When do you plan on retiring? Are you already retired? These questions will be vital in determining what financial instruments you’ll need to leverage.

Investing is all about your time horizon, goals, philosophy, and risk tolerance. The good part is you don’t need to have all of the answers the first day you start investing.

The power of income. Many investors chase capital gains because it makes them feel smart and gives them a rush.

Becoming an Entrepreneur #5: Building an Audience

They say things like, “My house went up in value by 200%” or “I bought a Tesla in 2013, and it has appreciated over 1,000%.”

However, life is all about cash flow. We need income to pay the bills and enjoy the finer things in life. I became an income investor to ensure I always had enough cash flow to be my best self.

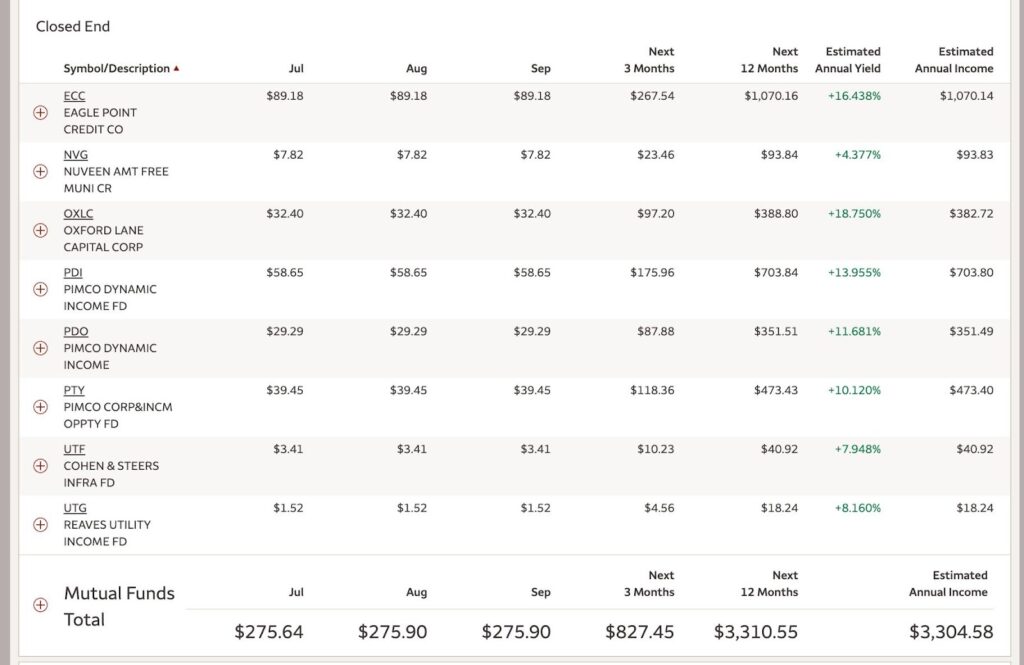

There are six categories of income investing: dividend ETFs, closed-end funds, mortgage REITs, preferred shares, business development companies, and high-yield blue-chip stocks.

Closed-End Funds vs. Dividend ETFs. I want to compare closed-end funds and dividend ETFs today because they play important roles at different stages in life.

Treasury Notes vs. Certificates of Deposit

Most investors in closed-end funds don’t overlap with those that invest in dividend ETFs. However, I invest in both, and I will share why.

Closed-end funds are all about grabbing your income today. When you purchase shares in a closed-end fund, you want to start seeing dividends within 30 days.

My favorite closed-end funds are PIMCO (PDI, PDO, PTY) bond funds that pay monthly. They all yield over 10% and add significant income to my daily life.

Why I invest in Dividend ETFs. Dividend ETFs, like Schwab US Dividend Fund (SCHD), are all about capturing the magic of dividend growth investing (DGI).

Bond Investing in Your 70s

Instead of buying powerful individual DGI stocks like McDonald’s (MCD) and Starbucks (SBUX), you can just dollar-cost average into SCHD for the rest of your life.

Seriously, you can purchase SCHD for the next 40 years and only check on it yearly. The fund does all the rebalancing work by itself—all with a meager service fee (0.06%).

Dividend ETFs are all about income tomorrow. Therefore, if you have a 20-30 year time horizon, you may be better off investing in a Dividend ETF.

I invest in both securities. I invest in both securities because I love income investing. I want my income today, so I invest heavily into closed-end funds as my main source of revenue.

Are We Living in Fast Forward?

However, I am only 42 years old. I would be a fool not to leverage the compound effect of years of dividend growth investing.

What is your time horizon? When do you plan to retire? Do you want to leave a portfolio of stocks and bonds to your kids and grandkids?

What is your tax situation? There are closed-end funds that are state and federal tax-exempt. Some dividend ETFs like SCHD pay qualified dividends that reduce your tax burden.

Start a Review & Content Business

There isn’t a one size fits all approach to investing, but the more you understand about various products, the better your chances.

Let’s look at income. As an income investor, I love looking at my dividend paychecks. If I invest $10,000 into PIMCO Dynamic Fund (PDI), at a yield of 14%, I would receive $116/month.

If I invest $10,000 into SCHD, at a yield of 3.58%, I would receive $29/month. But, I would be missing the point of investing in SCHD.

Five Takeaways from “Walk Yourself Wealthy”

Over the years, SCHD will continue to appreciate in value plus pay a rising dividend. Before you know it, my yield of cost will be closer to 20 or 30%.

To receive the same kind of dividend growth, I would need to reinvest 20-30% of my dividends in PDI back into PDI.

Understanding the language of investing. Dividend ETFs do all of the work for you. There is almost no bad time to purchase these funds.

Most closed-end funds use leverage and deal with products such as bonds, leveraged loans, CLOs, mortgages, and senior notes.

The Information: Passive Income is the Only Way

These leveraged products move in cycles, and interest rates heavily influence their prices and trajectories.

To get the best results from closed-end funds, you will need to understand business cycles, interest rates, and how they affect the underlying products of your CEF.

I find all of this stuff interesting, and I love following the technical and fundamental analysis of the stock market. If this is not your world, I recommend sticking with SCHD and other Dividend ETFs.

When do you need your income? If you are nearing retirement, closed-end funds can provide you with a paycheck replacement strategy.

Hustle Culture: How to Replace the 401K Mindset

I love receiving my monthly payments from my CEFs. It feels better than receiving a paycheck from work. One day, my dividend payments will be larger than my pension paychecks.

Dividend ETFs can serve you well today but are much better for tomorrow. A dividend ETF would serve you wonderfully if you want to create generational wealth.

Having a lot of income is great, but it does have a learning curve. Dividend ETFs can continue to grow with the economy through thick and thin, with less of a curve.

Few people will understand how to leverage a closed-end fund to receive the maximum benefits properly.

Beware of Fake Passive Income Claims

Again, to keep growing your income with CEFs, you must reinvest a portion of your dividends. Due to the nature of DGI, your heirs can simply extract all dividends from SCHD, and it will continue to grow in price and payments.

Conclusion. So there is a lot to take in: taxes, time horizons, income levels, and generational wealth.

Luckily, you can invest in both CEFs and Dividend ETFs like me. I have the best of both worlds and couldn’t be happier.

Treasury Bonds vs. Municipal Bonds

It’s important to remember that I do the work to stay abreast with all my securities. I know how to find the top 10 securities in SCHD and the current treasury bond rates.

The more seriously you take your portfolio and investing career, the better your “luck.” There is no easy answer, just knowledge.

If you received $100,000, how would you invest it? What would be your short and long-term investing goals? How much income do you need today and tomorrow? Think like this, and you will do just fine. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply