Do you still have a cable bill? I have a Direct TV bill plus three or four streaming services. All of these bills can be expensive and annoying.

Part of me wants to cancel these services, but I don’t because I have the resources to pay for them. Instead, I concentrated on building my passive income to fund these luxuries.

If you love having all of the streaming services, you’ve come to the right place. I will describe how to earn enough passive income from dividends to accumulate as many services as you’d like. Let’s begin.

Do you need streaming and cable services? I pretty much only watch YouTube all day; however, even that costs $25 per month.

I keep paying for Direct TV because I do not want to rely solely on the internet for entertainment. We have six humans in our household, all sucking down maximum internet. Having Direct TV ensures that I can watch something during the busiest times.

Let’s review my streaming and cable services: Direct TV ($90), Hulu w/ Max & Disney + ($35), Netflix ($28), Hallmark + ($8), and YouTube ($25). These services combine to cost a whopping $186 per month.

The good part is that I can cancel these at any point and not lose an ounce of sleep. I still have hundreds of physical DVDs and Blu-rays, plus another 800 digital movies on Vudu. I’m good on entertainment.

I keep these services for my kid’s benefit. Plus, watching YouTube without commercials is fantastic. However, I now need to pay this $186 per month with dividends.

The magic of dividend ETFs. I am a hardcore income investor seeking 9-10% annual dividend yields from anything I purchase. Dividend ETFs do not provide yields this high; however, I consider them to be income-investing products. Why?

Although Dividend ETFs only yield 3-4%, they have extremely high annual dividend increases and price growth. This means a 4% yield today may be 10% in a few years.

Dividend ETFs embody dividend growth investing (DGI), which differs from income investing. The concept behind DGI is to purchase income today that increases tomorrow.

Income investors want their cash flow today, while DGI investors want smaller income today in exchange for price and dividend growth tomorrow.

Income investors rely mainly on fixed-income sources, while DGI investors focus on companies with products that increase profits over time.

Dividend ETFs combine tons of DGI companies under one umbrella. My two favorite Dividend ETFs are Schwab US Dividend (SCHD) and WisdomTree US Dividend (DHS). They both yield around 3.5%.

I’ll need to invest a lot of money to cover $186 monthly, but we can get it done. Once we have this amount of coverage, the Dividend ETFs will continue to raise their dividends annually, making our lives significantly easier.

How much do I need to invest? Let’s start with some math. We can determine how much we can invest by first finding out the annual costs of our streaming services. The annual cost is $2,232 ($186 x 12).

Now we can divide $2,232 by the dividend yield of 0.035 to come up with $63,771. That is a heck of a lot of money.

How the heck can we save $64,000? Well, Rome wasn’t built in a day. We must cut our expenses to the bare minimum to achieve this level of saving and investing.

I remember a time when I thought it was impossible to save even $1,000. This wasn’t too long ago, by the way. I invested my first $1,000 in the markets in June 2019.

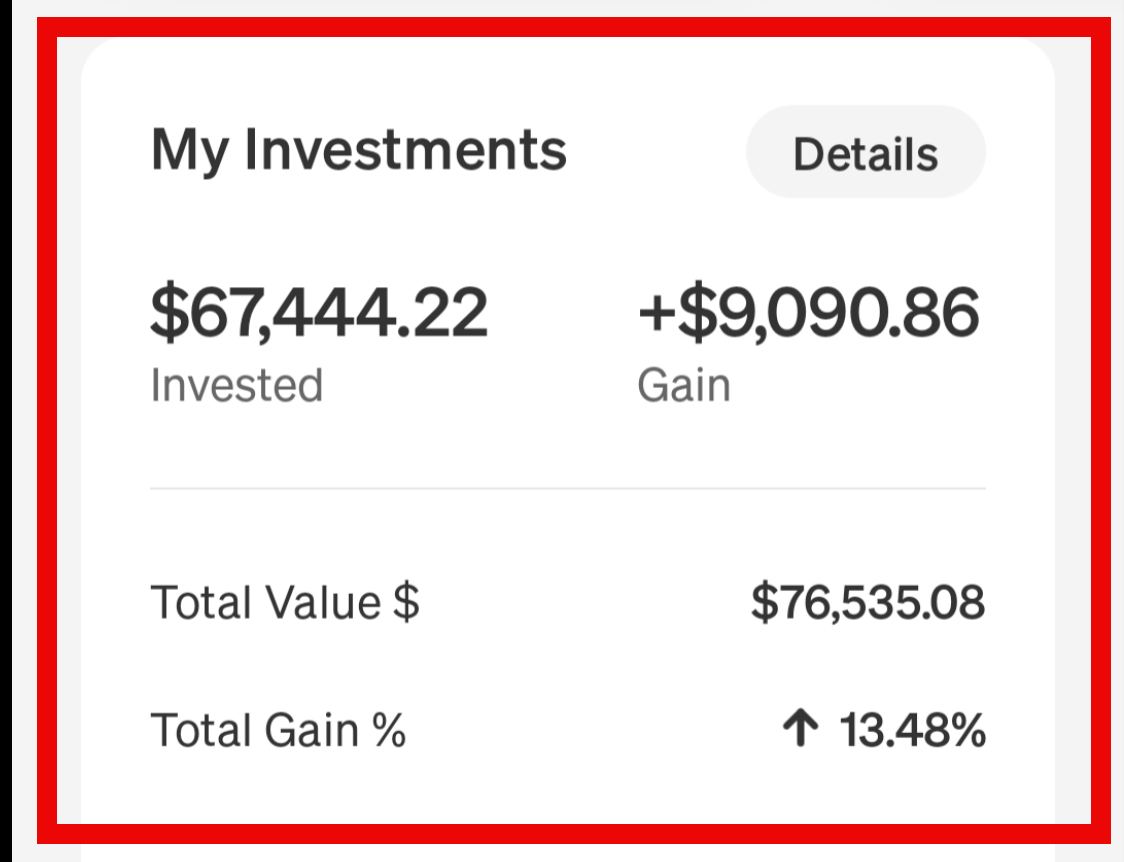

I opened my Cash App brokerage in July 2020 (you can read about it here). It now has $76,535 and pays me roughly $450/month.

My goal for 2025 is to receive a $100 quarterly dividend from SCHD. I put my first $8 in SCHD on the Cash App yesterday.

I have SCHD on other brokerage accounts, but now I am making a concerted effort to build a massive dividend from it.

I am focusing on SCHD because it tends to raise its dividend by over 10% every year. Instead of reinvesting, the companies will raise their dividends to beat inflation.

These dividend increases are why I consider Dividend ETFs to be income-investing products. Let’s see how the annual $2,322 dividend grows over time at 10%.

In the 30 years, the annual dividend would grow to $39,000, or $3,250 monthly. We should be in great shape as long as our streaming services don’t grow that fast.

Saving and investing. To save the $64,000, you may need to cancel your streaming services, which is the ironic part of the story.

My wife and I put our heads down for five years (2019-2024) and came out ahead. I went to Japan for two years without my family so that my wife could keep her job in Florida.

While I was in Japan, my wife kept two roommates, which covered the entire mortgage. I didn’t watch TV for those two years but focused on starting my writing business.

I now have over 1,600 articles on my blog. We have rental properties and a roommate. I go to college full-time using the GI Bill.

In short, the money isn’t going to save itself. To do more, you must become more. Coincidentally, the best feeling is not having to go to work on Monday.

Consider this a call to arms. If you need a job to pay your cable bill, then you’ll have to keep working.

Dividends and passive income represent a break from the norm. Now is the time to change everything and take control of your destiny.

Life is a simple game. When you receive money, you must find a way to grow it. Those who can put capital to work and earn a return will win.

Conclusion. $64,000 sounds like a lot of money, but saving this amount is possible. How much do you receive from taxes or a bonus? How much can you save by moving in with your family?

These are tough questions, but those who answer them honestly have a chance at financial freedom. I don’t like paying $186 per month for TV services.

However, it’s a luxury I can afford because I receive over $2,400/month in dividends, $700/month in rents, $300/month in royalties, and $1,800/month for college.

Dividend ETFs can change the course of your life. If you can get $64,000 into SCHD, companies like Chevron (CVX), Pepsi (PEP), Verizon (VZ), and Coca-Cola (KO) will do the heavy lifting for you.

Not only may your dividend income grow to $39,000, but your principal may grow to $1.1 million. These are impressive numbers that we all should strive to achieve.

Of all my favorite income investing products, SCHD requires me to invest the most capital to be productive. However, it also grows the fastest.

If you want every streaming service and cable network, it’s time to turn the tide on your income. Let’s replace earned income (from a job) with passive income from great companies. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply