People in their 20s have trouble with their finances because they have two objectives: building wealth and funding their future.

The financial media always tells the younger generation about compound interest and how vital it is to save and invest early in life.

The stark reality is that people in their 20s must contend with getting married, having kids, going to college, finding a job, and saving for retirement.

Dividend vs. Social Security

The American Dream costs $8 million (up from $5 million three years ago). However, there is light at the end of the tunnel. With some financial education, young people can build wealth while setting themselves up for economic success. Let’s dig in.

Happy Cash Flow Retirement. I created the term Happy Cash Flow Retirement to describe a future where you have multiple streams of passive income.

The great part about a Happy Cash Flow Retirement (HCFR) is that you can start living that life today. The sooner you understand the principles of passive income, the faster you’ll be sitting on the beach collecting dividends.

Happy Cash Flow Retirement 7

Investing is one major part of an HCFR, along with business, rental, royalty, and retirement income. Under the investing category, we must define risk in a way that is particular to our personal situation.

We use various assets, including bonds, stocks, and options, to mitigate risk across different parts of our portfolio. Typically, the more people we support financially, the less risk we want to take.

This doesn’t mean we can be overly risky in our 20s; it simply means we have more leeway to learn, take risks, and make mistakes. Let’s build a safe, high-yielding portfolio using all of our financial assets.

Bond investing in your 20s. Before we buy one bond, we want to ensure we have a nice-sized emergency fund based on our lifestyle. A car is the primary liability a typical 20-something uses daily.

Use Royalties to Supplement Your Retirement

Therefore, I would say building a $5,000 emergency fund would cover car repairs or having to move apartments suddenly. You can start buying bonds once we have $5,000 in a high-yield savings fund.

The only type of bonds you need in your 20s are Series “I” Saving Bonds from the US Government. They are safe, accessible, and convenient. The only issue these bonds have is that you can only purchase $10,000 of them per year.

Series “I” Bonds will act like the glue to hold your emergency fund, bond, and stock portfolios together. Because they are so reliable, they can serve as an extension to your emergency fund.

However, they also grow along with inflation, meaning they can act as a growth element. You also don’t pay taxes on the growth until you redeem them in 30 years. Plus, you can avoid taxes if you use them for qualified education purposes.

Build Your Rep: Create Your Bondy of Work

People in their 20s should aim to invest $200 to $300 per month in Series “I” Bonds. It sounds like a lot, but be creative. Imagine having these bonds mature in your 50s, creating another passive income stream for you in the future.

Stock investing in your 20s. The most challenging part of your 20s is controlling your FOMO or Fear Of Missing Out. Social media will convince you that your investments should double every few months; disregard this insanity.

The best advice I can give is to build wealth slowly. If you can earn 10% annual returns for 30 to 40 years, you will be wealthier than you can imagine.

For example, let’s say you invest $20,000 in your stock portfolio by age 30. If you let that sit, earning 10% yearly, you would have $350,000 at age 60. That’s the magic of compound interest.

From Dirt to Dividends 2: Livestock and CEFs

Now, how do you get $20,000 into your stock portfolio? A good rule of thumb is to reduce your cost of housing (shelter) and invest the difference.

That can mean renting a room instead of an apartment or living with parents. You can figure something out if you truly want to become wealthy.

As sexy as it is to be an investor, living with your parents will earn you much higher returns than you can ever earn on the stock market. Read my article, “Selling Covered Calls vs. Rental Rooms,” for more information.

Now that you can set aside $1,000 per month because you live at home, how do you split your investing dollars? I would put 50% of my stock money into index funds and the other 50% into dividend growth investing.

Index funds allow you to grow your wealth with the most powerful wealth generator in the world, the US stock market. You simply put your money into one of my four favorite index funds (QQQ, VTI, SPY, DIA) and sit back and relax.

Retire by Age 38 in 10 Steps

However, you also want to jump into dividend growth investing (DGI) stocks. There will come a point later in life where it will become extremely tough to invest, usually when you have a spouse, kids, and a mortgage.

You will want to have access to passive income from dividends. For example, I have $65,000 in my Cash App, mainly in DGI stocks. They pay me $400 per month.

Having a $400 income stream in my 20s would have set me free. I had some rough times in my 20s and 30s because I didn’t have enough cash flow. DGI stocks are a powerful resource you can tap into without selling shares.

Options trading in your 20s. Options trading in your 20s is akin to pouring gasoline on a fire. Again, social media will convince you to double your portfolio with options trading—every month.

Can You Retire on Dividends from Index Funds?

Aiming for 30% annual returns from your options portfolio is a better idea. A good rule of thumb is to match the size of your options portfolio with your emergency fund.

In this case, you have $5,000 in your emergency fund, which you can match with $5,000 in an options portfolio. Aiming for 30% annual returns means you would have $6,500 at the end of the year.

You don’t have enough money to make a good income stream by selling covered calls or cash-secured puts. In this case, I would use monthly long strangles.

It’s safe to say you can safely earn $200 per month by purchasing $1,000 in long strangles per month. If you earn $200 monthly, that would give you $2,400 in profits. You can take that $2,400 and place it in your DGI or index fund portfolios and restart with $5,000 the next year.

As you can see, your options trading portfolio is a high-growth element in building wealth. However, you must be careful in this world, as your fear and greed emotions will be on full alert.

REITs vs. Homeownership

Also, there are many ways to trade options, so you don’t need to use my methods. You must use the tools that align with your temperament and risk tolerance.

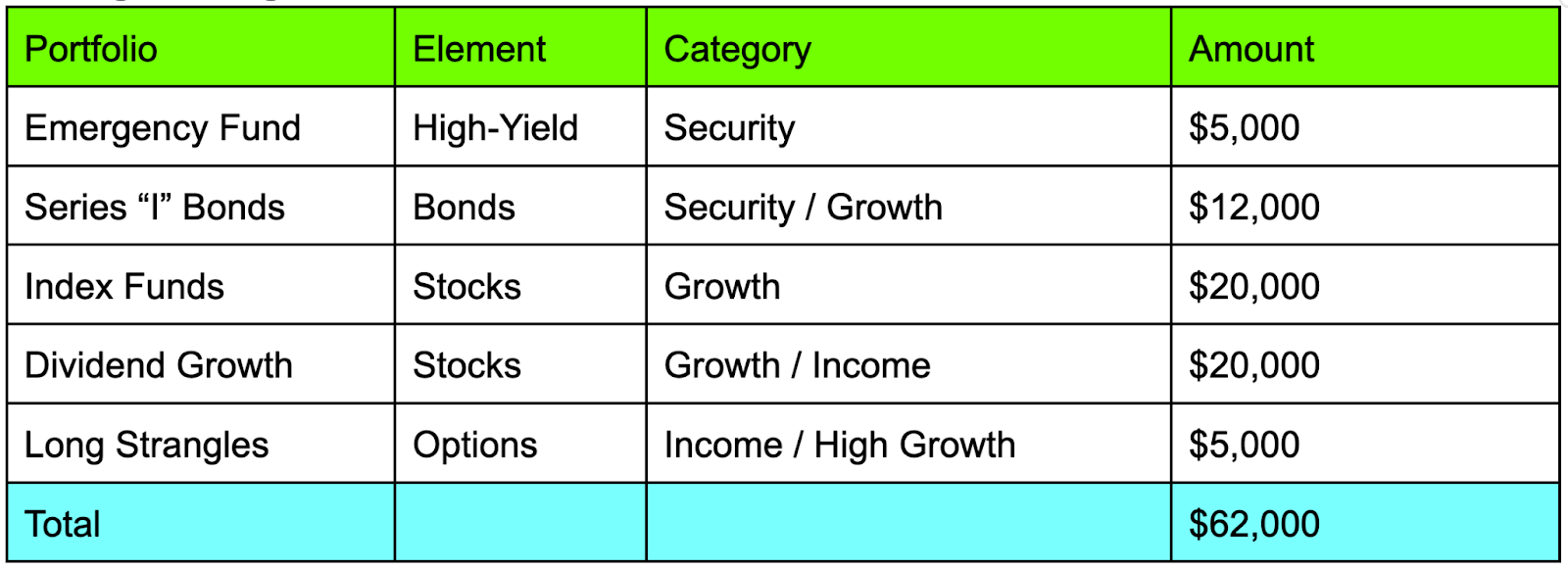

Putting it all together. Let’s take a look at our financial goals in our 20s. It may be tough to get these numbers, but even having some type of plan will pay off in spades.

As you can see from the chart, you can aim for $62,000 by the time you turn 30. Is it possible to save and invest this much in your 20s? Absolutely.

Most people look at their 20s as a time when they are broke; however, let’s flip the argument. In your 20s, you don’t need to support anyone; you can live at home and take risks.

Your physical capabilities are strong, and you do not have any sickness or back issues—you can work many hours.

Conclusion. Most importantly, you can use options trading to single-handedly fund your other portfolios. If you place $10,000 in an options portfolio and make $4,000 monthly long strangles trades, you can earn $400 to $800 monthly profits.

Is Your Neighborhood Overtaken by Investors?

Let’s say you earn $5,000 in options profits each year. If you can do that for ten years, that’s $50,000 (minus taxes) right there.

When you add options trading to living at home or renting a room, you have a recipe for wealth. Also, your Index funds and DGI stocks will continue to grow on their own.

The key to life is obtaining assets and letting them grow naturally. Options trading is more hands-on (and risky), but the rewards can be stunning.

You balance the risk of trading long strangles by having an emergency fund and purchasing Series “I” bonds. This multi-tiered portfolio creates a symbiotic financial relationship so that you can build wealth peacefully. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply