Many young investors get burned by trying to double or triple their money in a few months. Because of these unrealistic expectations, they chase bad cryptocurrencies, meme stocks, and shady real estate deals.

These investors aren’t bad; they probably don’t know how to define their risk profile. Understanding how bonds work is essential to becoming a successful investor. You should compare every investment to the risk-free returns of US Treasuries. Let’s begin.

What is the rate of return? Every investor should focus on the rate of return on their investment. The rate of return is how much money you will receive on top of your initial investment. You can see this expressed as “interest rate,” “return on investment,” “internal rate of return,” “cash-on-cash return,” or something similar.

The Importance of Index Funds to Your Portfolio

Luckily, the Federal Reserve sets the cost of money at the federal level, so you always know what the government is paying for capital.

Learning the current Federal Funds Rate (FFR) is crucial to making important investment decisions. Once we understand the FFR, we can look at US Treasuries to get an idea of the investing landscape.

The importance of US Treasuries. The government sells US Treasuries based on the current FFR. However, these are marketable securities, meaning their interest rates will vary based on market conditions versus the FFR.

This means that the US government sets the coupon rate on the Treasuries, but investors may pay a price more or less than the value of the bond. Does it sound confusing?

Military Success 104: Family Fitness

I like to compare bonds to gift cards. Let’s say Walmart offers a gift card for $100, but you can buy the gift card for $93 based on market conditions. However, you can still redeem the gift card for $100.

With Treasuries (and all bonds), the issuer sets the terms and sells the bonds on the market. Bond investors will adjust the price of the bonds to match current market conditions.

With Treasuries, investors adjust bond prices to match future inflation expectations, current inflation rates, and if they believe interest rates will be higher or lower in the future.

Retire Rich, Retire Comfortable with a Business

The bond market is very smart and far less emotional than the stock market. Understanding how the bond market fluctuates is vital to making great investment decisions throughout your lifetime.

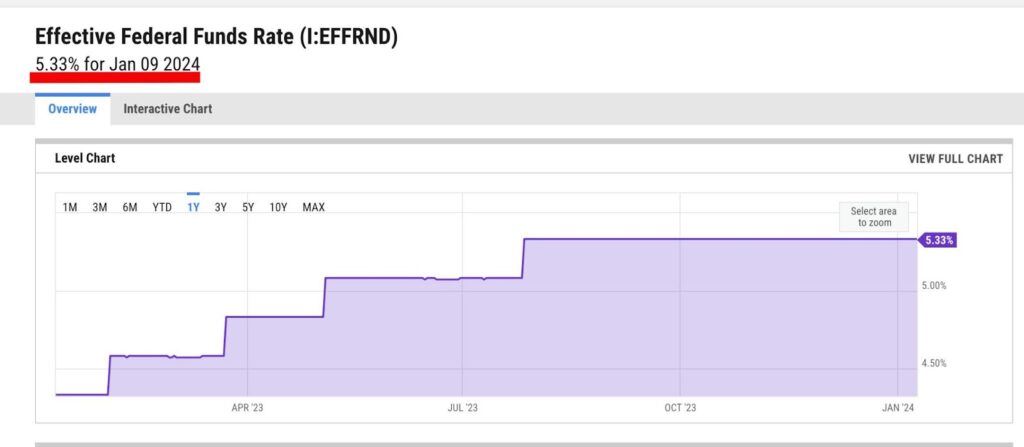

Let’s look at Treasury rates today based on a Federal Funds Rate of 5.33%. As you can see, the various US Treasuries adjust to today’s FFR versus future expectations.

How to define risk. Investors consider US Treasuries risk-free assets. As long as you hold your bonds to maturity, you are guaranteed to get your money back.

Creative Finances in Real Estate 103: Home Equity

Nothing in life is guaranteed; however, if you fear losing money with Treasuries, you probably should not be investing at all. If US treasuries fail, we will have much bigger problems in the world to consider.

The Treasury Department divides US Treasuries into multiple types that can fit your investing needs. Each kind of treasury has similar investments you can consider in the civilian world.

- Treasury Bills: 1 to 52 Months

- Treasury Notes: 2-10 Years

- Treasury Bonds: 20 and 30 Years

- Treasury Inflation-Protected Securities (TIPS)

- Series “I” Savings Bonds

- Series “EE” Savings Bonds

Once you understand how Treasuries work, you can start defining risk. Remember, Treasuries are considered risk-free as long as you hold to maturity.

If you attempt to sell your Treasuries before they mature, you are at the whims of the current market conditions.

Let’s say you have a 10-year Treasury Note with a 4% coupon, and the FFR is currently 2%; you can sell your bond for a higher price. This is because the price will adjust to match current interest rates.

Five Benefits of Options Trading

Conversely, if you have the same bond but current rates are 6%, the price will decrease to increase the yield. Remember, the analog of the gift cards. Prices and yield move in opposite directions.

Building a risk profile. Now, we can start to define our risk based on what we know. The current FFR is 5.33%, and inflation is around 3.1%.

One of the most significant risks to your future money is inflation. If you stuff your money in a mattress, you will slowly lose purchasing power.

Right now, all the US Treasuries will beat inflation. However, how long will the Fed keep the FFR this much higher than inflation?

Should You Consolidate Debt?

What is your investing time horizon? Will you retire soon, or are you saving for a house? Knowing what we know now, we can look at products outside of Treasuries to see how they compare.

High-Yield Savings Accounts. High-Yield Savings Accounts (HYSAs) are an excellent way to get results similar to short-term Treasury Bills.

However, as soon as the FFR decreases, your HYSAs will quickly lower their rates to match. I watched the interest rate on my HYSA slip from 2.0% to 0.4% in 2020.

Therefore, the risk of HYSAs is that they will produce different long-term results than a five or 10-year Treasury Note. However, you balance that risk with the ability to withdraw money in minutes.

Certificates of Deposit. The federal government insures your Certificates of Deposit (CDs) up to $250,000. However, you’ll receive the best rates up to 9 or 12 months.

The Truth About Discretionary Income

As you review long-term CDs, the rates will decrease because the bank is taking a considerable risk that interest rates may adjust over 2-5 years.

Also, the federal and local governments require you to pay tax on interest from CDs. States cannot tax interest from US treasuries, which is something to consider if you live in states like California or New York.

Other bonds. There are many different types of bonds, including mortgage-backed securities, municipal bonds, corporate bonds, and high-risk corporate bonds (junk bonds).

These bonds pay higher coupons than Treasuries, but you assume more risk. You can leverage knowledge of various markets to get a higher yield outside Treasuries. The danger is that your gamble doesn’t pay off as you intend.

Advertising 103: Maslow’s Hierarchy of Needs

For example, mortgage-backed securities currently pay 6 to 7% because of high mortgage rates. We all assume mortgage rates will decrease through 2024 and 2025, making your 7% yielding portfolio increase in price.

But what if rates shoot to 10% because of some unforeseen calamity? The value of your MBS will decrease to match current rates.

The government and investors adjust prices and yields on US Treasuries based on the FFR and inflation expectations. Other bonds adjust against US Treasuries AND their specific locality risk (municipal bonds), housing (mortgages), and business outlooks (corporate bonds).

You can’t accept the higher yield without understanding the new underlying risks. That’s why understanding bonds is vital to everything we do, including stocks.

Passive Income in CryptoCurrency

Conclusion. I will need to write a follow-up article covering stocks, fixed-income, options trading, real estate, business, and cryptocurrencies.

Hopefully, you are starting to understand how everything in investing begins with risk-free Treasuries. Once you determine the Treasury rates, you can input your own investment profile.

If you are near retirement, you may want to avoid investing in stocks. The 5% coupon on treasuries may be ideal for your situation.

Become a Real Estate Investor/Agent

If you need the money in one year, you may consider an HYSA versus investing in a 52-week Treasury bill.

You may have $10,000 in your HYSA and convert $5,000 to a certificate of deposit because of the ease of keeping it in the same bank.

There is no wrong option, but we must always consider what someone will pay us for our money without risk.

Sometimes, taking an unnecessary risk is the risk. Other times, taking no risk is the risk. As investors, we need to determine the best bet for our future. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply