We all must position our money to beat inflation. We can do this by investing in dividends, real estate, royalties, and businesses.

Once we start earning additional cash, we must invest it into securities that also attempt to beat inflation.

Two safe government-sponsored inflation-beating products are Series “I” Bonds and Treasury Inflation-Protected Securities (TIPS).

Financial Freedom is a Mindset, Not an Account Balance

Welcome back to the Investing for Interest series (101, 102, 103, 104, 105, 106, 107, 108, 109, 110, 111, 112, 113, 114, 115), where inflation doesn’t stand a chance against our investing prowess.

Starting from the top: Series “I” Bonds. Series “I” Bonds are saving bonds you can purchase directly from the US Government on the TreasuryDirect.gov website.

You can purchase up to $10,000 per year per social security number. Series “I” Bonds have two interest rate numbers that make their composite interest rate.

There is a permanent interest rate (usually small) and an inflation interest rate which adjusts every six months.

I Love Paying Bills Because I Mastered the Process

As your savings bonds accrual interest, the principal will begin to grow. Your interest payments will become larger (but stay inside the bond). You don’t pay taxes on the accrued interest and capital gains until the bond matures or you redeem the security.

Starting from the top: Treasury Inflation-Protected Securities: Treasury Inflation-Protected Securities (TIPS) are marketable securities the US Government provides at auction.

As an individual, you enter a non-competitive bid when you purchase TIPS. This simply means you will buy them at the market rate for that date.

If you want a $1,000 TIPS, it may cost you $1,005 or $990, etc. The government sets the interest rate (coupon) on your TIPS before the auction.

Five Takeaways from “The Everything Budgeting Book”

However, your principal will continue to adjust and grow along with the inflation numbers. Your interest payments will grow as your principal increases.

For example, your $1,000 TIPS may have a 2% interest rate. In 10 years, the principal increases to $1,200, and your payments go from $20/year to $24.

You will pay taxes on the interest payments and capital gains from the increases in principal. However, the principal gains will not be income—you’re paying taxes on income you didn’t receive (called phantom income).

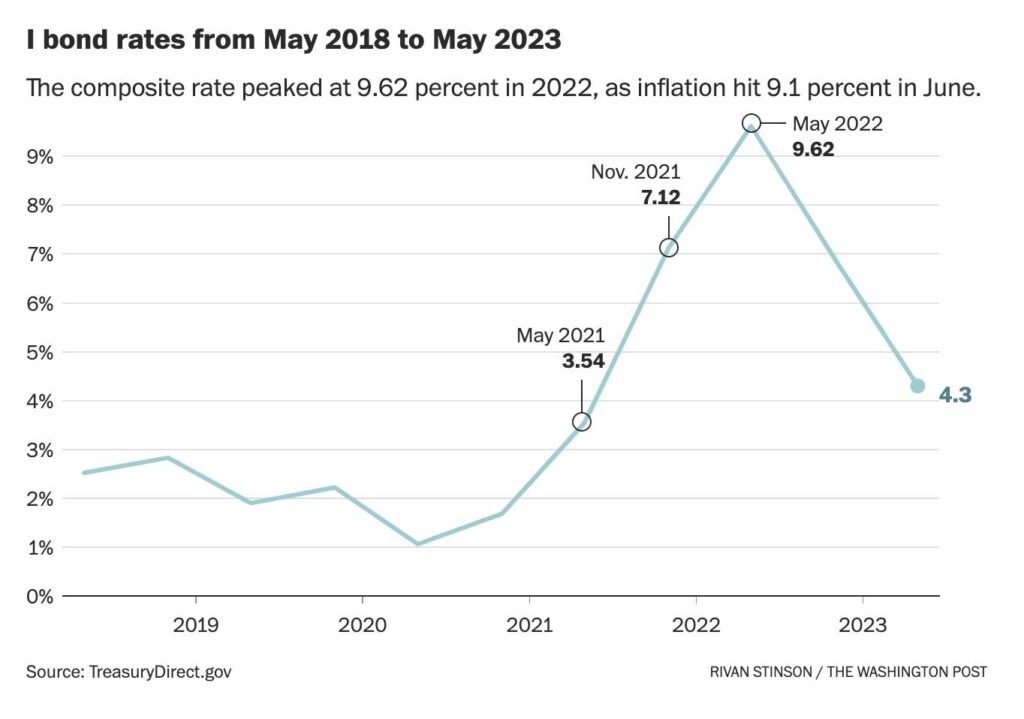

Which bond is right for you? Series “I” Bonds can be powerful allies if inflation spikes quickly. We saw this in May 2022, when Series “I” Bonds interest rates increased to 9.62%.

Annuities vs. Income Investing

However, for the most part, Series “I” Bonds rates are relatively tame. As soon as the Federal Funds Rate increases to beat inflation, Series “I” Bonds lose their luster.

Series “I” Bonds are straightforward instruments for you to purchase. You can buy them in a denomination of as little as $25—down to the penny (i.e., $25.36).

You can also purchase them any time of the month, as there is no auction. The main limiting factor is the $10,000 annual limit (you can add $5,000/year from tax returns).

Big investors need TIPS. TIPS have no annual limit, instantly making them the better choice for big investors.

Becoming an Entrepreneur #2: Dropping the 9-5 Mindset

You can also purchase them in 5, 10, or 30-year maturities. Series “I” Bonds are always for 30 years; however, the penalty for early withdrawal is low.

Series “I” Bonds make great gifts because the owner will not need to pay taxes until maturity. They are also tax-free if the owner uses them for educational purposes.

If you need income throughout the holding period, TIPS are your only option. If you invest $10,000 annually in TIPS and Series “I” Bonds, your TIPS will pay you semi-annually directly to your account.

Series “I” Bonds are more of a savings account you can’t touch for 30 years (unless needed). Your money is far away—doing great things for you.

The Leveraged Millionaire

Series “I” Bonds will make a great addition to your high-yield emergency fund. I wouldn’t recommend putting TIPS into an emergency fund because selling them is complicated.

What is your tax situation? Taxes are a big component of decisions investors make. You can invest in TIPS in a tax-sheltered vehicle like Roth IRAs.

The interest on TIPS and Series “I” Bonds is exempt from state taxes, making them great for high earners living in California or New York.

Series “I” Bonds are outstanding for tax purposes because you can redeem them individually. You’ll see how much income you will generate when you redeem them.

The Golden Handcuffs of Lifestyle Inflation 2

Redeeming your bonds. Series “I” Bonds are effortless to redeem. You select the security and the bank account you want the government to deposit the money.

You must sell your TIPS on the open bond market. You can do this through the TreasuryDirect website or your broker.

However, pricing your TIPS is highly complex. Although you have a $1,000 TIPS, it could have accrued principal.

The bond market is pretty straightforward for regular bonds. If your interest rate is better than current rates, your bond’s price is usually higher.

Happy Cash Flow Retirement 9

TIPS have the added inflation element, which sometimes goes against conventional bond wisdom. Expected inflation predictions (not current rates) play into the pricing of your TIPS on the open market.

All of this is to say that buying and holding your TIPS until maturity is the best way to navigate this complex security.

If you need your money before the bond’s duration, you may be better off purchasing a high-yield savings account, Series “I” Bonds, Certificates of Deposits, a Money Market account, or a TIPS bond fund on the stock market.

Ultimately, you can narrow your situation down to a few questions.

- When do you need your money?

- What is your tax situation?

- Do you have more than $10,000 to invest?

- Are you purchasing them for someone else?

Conclusion. Series “I” Bonds are the simpler of the two securities. However, as an investor, you don’t want to limit yourself to what is easy.

Quiet Quitting vs. Loud Rehiring

The world runs on income, and TIPS provide your inflation-adjusted return from 5-30 years. One $1,000 TIPS may provide a little income, but $1 million would be nice.

I’m a hardcore income investor, so I don’t dabble with much money in Treasuries. But I also have a secure military pension.

If I didn’t have a pension, I would need to relocate a lot of my wealth into safer securities like TIPS and Series “I” Bonds.

Give Your Kids a Different Path

My rule of thumb would be to max out my Series “I” Bonds for the year and then start buying TIPS.

However, I also love the 30-year Treasury Bonds over 4%. At 4%, I would beat inflation for the majority of the 30 years(just my opinion).

Don’t dismiss TIPS because of their complexity. We must at least understand all the tools at our disposal. I love Series “I” Bonds and am starting to understand TIPS. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 11 (Free 410-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply