Most Americans realize the importance of saving money—whether they choose to save is a different story. Saving is a mechanism we put into place to protect ourselves from emergencies while also preventing us from using our investment accounts.

I always tried to save early in my adult life—to no avail. However, in 2019, I started to take my finances much more seriously, which led me to open my first high-yield savings account.

Over the years, I have become fascinated with the distinction between savings and investing. While it is more fun to invest money, it is every bit as important to save money.

Why You Need Passive Income!

I have started accumulating many high-yield savings accounts, so I want to discuss their differences today. I aim to help you find a high-yield savings account that motivates you to save passionately.

The three high-yield savings accounts I will discuss today are Discover, M1 Finance, and Samsung Money by Sofi. Let’s begin.

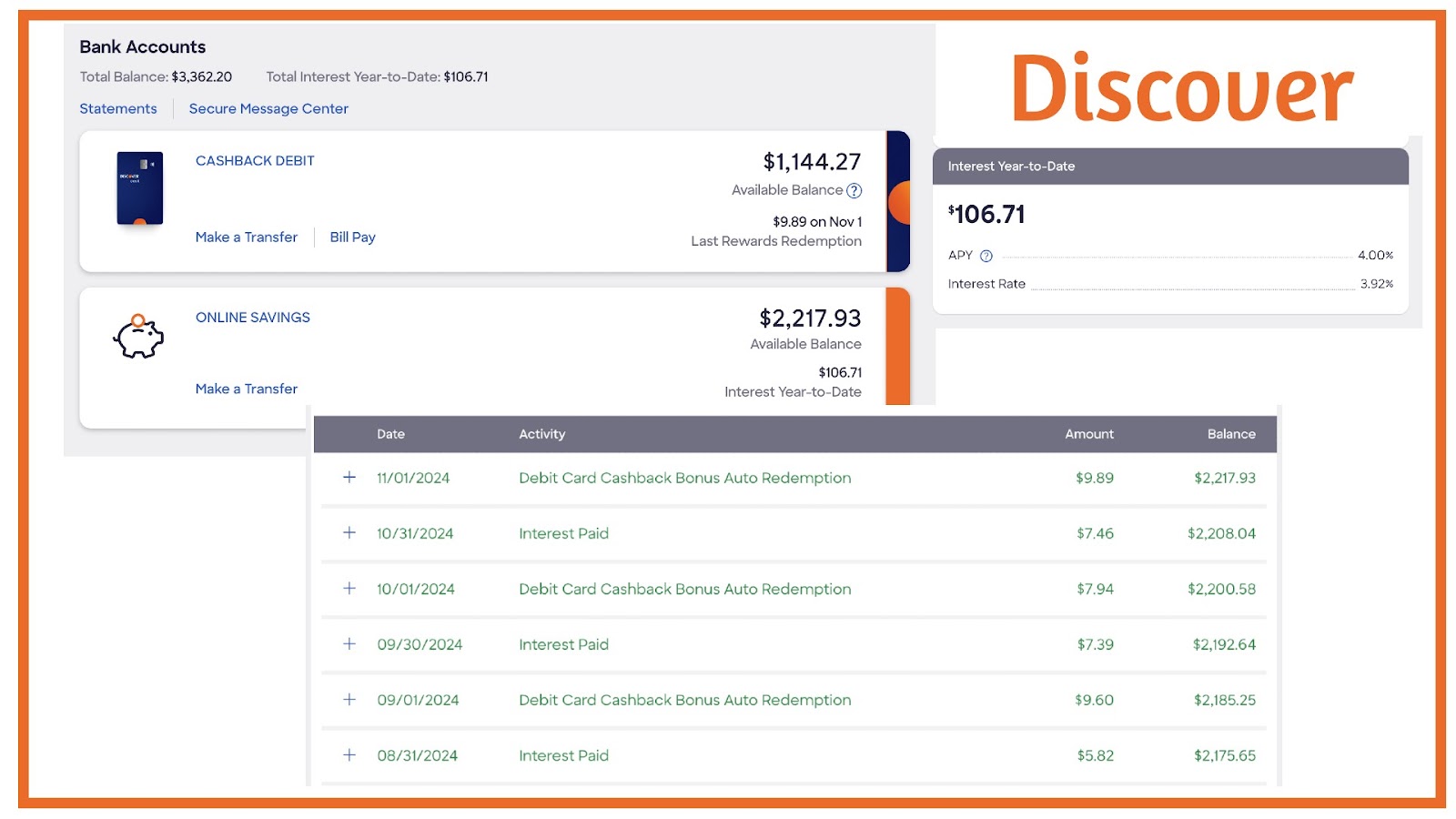

The magic of a Discover high-yield savings account. I opened my first high-yield savings account in June 2019. I was just learning about the magic of compound interest and wanted to start taking advantage of higher interest rates from banks.

I have been writing about my Discover high-yield savings account ever since. It may still be my favorite high-yield savings account because of its simplicity. My Discover HYSA is rather low right now because I used this account to drop a down payment on an RV recently ($10,000).

Today, Discover is paying 4% interest on my saved money. This is the lowest of the bunch, but there is a big caveat—their cashback rewards debit card.

Why Rents Will Continue to Rise

I wrote about their cashback debit in “Just Rewards: Credit Cards vs. Debit Cards.” The quick notes are that whenever I make a purchase using my debit card, they will deposit 1% of the purchase price into my HYSA at the end of the month.

I have been using my Discover Debit Card to maximize my rewards payments for over three years. And yes, I would rather use my debit card than credit cards for rewards. I hate credit cards. Period.

Outside of their debit card, Discover has the best customer service of all of my financial institutions. For 24 hours a day, they have an American representative.

It’s also easy to link external accounts to your high-yield savings account. This is vital because you never know when you will get a random windfall that you want to save.

Overall, Discover is still my favorite high-yield savings account because it exists outside of all of my other financial traffic. It sits alone with the sole purpose of making me money every day. Thank you, Discover HYSA.

The True Value of Owning a Home

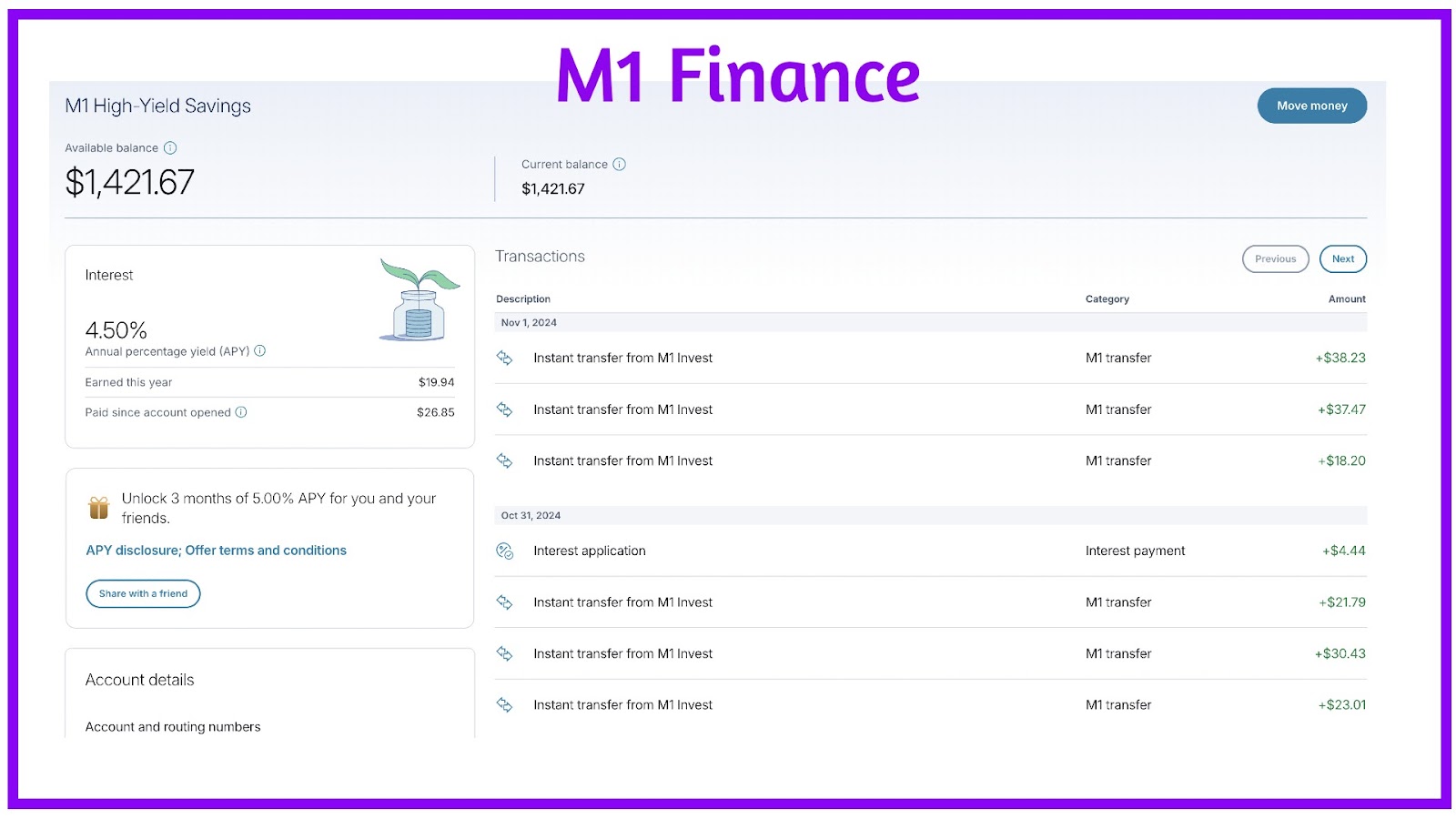

The Dividend Savings Account (M1 Finance). I joined M1 Finance in late 2020 for their amazing brokerage account. Their brokerages use a “pie system” that helps balance your investing over time.

M1 Finance opened a high-yield savings account about a year ago, offering an amazing 5% yield. However, I did not need an additional HYSA at the time. Currently, M1 Finance HYSA pays 4.5%.

About six months ago, M1 Finance added a function that allowed dividends from my brokerage account to be deposited automatically into my M1 Finance HYSA. That was a game-changer.

I wrote about this amazing feature in “The Dividend Savings Account.” The gist is that now I can turn on automatic HYSA investing, and my dividends will do the rest.

Every month, I feed my three M1 Finance dividend accounts (dividend growth, bond growth, income investing), and their dividends feed my Discover HYSA.

Turn a Reverse Mortgage into an Income Investing Portfolio

It is a glorious circle. I plan on keeping HYSA reinvestment indefinitely. I will simply keep adding money to my dividend portfolio with new capital.

I like the idea of capturing dividends in an HYSA because it will be helpful in an emergency. I know that if I need to take money from my M1 Finance HYSA, my dividends will replenish the amount without any effort from me. That’s a great feeling.

My only high-yield checking account. My Samsung Money by SoFi account is amazing because it is not a savings account; it’s a checking account.

My SoFi account is the most technologically advanced of the bunch. I like the account because I am a massive Samsung fanboy. A huge one!

My beautiful Samsung S22 Ultra has an excellent place for my digital Samsung Money card. I can also access my Samsung Money Account directly from my phone.

Even better, I can also access my Samsung Money account from SoFi’s website. I opened a brokerage account at SoFi to partner with my High-Yield Checking Account.

The True Costs of Owning a Home

I wrote about my SoFi brokerage account in “30 Monthly-Paying Dividend Stocks.” I think it is incredible to have a high-yield checking account integrated directly into my Samsung phone.

My Samsung Money also comes with a physical debit card. This is the final touch I love so much about my Samsung Money account.

On a side note, I am also a massive SoFi fanboy. I own their stock and plan to keep it for my lifetime. So, do you understand why I love this account so much?

I love Samsung, I love SoFi, I love high yield (4.25%), I love checking accounts, and I love technology. This is just a great account.

Stock & Bond Investing in Your 50s

On a sad note, I have never used my debit card (either digital or physical). I will need to go use it one day just for giggles.

How do you like to save? All of these accounts have one thing in common: they make it fun to save. The goal of life is to ensure one emergency doesn’t break the bank.

Saving money is one of two important things we can do to ensure our futures are bright and full of success. The other thing we can do is invest.

I remember being in serious credit card debt (-$77,000) and having nothing in savings. Now, I have +$33,000 across checking, savings, and bonds. I have no credit card debt.

If you are not on the savings train, it is time to start. These banks reward you for storing your money in their accounts. Will these higher interest rates last?

Being Mediocre in Not Okay

I think bank interest rates will stay above 3% for the foreseeable future. Even if rates go down, saving is still vital to our future survival.

Conclusion. I hope these three accounts resonate with you. I love how different and similar they are. I get excited every time I get to add money to each of these accounts.

I have come a long way from having three maxed-out credit cards. I am now working on maxing out my high-yield savings account instead.

I made the switch in my mind to not let the world beat me down financially. I took control of my financial situation by learning about compound interest and passive income.

Now, I can look into my account and see no negative or red symbols. I am firmly in the positive. I am so excited to discuss these high-yield savings products with you. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply