They taught us to work for money. Working is so ingrained in our nervous system that we get anxious when not working. When we aren’t working, we feel the world will collapse upon us.

But the rich don’t work for money; they work for assets. Once they have enough assets, the assets work for them.

Thanks to the internet and cell phones, everyone can purchase dividend-paying stocks and build a portfolio of assets. If you obtain enough of these stocks, you can retire from the dividends they produce.

Achieve F.I.R.E. via Income Investing

The most important part of retirement. The most important part of preparing for retirement is creating (and sticking to) a budget. Before leaving the workforce, you must know how much you require to fund your lifestyle. It makes sense.

The less we require to live, the faster we can leave the workforce. Earning $5,000/month in dividend income is more accessible than earning $10,000.

Most people wait until retirement to determine their budget, which perhaps explains why they stay in the workforce until they can no longer work. They simply believe more money is the better route.

However, a tighter budget is the best way to retire. Once you retire, you can always make more money. In fact, dividends are just a portion of the passive income you can generate.

Let’s start from the beginning. Suppose you are 40 years old and make $10,000 per month. The fastest way to determine your retirement goal with a $10,000/month budget is to multiply your annual income by 25.

Becoming an Entrepreneur #1

In this case, we would multiply $120,000 by 25 to get $3,000,000. This means if you want to live on $10,000/month, you would need to invest $3,000,000 and withdraw at a 4% annual rate.

But we can do better. Let’s say you can retire on $5,000 per month. This would reduce the amount you need to $1.5 million.

The key to retirement is beginning to live on $5,000 per month NOW. Don’t wait until you are 65 to live on a fixed income; start the process now.

Living below your means. Most people do not want to live below their means, although this is the fastest way to retire early.

How do you reduce your lifestyle from $10,000 monthly to $5,000? Well, drastic times call for drastic measures. Reducing housing costs is the number one way to cut your household budget.

Position Yourself for the Next Bull Run

There are many ways to reduce housing costs, such as getting a roommate, downsizing your home, moving in with parents, living in a small town, or moving overseas.

Pick your poison. My wife and I got roommates for five years, which reduced our housing costs to zero out-of-pocket. That was the key to letting us retire early.

To retire on dividends, you must understand how money works. The goal of the process is for your money to produce more money.

When you save money on housing, you don’t spend it frivolously. You use the additional cash flow you created to invest in dividend-paying stocks.

The more money you invest, the faster you can retire. In our example, investing $5,000 monthly will set you free quickly.

How to Start a Business Cheaply

Why don’t more people retire on dividends? Retiring on dividends requires discipline most people don’t possess. For most people, it is all about today.

To retire on dividends requires delayed gratification. My first month of dividend investing netted me $0.25—for the entire month.

But this amount has gone from $0.25 to $25 to $250 to $2,000 over the years. We are well on our way to reaching $2,500 per month in dividends.

We have been investing in dividends for five years. Can you imagine how much money we will make in another ten years? Twenty years?

My wife and I retired on my military pension; however, dividend investing is still my goal. I want my dividends to pay me more than my pension, and I suspect that will happen in about 15 years.

Change Your Money Cycle

Increasing your income. There are only two ways to get rich: reducing expenses and increasing income. We talked about living below your means to generate more free cash flow, so now, let’s make more money.

The key to retiring on passive income is to start making passive income while you work. If you have debt, you should get a second job.

However, the intent is to create passive income streams that will give you more cash flow to invest in dividend-paying stocks.

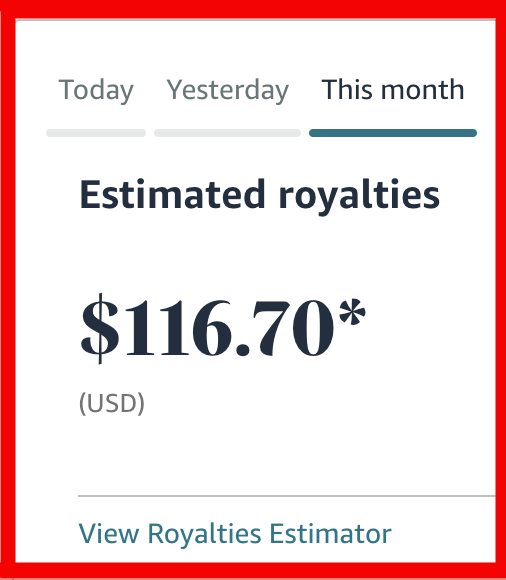

What is passive income? Passive income is when you do the work once and repeatedly reap the benefits. Writing a book is the perfect example.

You write a digital book that can produce income for your lifetime and 70 years afterward. You can repeatedly collect royalty payments from your one book.

So far this month, I have made $116 from my books on Amazon. Although I write daily, my income comes from my past work. If I stopped writing, I would still generate some genuinely passive income.

Rental Income vs. Income Investing

Other ways to create passive income include starting a video channel or podcast. You can also rent a room, your car, or a storage shed.

Try to create something where you don’t exchange time for money. You can use whatever income stream you produce now—and during “retirement.” The goal for retirement is to have multiple streams of passive income.

How I retired. My passive income during retirement year one is a military pension ($9,000 per month), dividends ($2,000), rents ($700 after mortgages), and book royalties ($200).

The Department of Veterans Affairs (VA) will also pay me to attend college starting next month. That will generate $1,700 per month is semi-passive income.

That’s a lot of money in retirement. But the key is that my wife and I can survive on $6,000 monthly. Therefore, we aim to save and re-invest at least $2,000 annually in dividends.

Dividend ETFs vs. Index Funds

I am 43 years old and have been retired for almost a year. Can you imagine these numbers in ten years? Even though we are not in the workforce, we are still saving and investing!

Conclusion. Dividends can help you retire soon; however, the key to retirement is your budget. You will live and die based on your budget.

I know most people don’t want to live below their means. They want to take their big paychecks and go to Disneyland today.

Power Writing: Write a Book in One Week

However, not working is the most enjoyable way to earn money. My wife and I have time to focus on our kids, health, and wealth.

We can ensure our kids start with a dividend portfolio now, at a young age. They will leverage the power of compounding at age 14, not 38, like I did.

The fastest way to retire on dividends is to determine how much you require to live on. The lower the number, the faster the process can work.

There is nothing like receiving dividends during retirement. Dividends are guilt-free money; enjoy them. Throughout this series, I will help you learn to appreciate your wealth via dividends. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply