Most of us don’t have a lot of money in our 20s. In fact, we spend our 20s trying to have fun on a budget. If you can devote just a tiny portion of your 20s to income generation, you can exploit the power of compounding at an early age.

But what is the best way to build wealth in your 20s? You can start a business, invest in dividends, earn your education, or purchase real estate.

Another avenue is to start trading options. Options trading can fast-track your wealth OR destroy any chance of building a life. Only you can decide which path you’re trading will take.

- Dividend Investing in Your 20s

- Bond Investing in Your 20s

- Stock & Bond Investing in Your 20s

- Staying Debt-Free in Your 20s

- Real Estate Investing in Your 20s

- Retirement Planning in Your 20s

The power of 30%. It’s not unheard of for options traders to double their investment portfolio yearly. However, I believe aiming for a 30% annual return can do wonders for you in your 20s.

Series “I” Bonds vs. Roth IRAs vs. HSAs vs. 529 Savings

Let’s follow the numbers. Investing $5,000 in your options portfolio at 30% return yields you over $12,000. Over 30 years would yield you $68,000.

The toughest part of trading in your 20s is fighting the urge to go bigger and badder. Trading options can make you feel like the hero of time or the dumbest person on Earth.

Most young people want to double their money in 2-3 months—this is simply not how money works. Doubling your money in one year would be a 100% annual return; remember, high-yield savings accounts pay a 5% yield on your cash.

Understanding risk. The best way to understand options trading is to understand risk. The first place to look is where you can earn a risk-free return.

There are a few places to earn a risk-free return: high-yield savings, money market funds, treasury bills, and certificates of deposit. Currently, you will earn 4-5 % yields on these products.

The Leverage Millionaire

To earn 8-12% returns, you must invest in high-yielding products like business development companies, real estate investment trusts, closed-end funds, and preferred shares. These come with their own risks but are much safer than trading options.

This brings us to options trading as a source of income. There are many reasons to trade options (speculation, hedging), but I like income generation the best.

Let’s invest $5,000 in our options trading portfolio. Okay, let’s say you saved $5,000 in your brokerage account, and now you want to start generating income.

If you have this much money, selling cash-secured puts and covered calls is an excellent place to start. Selling options is the safest way to partake in the options market.

These two products require you to own the underlying 100 shares of the assets or have enough money to purchase 100 shares of the stock.

Becoming an Entrepreneur #2

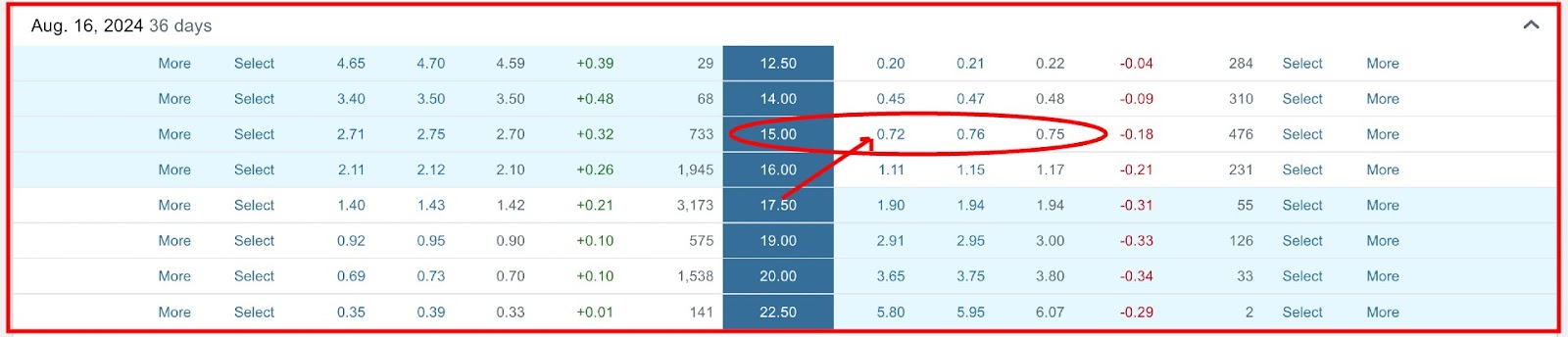

I like to trade young, volatile stocks like Rivian (RIVN) and Palatir (PLTR). Right now, RIVN is trading for $16.91. That means we can sell three cash-secured puts with a strike price of $15.

Those three puts would net us $72 each, or $216. Earning $216 per month for 12 months would give you an annual return of 51% (based on your original $5,000).

This is a great deal of money, but it takes patience. You must resist your fear and greed meter, which is challenging at a young age. The less risk you take in the options market, the less you earn. However, your goal should be to beat inflation, not get rich in one year.

Getting started with options. The most challenging part of trading options is building your initial capital. As a young person, you may be tempted to use margin to use someone else’s money to get rich. I would advise against this.

Annuities vs. Income Investing

The simple fact is that most people lack the discipline to save $5,000. Once you build your $5,000 nest egg by yourself, you are more likely to protect it at all costs.

The ultimate goal of investing isn’t to have a massive options trading portfolio; it’s to take those proceeds and put them into real estate and dividend stocks. In the end, dividend stocks and rental income will set you free—not risking your money every month.

Let’s do some math. Let’s say you can generate $200 per month using the options wheel strategy with your $5,000 portfolio. You generate the same $200 monthly for ten years (or 120 months).

You take that $200 monthly and invest in an income-investing portfolio that yields 10%. At the end of ten years, you have your $5,000 options portfolio and an income portfolio at $38,000. Your income portfolio would pay at least $3,000 annually (or $316 per month).

Five Takeaways from “The Everything Budget Book”

Let’s keep the same $5,000 portfolio and $200 per month strategy but extend it over 40 years. Your income portfolio would be over $1 million and pay you at least $100,000 in annual dividends.

The numbers would be even more insane if you increased the size of your options portfolio to $30,000 and made $1,200 monthly. In this case, you would see $6 million after 40 years.

The moral of the story. The story’s moral is that options trading can be quite lucrative over a long career. Most people jump into the program, get themselves burned, and leave with a bad taste in their mouths.

To understand options, you must understand money. Money is an exchange of value; nothing more, nothing less. If you jump into the options market, you’ll lose quite quickly if you are purely trying to make money.

I Love Paying the Bills because I Mastered the Process

Instead, use options as one income-generation tool in your arsenal. The more you try to protect your wealth and build an empire, the better decisions you will make.

In the world of options, there is no amount of money you can’t make. No number is too big. On the flip side, you can lose it all. If you trade on margin, you can lose all your money and someone else’s. There is a lot at stake.

The key is understanding everything about money, business, bonds, and the economy. You can’t simply go into the options market against the market makers, professional traders, and speculators and think you’ll walk away on top.

Financial Freedom is a Mindset, Not an Account Balance

I will recommend some books I wish I had read at age 18 instead of 38.

- “Rich Dad, Poor Dad”

- “Rich Dad’s Cashflow Quadrant”

- “The Bond Book”

- “Covered Calls for Beginners”

- “The Psychology of Money”

Once you get into a rhythm, continue to read about other people’s strategies. Trading options is a highly emotional affair. You must employ tactics that match your personality and demeanor.

Conclusion. I wish I were an options trader in my 20s; however, from 2000 to 2010, the infrastructure wasn’t in place for the average person to access the options market.

As a 43-year-old with a wife and kids, I exercise caution in the options market. I have a $5,000 portfolio that generates some nice, small returns.

The best advice I can give to young people looking to trade options is to have a bigger plan. If you don’t have a reason to trade options except to make fast money, you’ll lose in the long run.

Series “I” Bonds for Life

You need something to keep you grounded in reality—like saving for a down payment. Nobody can predict the stock market. You will lose! Period.

However, if you take your wins early and cut your losses early, you’ll end up on top in the long run. You may want to join an options trading club, but be careful.

Don’t follow the leader just because he is the leader. He may have a different goal than you. He may have $1 million in the bank that he can blow without worry.

You must protect your nest egg at all costs. Taking a risk is necessary to get us where we need to go. However, we can manage the size and depth of this risk.

Earning and compounding a 30% annual return will make you rich. However, greed is the killer of wealth. Learn to control your fear and greed early, and you will be ready to trade options in your 30s. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply