Paying bills sucks, but it is a necessary part of our lives. How can we create less friction when dealing with our expenses?

The best solution, I found, is to pay bills with passive income. Why is passive income important to your overall financial health?

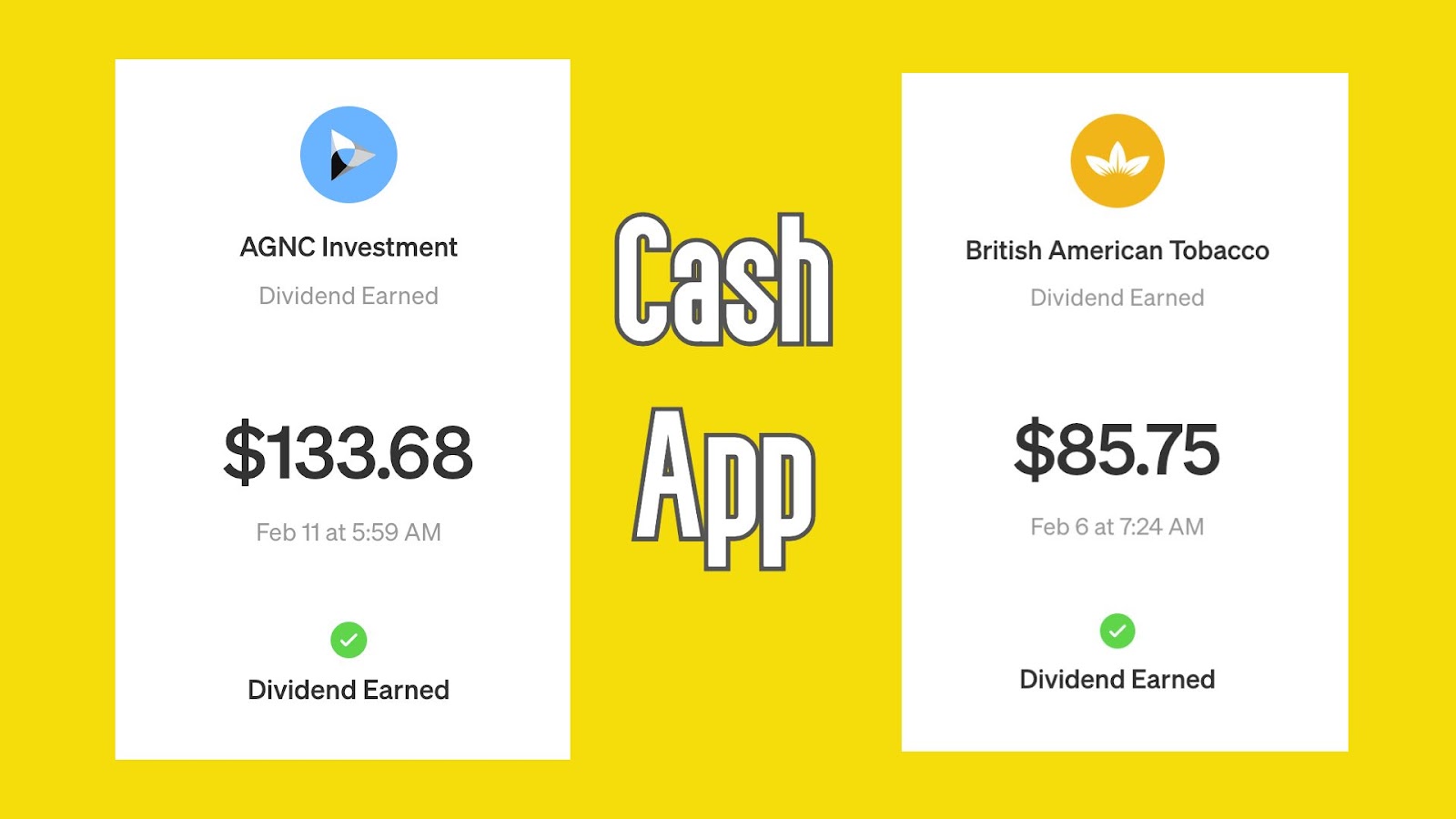

Passive income is money you receive without exchanging time for money. Imagine receiving $133.68 from one of your stock positions—what bills could you pay with that?

What is Your Creative Ability?

To understand the premise of paying bills with passive income you must first understand the lie they told you from the start. Once you rebuke this lie, you stand a much better chance of building passive income streams that can set you free.

The greatest lie ever told. They told you to work for money. They sent you to exchange time for money and, in turn, exchange money for expenses.

This is the first lesson Rich Dad taught the kids in Robert Kityosaki’s “Rich Dad Poor Dad.” He told them to work without receiving a paycheck. After some time, the kids learned the most important life lesson: don’t work for money, work for assets.

The average person works to pay bills. When they stop working at age 65, they use Social Security to pay for expenses. However, they receive greatly reduced income from social security.

For many, their only “asset” is their social security payment and perhaps a house. All that hard work throughout their lives for this final existence.

Life as an Income Investor

These hard-working people, including my parents, fell into this trap. They had help from corporations and governments that promised nice pension payments along the way.

My parents never focused on owning assets; therefore, they retired without assets. I was heading down the same path until I became a student of Robert Kiyosaki.

Let’s destroy the lie today, right now—forever. Do not work for money; work for assets. If you can convert your brain to focus on assets, you’ll be on the path to an easy street. Let’s begin.

It’s time to purchase assets. Every single American with a cell phone can download Cash App. Answer a few questions and you can become a stock market investor.

When you receive your paycheck, purchase dividend-paying stocks with at least 10% of your after-tax income.

Get Past the Middle Class

“But Josh, I can’t save that much?” Sure you can. Remember, you are not working to pay expenses, you are working to purchase assets. That’s your primary objective.

Does it take some time to convert your mindset? Sure. But it is possible. My wife and I owned zero dividend-paying stocks in June 2019. We have over $380,000 in stocks, bonds, and high-yield savings accounts less than six years later.

More importantly, we receive $2,400/month in dividend income. With this money, we can pay all of our bills minus our mortgage.

I spent the last couple of weeks writing in detail about how to pay each of your bills with income-investing products such as closed-end funds and preferred shares.

- Paying Your Electricity Bill with Closed-End Funds (pdf)

- Paying Your Water Bill with Preferred Shares (pdf)

- Paying Your Auto Insurance with BDCs (pdf)

- Paying Your Cell Phone with Dividend Stocks (pdf)

- Paying Your Car Note with Mortgage REITs (pdf)

- Paying Your Cable Bill with Dividend ETFs (pdf)

Each article explains how to generate enough income from dividend stocks and income-investing products to set yourself free.

Down-sized? Time to Start an Online Business

Passive income: myth versus reality. But does passive income work in reality? Can you depend on the dividend to hit your accounts religiously?

I’ll level with you—who would you trust more: Fortune 500 companies like Verizon (VZ) and AT&T (T) or the government with social security?

Verizon (VZ) and AT&T (T) have quarterly earnings calls and set their dividend size and dates far enough to see what is happening. I personally trust these corporations more than the government—and I worked for the government for 24 years.

The government gives you one measly social security cost of living allowance per year. Your real expenses increase by 10-20%, and the government raises your check by 2.5% (for example).

We can do better with corporations and closed-end funds. I know it is tough for some people to trust corporations, but you must think like a businessperson.

If you trust social security more than British American Tobacco (BTI), nothing I can say can change that. However, investing in corporations and income products puts me in charge of my financial destiny.

The American Dream is Passive Income

The magic of learning about money. Let’s say I receive my $85.75 dividend from BTI. Based on what’s happening, I can reinvest it in BTI, save it in a high-yield savings account, invest it into a 12%-yielding closed-end fund, or take my wife to dinner.

I can make whatever decision best suits the moment. If you keep investing, eventually, you’ll have excess cash compared to expenses.

You’ll have more money coming in than you can imagine. You can pay your mortgage, bills, and food budget with dividends.

Once you reach this point, you will become financially independent, or, work-optional. Even better, these corporations will give you annual pay raises to help you deal with inflation.

Individual Preferred Shares vs. Preferred Shares

So, what’s the downside to investing for dividends and paying your bills with income products? The toughest part is getting the money into your brokerage account.

One budget to rule them all. My wife and I completely changed our lives and started saving and investing. Our first mission was to pay down debt.

Debt is the power of compounding working against you. To save and invest, you need financial discipline, which is extremely challenging for most people.

America convinced you that you need a huge home, two nice cars, and many spa trips. The American dream morphed from a small home with a dog to lavish trips and fancy cars.

To start saving and investing, you’ll need to reset your version of the American dream. I am living my version of the American dream today.

Homeschooling + Online Business

My wife and I don’t have to work. I will homeschool my kid starting next year. We own properties and live in a nice home. The best part is we earn over $150,000/year without working.

The key to our financial success isn’t something crazy or extraordinary; it’s simply living our lives through basic needs.

We drive our cars for years and take care of them. We go on local trips and have an $800/month food budget. My wife and I each have a $750/month personal allowance.

Each month, I route at least $2,000 of fresh capital into our brokerage accounts, on top of reinvesting. Therefore, we earn more dividend income each year than the last (by a country mile).

Wiping the Debt of Christmas Past

Conclusion. Ask yourself one question, “If your paycheck stopped, how much money would you still have coming in?” That is your passive income.

I track my monthly passive income from dividends ($2,400), royalties ($300), rents ($1,800), and college ($1,800). This is on top of my military pension ($9,100).

My goal is to have my dividend income exceed my military pension for ten years. This is important because my pension dies with me, but I can pass my dividend income to my kids and grandkids.

Imagine your entire family not having to work. Instead of focusing on “nastygrams” from your boss, you can volunteer at church, conduct vital research, or teach your grandkids to farm.

The world is your oyster. There has never been a better time to free yourself from the workforce. Sure, you may need to move in with your parents or siblings or get roommates, but what are you willing to do to be free? I know what we did, and we are now living the dream. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply