Getting your finances “together” means putting idle money to work. Saving and investing can be tough concepts for the average person because they involve risk.

Today, I want to assist retail savers and investors in deciding which products are best for their unique situations. The first step to making informed decisions is accumulating lots of information, which is my goal.

CDs vs. Bonds. I wrote “CDs versus Bonds” over a year ago, and some things have changed. The Federal Reserve has dropped interest rates by about 1%. This drop forces retail investors to understand the difference in financial products.

Covered Calls vs. Cash-Secured Puts

Certificates of deposit (CDs) originate from banks and other financial institutions. They encourage savers to lock their money inside the institution for a set amount of time.

For their efforts, CD investors receive decent yields that could be slightly higher than the Federal Funds Rate. The Federal Deposit Insurance Company also insures CD accounts up to $250,000.

Bonds originate from corporations, municipalities, and governments that hope to attract investors with tempting yields. You can find bonds for your unique situation but must know where to look.

You can do better. As a retail investor, you can do better than CDs. Certificates of deposit were important when you wanted to obtain rates higher than the standard 0.01% on your checking and savings account.

Building Generational Wealth Via Dividends

However, the advent of high-yield savings accounts diminished the importance of CDs. Instead of locking my money in for a year, I can get the same yield on a high-yield savings account.

Let’s review Discover Bank’s CDs, which also offer my favorite high-yield savings account. Twelve-month CDs yield 4.00%, and 30-month CDs offer 3.40%. I don’t find these numbers impressive.

The world of bonds is much wider and taller than CDs. In fact, the bond market ($55 trillion) is many times bigger than the stock market ($40 trillion). However, bonds hide in plain sight because there is nothing sexy about bonds.

Discovering all the various types of bonds will serve retail investors over time. Not only can you lock in rates for far longer, but you can also find unique traits in each type of bond. Let’s review some of those unique traits.

The Perks of Becoming a Capitalist

Series “I” Bonds. These savings bonds should be your first step on the journey. They last 30 years, adjust with inflation, and grow interest-free (until you cash them in). You can purchase them on the TreasuryDirect.gov website.

Series “EE” Bonds. The US government guarantees that your Series “EE” bonds will double in 20 years. You get a small interest rate for 30 years. These are great to purchase for kids who will need to use them in 20 years. You can purchase them on the TreasuryDirect.gov website.

Treasury Bills. These bonds offer maturities between 1 month to 52 weeks. If you have lots of money and want to keep rolling it, this is where to do it. You don’t pay state tax on these products and the rest of the treasuries from TreasuryDirect.gov.

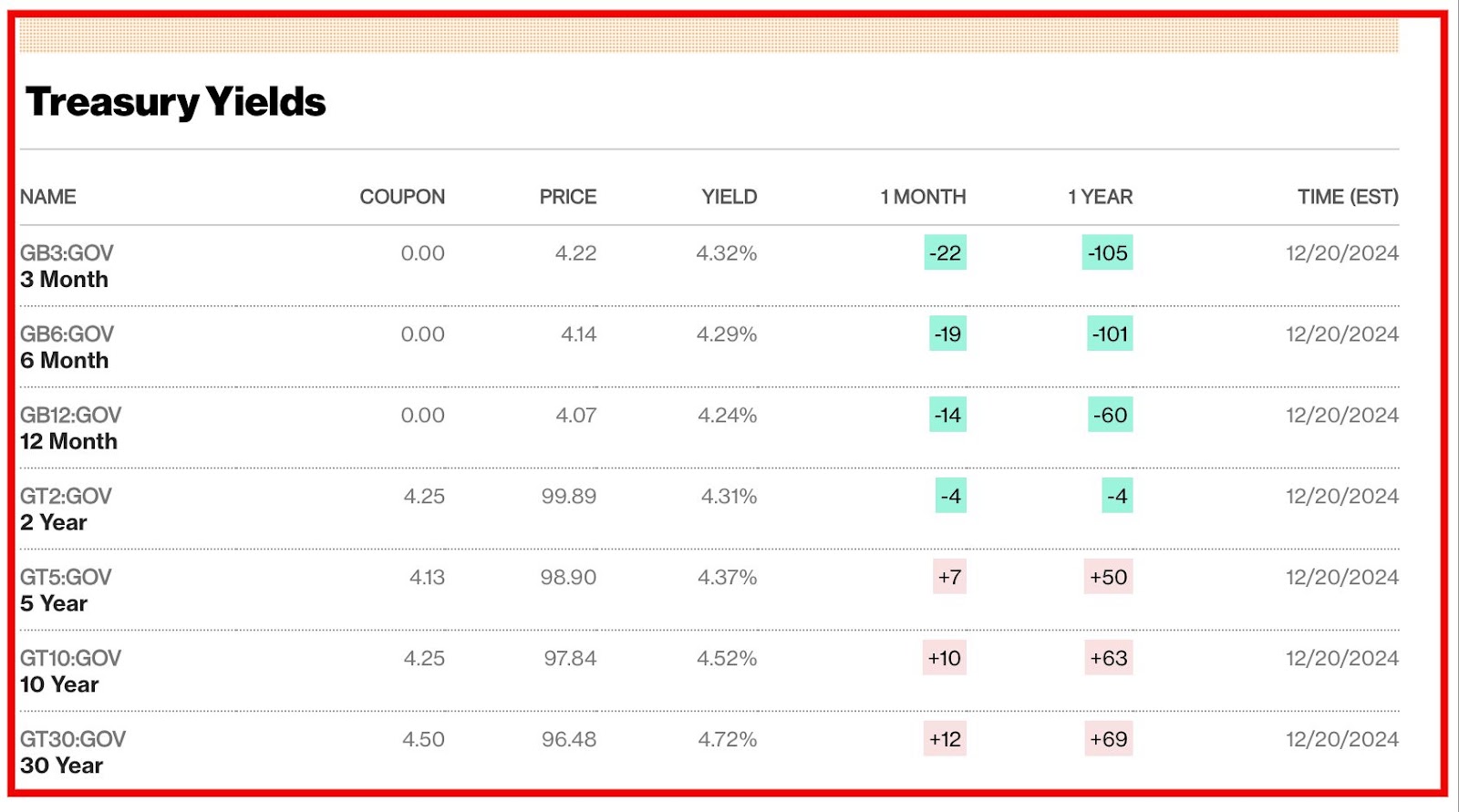

Treasury Notes. These bonds offer maturities between 2-10 years. Current rates are: 2-year (4.31%), 5-year (4.37%), and 10-year (4.52%). These rates are much higher than the CDs we saw earlier, plus the price can appreciate (or decline). You can purchase them on the TreasuryDirect.gov website.

Treasury Bonds. My favorite treasuries are Treasury Bonds that mature in 20-30 years. Current rates are: 20-year (4.8%) and 30-year (4.72%). The 20-year rate is absolutely amazing. You can purchase them on the TreasuryDirect.gov website.

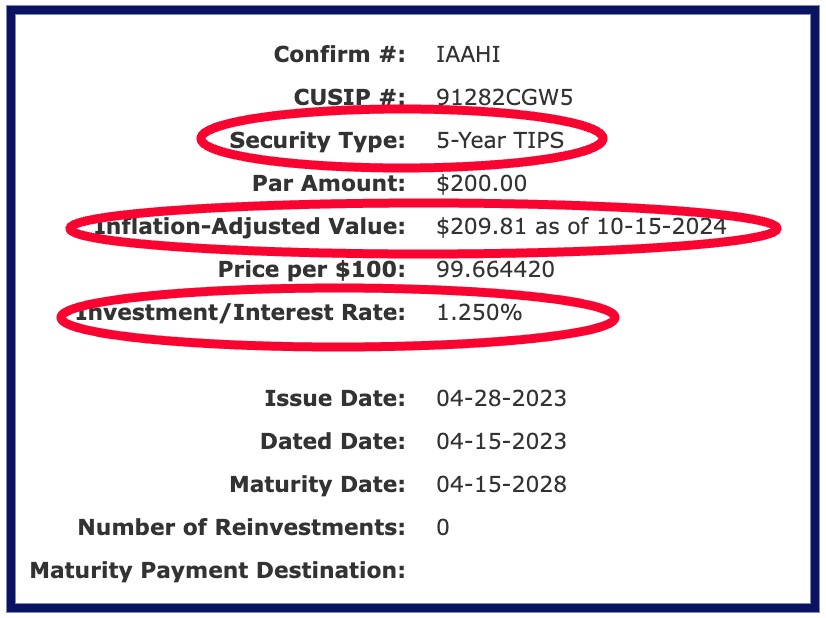

Treasury Inflation-Protected Securities (T.I.P.S.). TIPS can be tough to understand, but they adjust your principal to affect your interest payments. If things go as planned, your interest payments will adjust along with inflation over the years. You can purchase them on the TreasuryDirect.gov website.

Municipal Bonds. Municipal bonds are a great way to support your local municipality. The best feature they offer is most do not pay federal tax on interest payments. If you live in a states without state taxes, you may put yourself in a totally tax-free environment. You can purchase these bonds at CharlesSchwab.com and in municipal bond funds on the stock market (recommended).

Mortgage-backed Securities (MBS). MBS are bonds that package many mortgages into one security. Because of their slightly higher risk, MBS offers slightly higher yields than treasuries. These bonds are mainly for institutional investors, but retail investors can access them on the stock market through corporation stocks like Annaly Capital (NLY) and AGNC Corporation (AGNC).

Corporate Bonds. Corporate bonds can offer 20 and 30 years of products that yield over 6%. You can purchase directly from brokerages like ChalresSchwab.com, but typical minimums are at least $10,000. Corporate bonds offer advanced retail investors an opportunity to invest like institutions.

Welcome to the world of bonds. Does the world of bonds seem overwhelming? It may be from the start, but it’s worth exploring and exploiting.

Certificates of deposit cannot offer the magnitude of choices you can find in bonds. Treasuries offer no state taxes, while municipal bonds offer no federal tax. Series “I” bonds and T.I.P.S. adjust with inflation.

Dividends vs. Royalties IV

CDs are a good first step into the world of collecting interest. However, as rates drop, you must find better investments for your money. At one point in 2020, CD rates were around 1.5%.

I recommend the following order of operations: certificates of deposit, treasuries, corporate bonds, and bond funds on the stock market.

One final difference between CDs and bonds is that bonds can appreciate or depreciate in value. You’ll be in a good position if you hold a 5% bond in a 2% interact-rate-environment.

Most Certificates of Deposit do not resell on the open bond market; therefore, you won’t be able to leverage that aspect of bond growth investing. However, the best technique for bond investing is to buy and hold until maturity.

How to Control Your Spending 104

High-yield bond reinvestment. High-yield bond reinvestment is something you should do for all interest payments from CDs and bonds.

With this technique, you reinvest your interest payments into higher-yielding products. You can buy Series “I” bonds with a minimum purchase of $25. Alternatively, you can purchase partial shares of bond funds, preferred share funds, and closed-end funds on the stock market.

Always try to reinvent your bond interest payments. Eventually, you can spend the dividend income from your stock market bond funds.

Rich people have figured out that the best way to produce money is with money. We should follow their lead and reinvest our interest payments into more long-term assets.

Conclusion. I am not a big fan of certificates of deposit. However, if you are retired and fear the markets, they offer safety and security.

Retirement Planning for the Average Person 6

However, retail investors must venture outside their realm of knowledge to obtain excellent yields. The world of bonds is massive and exciting.

If you purchase a 30-month CD at 3.4%, the prevailing interest rates will almost certainly be lower by then. What should you do next?

You don’t want to depend on a 2% certificate of deposit in retirement. I have locked in 4.5-yielding treasury bonds for 30 years and will continue to do so.

It’s an exciting time for retail investors as more options open up to us. Professionals have used bonds to maintain wealth for centuries, and we should do the same. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 13 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply