For years, I stuffed my money in a standard savings account at Wells Fargo, which has a measly 0.01% interest rate. They should be ashamed of themselves.

In 2019, I learned about high-yield savings accounts and immediately opened an account at Discover. My favorite high-yield savings account pays 4.10%, an enormous increase from Wells Fargo.

However, even my Discover HYSA cannot keep pace with my income-investing portfolio, which pays over 10%. Wouldn’t it be great if my income-investing portfolio fed its dividends into my HYSA? That way, the process could happen without my oversight.

Minimalism is Now a Necessity

Today, I have an income and dividend growth investing portfolio that feeds dividends directly into a high-yield savings account. This method is an incredible way to save and invest in the modern day. Let’s look at how this new technique can change your life.

Along came M1 Finance. I opened my M1 Finance in August 2020. I have slowly built this brokerage account into something amazing.

M1 Finance is a powerful brokerage account because of the “pie” system it employs. You start a pie and add slices. Slices are different stocks, ETFs, and Closed-End Funds.

The pie attempts to keep your allocation preference to each slice. However, sometimes stocks grow faster than the bunch. When you insert money into the pie, it smartly pushes the cash to which stocks need it most. Let’s call it a “self-balancing system.”

Over the years, I have built three separate pies under my M1 Finance portfolio: a dividend growth investing portfolio, a bond growth investing portfolio, and finally, an income investing portfolio. Together, the portfolio amounts to $51,184.

The exciting part is that each portfolio produces roughly $100 in dividend income, for a total of $300 per month. Typically, I let these dividends reinvest themselves across their respective pies, but I changed something recently.

What is Your Investment Philosophy?

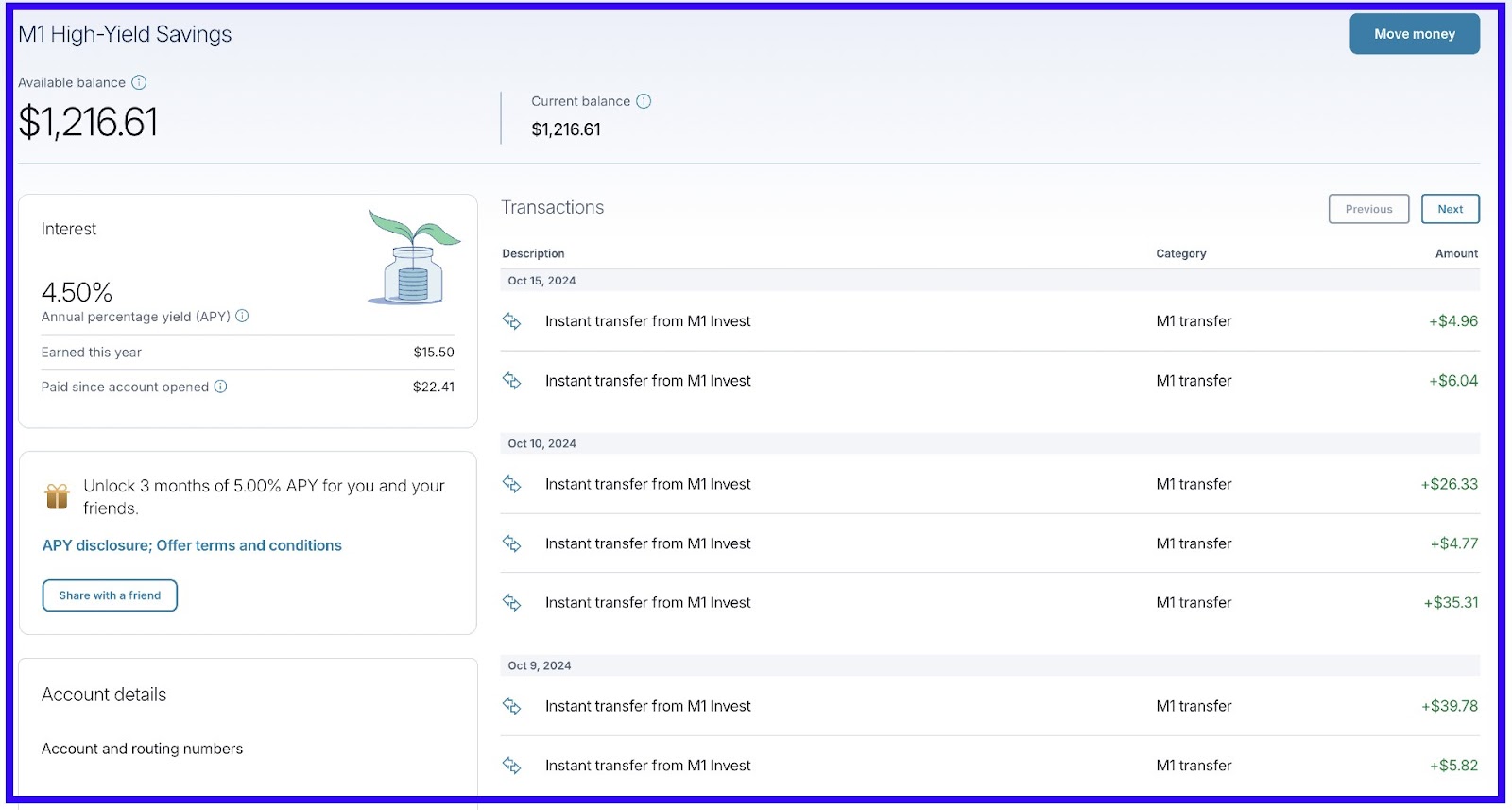

A new HYSA to rule them all. M1 Finance started a high-yield saving program with a starting interest rate of 5% (now 4.5%). Of course, this rate caught my attention, and I signed up quickly.

However, it was too tough for me to transfer money into this account. It required too much brain power to go to a website and click through a few web pages.

Remember, you want the least amount of “friction” possible when it comes to saving and investing. So, my M1 Finance HYSA floundered for a few months.

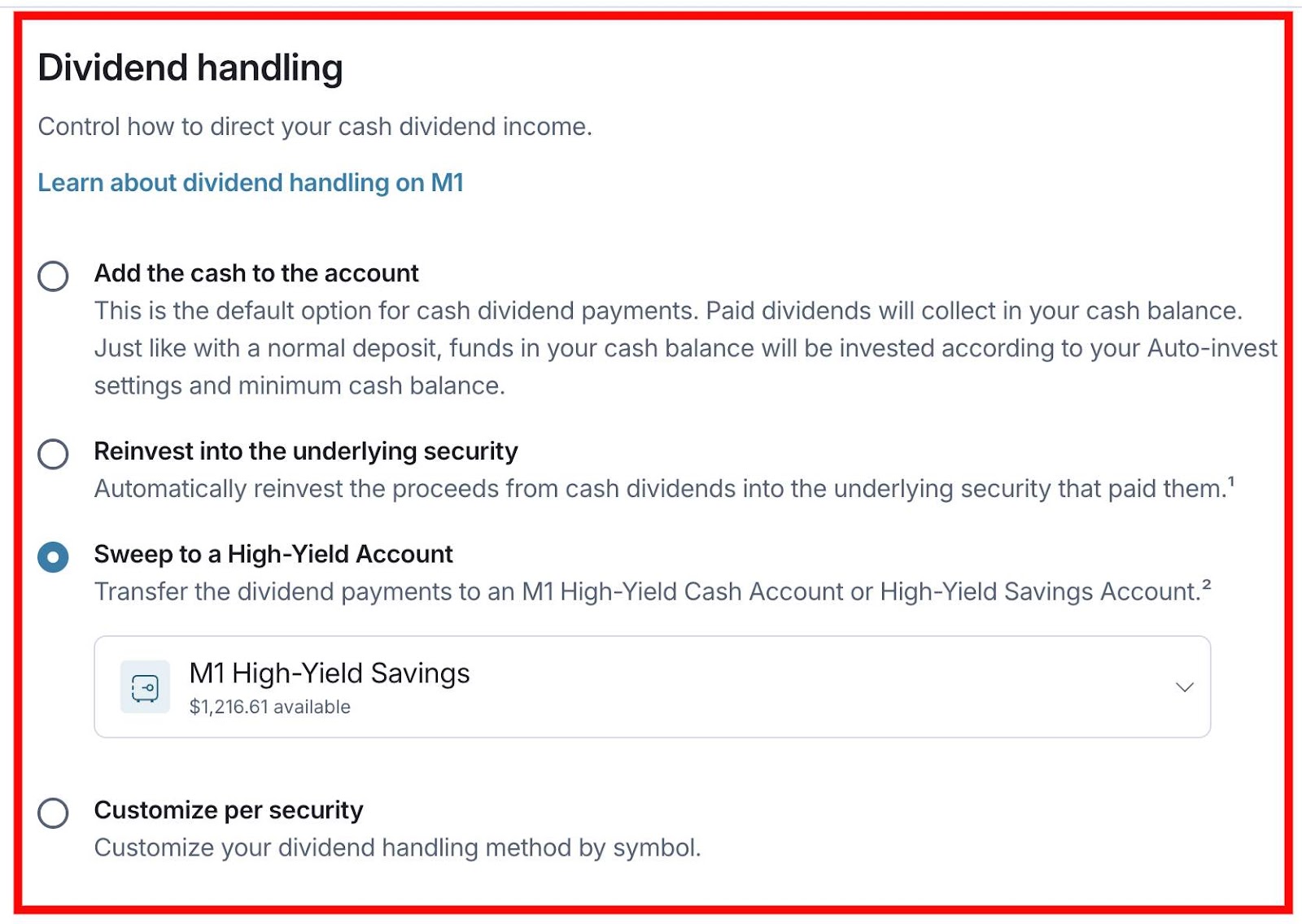

One day, M1 Finance changed the game’s rules by giving us the option to decide how we wanted our dividend to be allocated. They give us four options:

- Add the cash to the account

- Reinvest into the underlying security

- Sweep to a High-Yield Account

- Customize per security

How exciting! Of course, the third option is what excites me the most. Now, I could just wake up and see my M1 Finance High-Yield Savings Account growing substantially.

Saving is Defense: Investing is Offense

Why is automatic HYSA investing so exciting? You may ask, “Josh, why is automatic HYSA investing so exciting? ” because I am building not only a massive dividend portfolio but also an emergency cash fund.

Every month, I invest $100 into each M1 Finance pie for a total of $300. My M1 Finance portfolio pays me $300 in dividends, which go directly into my M1 Finance HYSA.

Therefore, each month, I buy more shares of dividend stocks and funds, which pays me more income. It is a glorious loop.

The reason this is so exciting is because now, more than ever, we must have cash on hand for emergencies. Did you see the damage from the two major hurricanes (Helene and Milton) in fall 2024?

What is Your Relationship with Money?

The people who had financial resources (cash) were able to evacuate and pay for hotels, rental cars, and supplies. Those who didn’t have the resources were stuck between a rock and a hard place. We must learn from these situations.

My overall savings plan. I have three high-yield savings accounts that I am slowly building up. I consider my Discover HYSA my emergency fund: the big boy.

However, I need more “contingency-based” savings accounts for direct emergencies. Dave Ramsey says you should never use your emergency, so I am creating more accounts that prevent me from tapping into my Discover account.

My M1 Finance account will serve as a “disaster” emergency fund. Hopefully, I can get this account to $10,000 over the next few years. Even $5,000 is an amazing amount of money to have in a natural disaster.

The Metaverse 117: Return to the Metaverse

My final high-yield savings account is actually a high-yield checking account created by Samsung Money and SoFi. It pays $4.25% and comes with a physical and digital debit card. I hope to increase this account to $10,000 over two years.

Dividends Forever! I will always love investing in dividends. I wish I could just build up $10,000 in an emergency fund and invest the rest in dividends.

However, I must always keep my eye on current and future events. It is obvious that these insurance companies will not pay us out during a natural disaster. FEMA will not be there to support us when we need them.

Therefore, we must take matters into our own hands. Every American household needs $100,000 in various savings accounts. This will give us the power to “self-insure” and also become a bank for our children.

We do not want our kids to pay 30% interest on credit cards, do we? That’s why I have turned my focus to saving a massive lump sum of money.

What is Your Risk Profile?

I still invest $2,000 to $3,000 per month into my various brokerage accounts (I have six), but after watching the hurricanes this year (I live in Florida), I truly understand that cash is King.

The magic of high yields. We are living in a special time when we can get 4-5% interest rates on our money. Of course, we must do more than this to outpace inflation, but this is a great start.

I am also investing $350 monthly in Series “I” Bonds because they will perform better over the long run than high-yield savings accounts.

All of this is to say that M1 Finance has created a wonderful program that allows me to feed two birds with one stone. I insert $300 into the top of my dividend funnel, and $300 comes out directly into my M1 high-yield savings.

Saving & Investing with $1,000 Per Month

Conclusion. The magic of saving and investing is the ability to change direction as required. This 2024 hurricane season has changed my thinking about the size of my emergency fund.

Those with the most cash and cash flow win. This means that you need cash upfront, but you also need cash flow (outside of a job) to sustain you.

I already have over $2,200 in monthly dividend income, but I need to build a massive emergency fund to ensure that my family and friends remain safe as disasters arrive; that’s the power of saving and investing.

I truly love the M1 Finance high-yield saving and dividend investing programs. When combined, they are even more powerful.

In an evacuation situation, saving money alone will not protect you forever; you will also need cash flow (dividends) to sustain you. Therefore, we need both cash and cash flow, and M1 Finance gives us both options. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply