding more risk but more reward.

Putting it all together. Trading options is the purest form of money. You are using your capital to make more capital. Very few people on Earth have done this successfully for a long time.

It’s not particularly difficult, but it can be an emotional roller coaster. That’s why we limit our trading allocation to a small portion of our overall portfolio.

Debt-Free Society: Beat Student Loan Debt

Likewise, owning a primary residence can be very demanding; maintenance costs are constant, and expenses seem to rise every month.

Becoming a landlord is more challenging than owning a primary residence because you now have two or more properties to consider and maintain.

I own three homes and a tiny house. Buying each house was a pain in the arse. Let me know if you want me to discuss the torture of buying (and refinancing) each home; interestingly, each has its own horror story.

Being Broke Isn’t Cute part III

Conclusion. When you trade options or become a landlord, you must do it for a higher purpose. “Making money” is not a good enough reason to lose sleep or jeopardize capital.

I do both for the benefit of my children. Eventually, my rental properties will not have a mortgage, and they will be almost 100% pure income.

Trading options allows me to make money at any time, right from the comfort of my home.

If I want to make more than the amount above, I can find two more stocks to follow. This way, I can trade a long strangle once a month. That would increase my annual options earnings from $8,000 to $24,000.

You see, I control my financial destiny. I can squeeze more juice from the same lemon (the same $10,000). I just need to dedicate more time to learning and following more stocks.

Debt-Free Society: Beat Automobile Debt

Owning multiple properties is not a lucrative endeavor in the short term. It may take 20 years to earn extraordinary profits. However, with a long-term vision, owning multiple homes can grow your wealth significantly.

If you are serious about building wealth, I would start with trading options. Learning to make money from scratch is vital to understanding the velocity of money.

Once you have a good handle on trading options, becoming a landlord is the next step. As a landlord, you need a dynamic income stream to handle multiple financial scenarios simultaneously.

I’ve been a landlord for over ten years, and you can fix most of your problems with money—that’s why options trading is so valuable. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply