There are many ways to retire on dividends, but you’ll have to pick the best path according to how you want your future life to look.

Some people love to see their portfolio’s total value grow and compound, while others prefer to see their portfolio’s income grow and compound.

Welcome back to the Retiring on Dividends 101 series (101), where we discuss how much your retirement dreams come true.

Your Daily Routine Is Your Success

What is Dividend Growth Investing (DGI)? If you love to look at the size of your portfolio more than its income, then dividend growth investing is for you.

Dividend growth investing uses four compounding elements to ensure your portfolio becomes larger than life. These four elements are dividend raises, share price appreciation, dividend reinvestment, and dollar-cost averaging. Let’s explore these quickly.

- Dividend Raises. This is when a company raises its dividend annually to combat inflation and give shareholders a larger piece of the profits.

- Share Price Appreciation. The share price of a company should grow along with profits and dividends.

- Dividend Reinvestment. You’ll want to reinvest all dividends until you hit retirement age. This maximizes the power of compounding.

- Dollar-Cost Averaging. You want to invest the same monthly amount of money into the markets. As you earn more, you can increase your investment allowance.

Using these four principles of DGI, you’ll grow your wealth over time. DGI is akin to owning a rental property. As time passes, the value of the home increases, along with the rent you can charge.

The goal is to own a massive DGI portfolio that also pays a significant amount of dividends. Today, I want to focus on achieving this goal with high-growth companies with fast-growing dividends.

Middle-Class Investing 108

Finding high-growth DGI companies. Searching for high-growth companies with fast-growing dividends can be trickier than pulling up a list of dividend aristocrats.

You can search for companies that pay dividends with less than a one percent yield. You can also search for companies that just initiated a dividend.

Here are some of my favorite high-dividend growth companies: Visa (V), Mastercard (MA), Apple (APPL), and Microsoft (MFST).

Here is a list of companies that just started paying a dividend: T-Mobile (TMUS), Facebook (META), and Google (GOOG).

But why is investing in high DGI growth companies vital to your retirement planning? Why not just invest in index funds?

DGI versus Index funds? Although index funds and high-growth DGI look similar, one stark difference is the dividend growth rate.

Compound Interest: You Can Either Pay It or Earn It

Let’s say Facebook (META) continues to compound its dividend at a 10% annual rate. Over time, that compounding would produce some serious income in 40 years.

You could also benefit from outsized growth compared to a standard S&P 500 index fund (SPY). If you own 20 DGI stocks, two or three will beat the market in total returns. Others will beat the market in dividend growth and payments.

Many people have made fortunes by purchasing DGI stocks early in their lifecycle. Warren Buffett makes billions of dollars from Apple (APPL) and Coca-Cola (KO) dividends.

The goal is to get in early and let the power of compounding work its magic on your portfolio and dividend income.

Getting started with high DGI growth. The first thing you want to do is find your preferred investment platform. I use six different ones because I love choice.

Middle-Class Investing 107

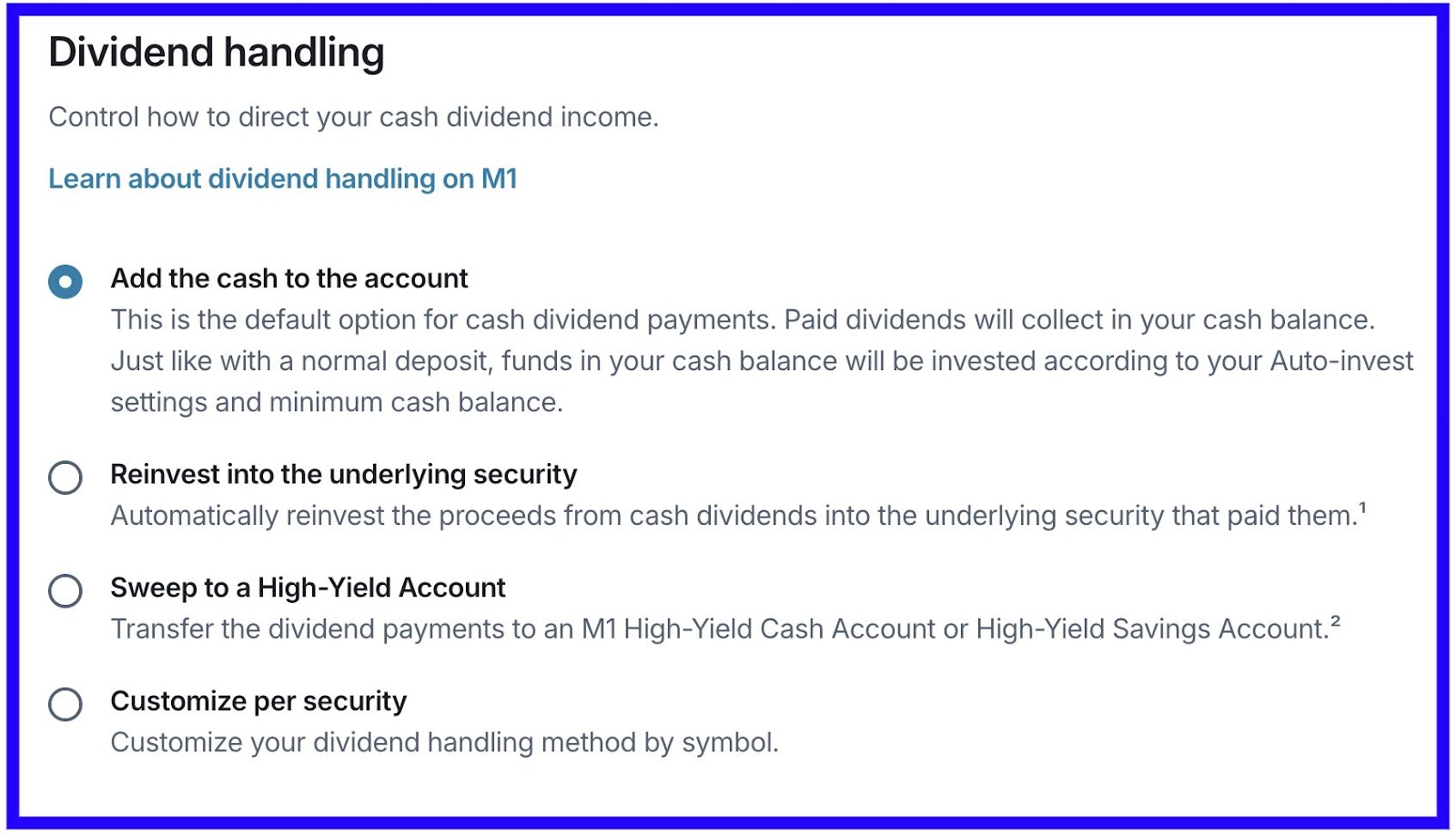

I recommend M1 Finance or STASH. With M1 Finance, you can put all your high DGI growth stocks into one pie and automatically transfer a set amount of money.

The M1 Finance algorithm will purchase the best stocks during your transfer. You can also set how you want your dividend payments to behave.

STASH gives you many options as well. For example, you can allocate $5 weekly to each stock. You can also purchase stocks any time you want or drop $50 into your portfolio and pick certain stocks whenever you choose.

The goal is to automate as much as possible. You don’t want to have to log in to make these things happen. Currently, I automatically transfer $50 to STASH and $150 to M1 Finance at the start of the month.

Keeping up with your stocks. Although you don’t want to check in on your stocks daily, you will want to update your spreadsheet monthly.

Home-Buying for the Average Person 2

To be a good dividend growth investor, you must document your monthly dividends and pick stocks that pay consistently across different months.

Stock usually pays quarterly dividends. Therefore, you want stocks that pay in January, February, and March.

For example, Coca-Cola (KO) pays in January, Mastercard (MA) pays in February, and Facebook (META) and Google (GOOG) pay in March.

You want to keep your months reasonably even as you prepare for retirement. You don’t want to earn $1,000 in January and $4,000 in February.

Middle-Class Investing 106

DGI is not for current income. You don’t become a high-growth DGI for your current income. This means you don’t want to use your dividends in daily life until you are 60 or 70.

If you want current income, you want to become an income investor or invest in high-yielding dividend stocks like AT&T (T) and Verizon (VZ).

The good part is that you can mix and match strategies. Ultimately, you want enough cushion (income) elsewhere in life to keep your high-growers compounding.

Two People, One Budget

It is vital to have a fully funded emergency fund. This fund will prevent you from selling stocks to generate income. Remember, the overall goal of dividend investing is never to sell shares to generate income.

Conclusion. Are you a high DGI growth investor? If you love staring at unrealized gains, you are probably one.

I am an income investor through and through. However, I can appreciate the beauty of seeing a stock like Apple (APPL) kicking butt and taking names.

Most people love to brag about capital gains at the detriment of income. In fact, many people invest in stocks like Tesla (TSLA) and Nvidia (NVDA) that don’t pay dividends.

Middle-Class Investing 105

High DGI growth investing gives you the best of both worlds. You never want to sell shares, so you want to have your investments generate dividend income.

However, if you love capital gains, then this is the best method for you. The best way to become a great investor is to follow your heart.

Find your niche, and stay with it. I love income investing because it is all math. You invest purely for the income that a company or fund produces.

For high DGI growth, you invest in the company’s story and outlook. You want to hold these companies for 40 to 50 years.

In fact, you will retire on dividends because of these companies. If that sounds amazing, dabble your toes in high DGI growth investing. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply