Do you really want to work until you are 65? At some point in my working life, I thought I would have a 30-year military career followed by 20 years in the civilian workforce.

And then I changed my mind. In 2021, I wrote “No Freaking Way I Am Working Another 25 Years.” That was the year I turned 40.

Somewhere along the way, I decided I had had enough—I wanted out. At age 42, I freed myself on the back of my assets. I was now financially independent.

Run a Mentoring Program Toward Passive Income

The power of assets. If you want to retire early, you must own assets; rich people understand this, while the poor may not.

Let’s look at some examples of how powerful assets can become in the right hands. The goal of life is to harness the power of compounding. The more assets you own, the more assets you will have compounding.

The power of real estate. Let’s say your parents gave you a paid-off home when you turned 18. Now, as you progress through life, your home is compounding—the price and rent values increase.

Not only are your real estate holdings compounding, but it is also the money you save by not paying increasing rents. You can save and invest more money as you progress through the corporate ladder and increase your income.

After 40 years of work, you will have enough money to purchase multiple properties. The key to this scenario is obtaining a powerful asset early in life.

The power of investing. Let’s say your parents gave you an income-investing portfolio that pays $2,000 monthly when you turn 18.

Becoming an Entrepreneur #3

As long as you reinvest at least 25%, your portfolio’s output will continue to increase. Eventually, you’ll make enough in dividends to pay for your lifestyle. You will have become financially independent.

The power of creativity. Let’s say your parents gave you the royalty rights to a set of books they had written. You would collect the passive income from these creative works.

As you grow older, you find new ways to get these works in front of a new audience. You can expand their reach, which would expand their income-producing ability.

The power of business. Let’s say your parents gave you a food truck business when you turned 18. It runs itself, and you collect the residual business income.

As you age, you start to expand the business via franchising. You also create valuable content on owning and running a food truck business.

Time is Money #1: Debt

When you turn 40, you sell the food truck business for a few million dollars. You use the money to start another company, invest in dividends, purchase real estate, and create more content. You become a capitalist.

The power of education. When you turn 18, your parents decide to pay for all of your education. Even if you become a doctor or dentist, your parents can afford to cover you.

With no student loan debt, your quality of life can compound rather quickly. You can use the extra cash flow to invest in assets.

Choose Between $100,000 Active versus $50,000 Passive Income

Time to become a capitalist. One common trend in all of these scenarios is that your parents were capitalists. They put themselves in a position to own assets and pass them down.

Most of us don’t have capitalist parents, so we must take the long road to becoming one ourselves. But do you see how powerful owning an asset can be early in life?

A capitalist understands the value of owning assets in the long run. They also understand the difference between an asset and a liability.

Thus, the goal is to become a capitalist and leverage assets to retire early. Can an average person without capitalist parents become a capitalist and retire early? The answer is yes.

My story on becoming a capitalist. I joined the Marine Corps in 1999 because I wanted to live a solid middle-class life. I had no delusions of becoming wealthy and living high on the hog.

Series “I” Bonds vs. Index Funds

However, after 20 years in the military, I couldn’t afford to take my family to Applebee’s without using a credit card. Something had to change.

At the time (in 2019), we owned two assets: a home in Yuma, Arizona, and a home in Pensacola, Florida (our primary residence).

We decided to use our home in Pensacola as an asset and start making money from it. We rented rooms and began to create positive cash flow.

This awakening allowed us to purchase another home in 2020. Today, we own three homes and a tiny house. We were becoming capitalist.

Since 2019, I have also become involved in the stock market. Over the years, I have become a dividend growth and income investor. We now earn $2,000 per month in dividends.

I also write books that generate a small amount of monthly passive income. I am using my GI Bill as an income generator to generate tax-free income that I can invest.

Give Your Kids a Different Path

I became a capitalist and retired early. Don’t get me wrong; I can live my entire life on the income from my military retirement. However, my military retirement is not an asset because I cannot pass it down to my kids.

Therefore, my goal is to obtain assets (buy, create, build) that I can pass on to my kids and grandkids. I want them to begin life with a massive head start toward the power of compounding.

You can also become a capitalist. You must make self-education your top priority. No one book will teach you everything you need to know.

The fact is that we will all gravitate to different aspects of capitalism. Some people prefer business over real estate, and others love creativity over investing.

Quiet Quitting vs. Loud Rehiring

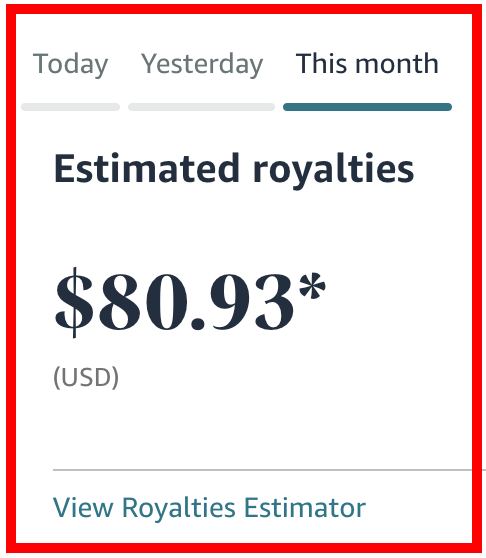

The goal is to have your assets working alongside you 24 hours a day. I can log in to Amazon daily to see how much income my books have produced.

So far this month (July 10th, 2024), my books have produced $80 of passive income. It’s not a lot, but it’s a lot of money when you don’t depend on it.

My books produce roughly $200 per month, my dividends $2,000, and my real estate $700 (after paying mortgages). That’s a nice chunk of change that keeps growing every year.

Outside of income, these assets also grow in value. Real estate prices keep increasing, my stocks rise, and the value of my book business increases with each book I release.

Happy Cash Flow Retirement 9

Set your kids up for success. Wouldn’t it be lovely to have a home when you turn 18? We can all dream, but we can also do this for our kids.

We must focus on obtaining assets for our kids and grandkids, not living a hyper-consumerist lifestyle. Trust me, corporations want you to purchase RVs, boats, and vacations at the expense of owning tangible assets.

Conclusion. You can retire early on the backs of your assets; the key is obtaining assets. You must create assets if you don’t have the money to purchase real estate or dividend-paying stocks.

The Golden Handcuffs of Lifestyle Inflation 2

My favorite author, Robert Kiyosaki, says you can create assets from thin air. We all have experiences that can help someone else.

You can turn those experiences into books, podcasts, or videos. That is the beginning of your business. Your business generates income that you convert into passive income via stocks and real estate.

There is no room for excuses. It’s time to become a capitalist and leverage capital markets (real estate, stocks, bonds, cryptocurrencies) to our benefit. Whatever assets we obtain, we can pass along to our kids—which is the ultimate goal. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply