How much money can you earn in a 30-day cycle? I guess it depends on how you choose to earn your income. You can do it the safe way or add a little spice.

Ultimately, it depends on your objectives. If you want to juice your returns to retire earlier, you’ll have to take on a little more risk.

You also have the safe option of earning high yields from the federal government. The only caveat is that yields come and go, and you may be left earning 1% or less on the bond market.

How to Channel the Velocity of Money

Today, I want to compare two very different financial instruments and strategies. On one hand, we have Treasury Bills (T-Bills) from the federal government. On the other hand, we have selling cash-secured puts on the options market. Let’s begin.

What are Treasury Bills? Treasury Bills are short-term bonds you can purchase directly from the federal government on the Treasurydirect.gov website.

T-Bills have been paying an exceptionally high yield due to the Federal Reserve’s interest rate hiking cycle, which began in 2022.

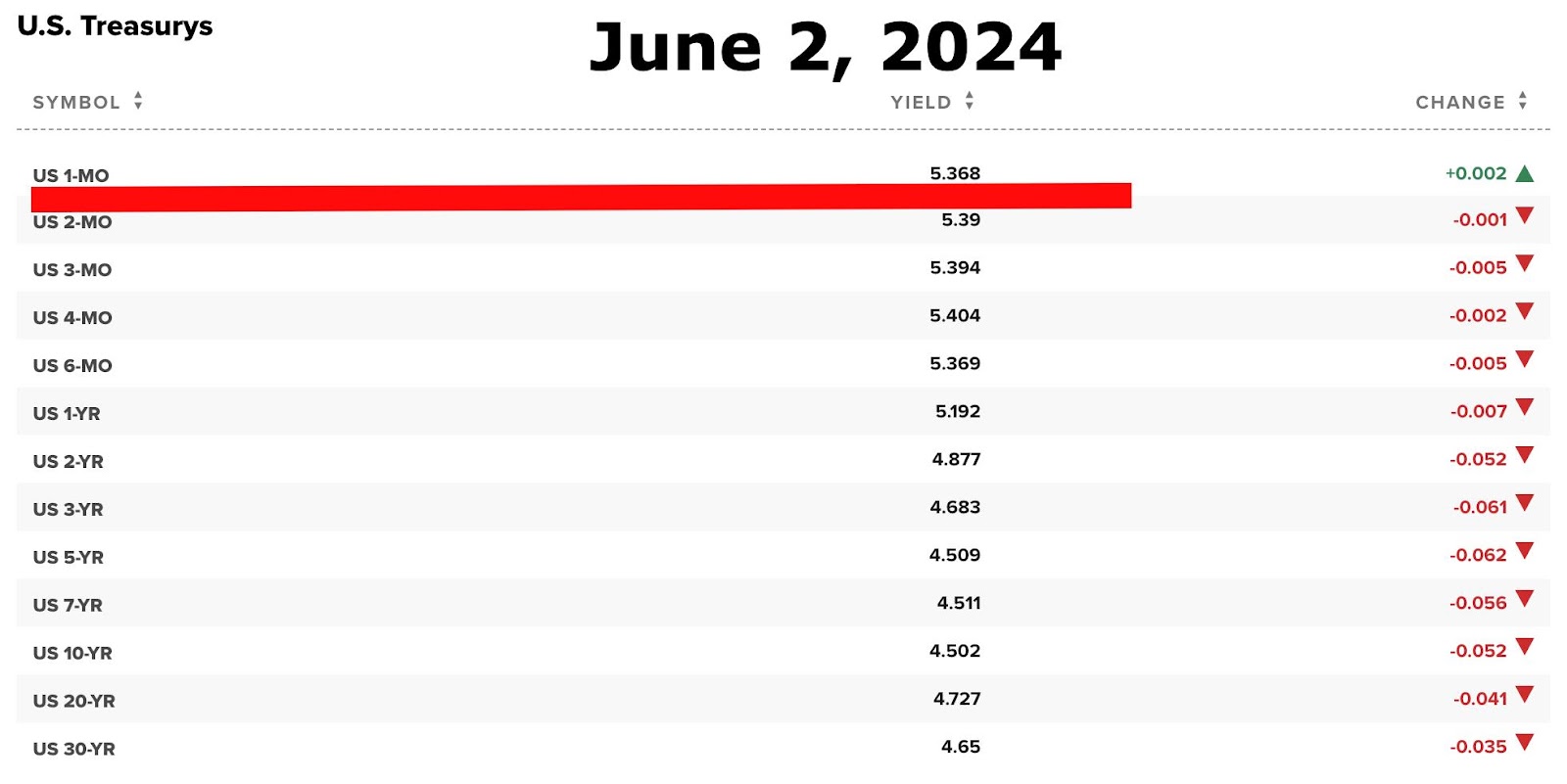

Today (June 2, 2024), one-month (or 4-week) treasury bills pay a whopping 5.368%. This is a fantastic time to “T-Bill & Chill.”

Leaving the Workforce in 10 Years: For Singles

“T-Bill & Chill” is the art of continually rolling your T-Bills over and collecting the high-interest rate income. It is an alternative to investing in a Certificate of Deposit or High-Yield Saving Account.

T-Bills have one massive advantage over CDs and HYSAs: you don’t have to pay state tax on them. Therefore, if you live in a high-state-tax area like California or New York, T-Bills will save you a load of money.

The 4-week T-Bill also has the shortest duration risk, meaning you can pivot your money quickly if the market changes.

What are Cash-Secured Puts? On the opposite end of the risk spectrum are cash-secured puts. Selling cash-secured puts means you are selling someone the option to sell you their stocks if the share price decreases.

You can sell puts on a weekly basis, but I find that the monthly option gives the highest reward with the amount of risk you take.

To sell one cash-secured put, you must have the cash to purchase 100 shares of the underlying stock if the share price declines below the strike price.

What I Have Learned from Having Tenants for 10 Years

For example, let’s say Rivian’s (RIVN) current share price is $10.35. I can sell one cash-secured put at the strike price of $9.00.

I need $900 ($9.00 x 100 shares) on hand to sell this put. If the share price decreases to $8.99 or below, the buyer could sell me their shares for $9.00.

For my trouble, the buyer would pay me a premium. In this case, let’s say they gave me $25. The goal is to never get assigned shares and keep collecting the monthly premiums with the same cash on hand.

What’s the return on cash-secured puts? It’s easy to see the yield on Treasury Bills; however, you’ll need to do some math to conduct a fair comparison with selling puts.

Life is a Math Game

You always want to compare the annual rates of your investments. We know the annual rate of the T-Bill is 5.368%, even though we only get one month of income at a time. Over the 12-month cycle, this rate will change continually.

The same is true for cash-secured puts. You won’t always get the same $25 premium, and the share price won’t always be $9.00

But let’s assume we receive $25 per trade at a $9.00 share price. The annual premiums we collect would be $300. We would divide $300 into $900 to get the annual rate.

That gives us a whopping 33.33% annual return! Is this too good to be true? No, not really. You can make these fantastic returns and more, but you must accept risk.

Risk versus risk-free return. Investors consider US treasuries risk-free investments. This means that if you put your money in and hold until maturity, you will get your money back plus interest.

Your Income Should Increase Every Year 2

The entire world assumes that the US treasury is risk-free, so every other financial product compares itself to it.

If I can get a 30-year US Treasury Bond at 5%, I would consider that before purchasing a rental property that will generate 4% returns.

Dividend stocks also fluctuate based on the current treasury rates. Don’t underestimate the power of receiving a safe 5% interest rate for doing nothing.

On the other hand, options trading can be pretty risky. The most dangerous part of trading options is ourselves; our brains have a “fear and greed” meter.

I’m High on Life with Royalties

If we cannot control our emotions, we will lose big in the options market. Regarding selling cash-secured puts, the most considerable risk is collecting the largest premiums.

When you sell a cash-secured put, the largest premiums come from the strike prices closest to the current share price.

For example, if the current share price is $10.35, you’ll get the highest premium if you set the strike price at $10.00. You may collect a $55 premium.

However, if you set the strike price at $9.00, you may collect a $25 premium. What happens if you assume shares at the $10 price?

Chances are that if you assume shares at the $10 price, the share price is already below that value, perhaps $9.20.

The Magic of Passive Income Investing 2

Now, you would need to sell covered calls from a position of weakness. However, if you set the strike price of your put lower, you’ll be in a much better position.

If everything fails, you can assume the shares at a low price and wait until your position improves. Remember, it will be easy to beat the returns of treasury bills using cash-secured puts, so there is no need to get greedy. You’ll need to sit and wait for the stock price to recover; it’s no big deal.

Passive income in retirement. You will need to utilize both strategies if you plan to retire early. Yes, T-Bill yields are impressive now, but they have been garbage for over 13 years (2008-2021). If the Federal Reserve drops rates back down to 1-2%, you’ll need other methods to collect yields.

As rates drop, more people will pile into higher-yielding securities such as dividend stocks, closed-end funds, business development companies, and Real Estate Investment Trusts.

Scarcity vs. Abundance

As yield-hungry investors pile into these higher-yielding products, their prices will shoot up, decreasing the yields.

The sexy Mortgage REIT AGNC (AGNC), which currently yields 14%, may drop to 10%. The amazing business development company Ares Capital (ARCC) will theoretically go from 10% to 7%.

You will lose your ability to T-Bill & Chill with any kind of success. Yes, it’ll be an excellent way to maximize the returns of your emergency fund, but that’s about it.

The Magic of Income Investing 2

Conclusion. You’ll need to generate over 10% returns to beat inflation and price hikes consistently. With the right mindset and emotional outlook, you can do this by selling cash-secured puts.

I would love to T-Bill & Chill for the rest of my life, but that is not how this will play out. At some point, the rates will decrease. The Fed cannot afford to pay high-interest payments on these bonds forever.

When rates come down, inflation may still be high. Even if inflation lowers, companies and governments will still be greedy. Prices around you will continue to increase.

You’ll need to generate at least 10% returns. Use your treasury bill strategy as a safe haven, but don’t stay there forever. You’ll need to use a small portion of your portfolio to generate high returns and stay ahead of inflation. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply