I love comparing various financial products against one another, but this one will take the cake. How do you compare the safest option to the riskiest one?

So, let’s simplify the comparison: How would I safely grow a small nest egg of $1,100?

The easy answer is to put the money into a high-yield savings account and let it compound at 4% indefinitely. Today, I want to explore another option—selling covered calls.

Saving is Defense; Investing is Offense

What is a high-yield savings account? A high-yield savings account (HYSA) is a savings account that pays considerably more interest than a standard savings account.

For the most part, online banks offer the highest yields on these accounts because they do not have to support physical brick-and-mortar stores.

Interest rates on HYSA have been high lately because the Federal Reserve has raised interest rates to 5%. This means that HYSAs are paying roughly 4.5%.

If I invested $1,100 for 30 years at 4.5%, I would end up with a total of $4,120. However, there is a massive hole in this theory. Chances are the Federal Reserve will not hold rates this high for 30 months, let alone 30 years.

What are covered calls? Selling covered calls is a way to leverage shares you own of a company to make additional capital.

What is Your Relationship with Money?

Say I own 100 shares of Rivian (RIVN). I can sell someone the right to purchase these shares from me if the stock price meets certain conditions. For my pain, the buyer would pay me a premium.

I collect the premium whether the buyer takes my shares or not. The goal of selling covered calls is to collect my premium while keeping my shares—then repeating the process. Leveraging options (calls, puts) is much easier when we remove “personal greed” from the equation.

Selling covered calls vs. high-yield savings. I know this is a strange comparison, but hear me out. We know that high-yield savings accounts offer 4.5% yields in today’s market.

By adding a small amount of risk, we can safely grow our $1,100 options trading portfolio much faster.

The key to earning safe returns from selling covered calls is comparing your returns to the 4.5% HYSAs. Too often in options trading, we want to earn the highest yields by assuming the highest risk.

The Metaverse 117: Return to the Metaverse

The first step in comparing covered calls and HYSAs is determining how much we would make annually with a HYSA. At a 4.5% rate, we earn about $50 in interest annually.

Therefore, to successfully implement a covered call strategy, we would need to beat $50 a year; this would be the goal of our covered call portfolio.

Purchasing stocks and selling covered calls. I picked the $1,100 amount because I can buy 100 shares of my favorite stock for $1,035.

Currently, Rivian (RIVN) is selling for $10.35. I can purchase 100 shares for $1,035. Buying stocks is easy; now it is time to sell our covered calls.

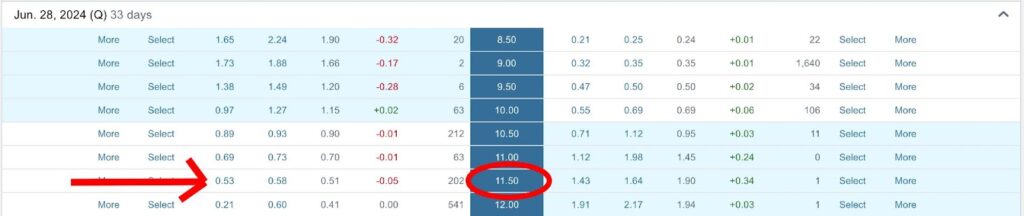

Looking at the “options chain” chart above, we can see that we can sell at the strike price of $11.50 for $0.53 each. That would net us a premium of $53 ($0.53 x 100) minus the broker fee.

Why did I choose the strike price of $11.50? I would have made much more money at the $10.50 strike price ($0.89 vs. $0.53). However, the chances of my shares being called away are much greater.

What is Your Risk Tolerance?

Let’s examine what happens if the share price goes to $12.00 when my strike price is set at $11.50. First, I collect the $53 premium.

The buyer collects my shares and pays me $11.50 each. Remember, I paid $10.35 per share, which means I will also collect a profit of $115.

I walked away with $168 ($115 profit + $53 premium) on an investment of $1,035, which would give me a 194% annual return.

Forming a safe strategy. As you can see, we made more with covered calls than in an entire year with a high-yield savings account.

The goal is to keep building safe, dependable passive income streams. The trick to earning good returns with covered calls is focusing on the cost basis.

Saving & Investing with $1,000 per Month

If the cost basis of your 100 shares is $10.35 per share, you must ensure that you set your strike price higher.

There will come a time when your cost basis is higher than the current price. For example, the current price may be $9.00, and your cost basis is $10.35.

In this case, you can sell a covered call at the strike price of $11.00; however, your premium will be low. Or you can wait it out and hope the price increases over the next few months.

Don’t put yourself in a situation where the buyer can take your shares away, and you will lose money on the sale. I have done this, and it’s not fun.

Rents Go Up: Which Side of the Equation Are You On?

The magic of HYSAs. The magic of high-yield savings accounts is that you can put your money away and forget about it. You don’t need to do any work to maintain your interest income.

However, what happens when interest rates come down? I remember that in 2020, I received 0.40% on my HYSA.

That’s why learning how to leverage covered calls is essential to earn additional income. Even if you only sell two or three covered calls per year, you could make 4 to 8 times more interest income than with a HYSA.

When you finish trading covered calls, you can put the entire pot of money in your HYSA and relax for the rest of the year.

How to Use a Daily Budget

Imagine making $200 on one covered call and putting $1235 into your HYSA to earn 4.5%. Very few people on earth can exercise this kind of financial discipline.

Conclusion. Using both HYSAs and covered calls is the ideal way to earn a safe return. You don’t want to keep risking your money in the options market.

You’ll want to withdraw your money from the “casino” and let it grow safely and organically. However, it’s also a good idea to learn the ropes of covered calls.

Interest rates are not guaranteed. We may enter another 10+ years with zero interest rates where your money earns no money.

In cases like this, we must force our interest income by leveraging covered calls. The most challenging part of trading options is controlling your emotions.

Personal Loans vs. Credit Cards

The first question you must ask yourself is how much money you would make annually in a HYSA. You’ll probably make more money in one trade than an entire year.

Always avoid this perspective: The main appeal of the options market (for most people) is the ability to double your money in one trade.

However, you’ll take on an extreme amount of risk. The better way is to earn 5-10% of your money per trade. You will exceed a savings account’s annual interest payments in several trades.

Once you have made more than enough for the year, put the money into an HYSA and enjoy the compounding interest safely. Very few people have the emotional and financial discipline to pull this off. Do you? Good Luck.

- PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 4! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 12 (Free 460-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply