Investing in bonds was nearly impossible for 15 years (2008-2022). The Federal Reserve kept interest rates low to spur the economy meaning bond yields were abysmal (1-2%).

However, the Federal Funds Rate is above 5% currently, and bonds are back to being a good source of safe yields. Now we must decide the best ways to employ bonds in our portfolios.

Welcome back to the Investing for Interest series (101, 102, 103, 104, 105, 106, 107, 108, 109, 110, 111, 112, 113), where we find the best bonds for the future and beyond.

Dividend Investing in Your 70s

Why Treasury Bonds? Treasury Bonds offer the safest yields in the entire world because the US government guarantees them.

If you are looking for safe returns, look no further than US Treasury Bonds. They also come in various durations, from 4 weeks to 30 years.

You can create Treasury Bond ladders to protect yourself from sharp changes in interest rates. Your ladder can have different durations (say 1-year, 5-year, 10-year) and yields (5-year at 4%, 5-year at 4.5%).

You can purchase your Treasury Bonds directly from the US Government at TreasuryDirect.gov. You can also go through a brokerage, which may make it easier.

Don’t Gamble with Retirement 8

Why Treasury Bond Funds? The entire world invests in US Treasuries, giving us a wide selection of options to fit into our portfolio.

Treasury Bond Funds usually differentiate themselves by duration. My favorite Bond funds are Vanguard Long-Term Bond Fund (BLV) and iShares 20+ Treasury ETF (TLT).

I love long-term bonds because I like to lock in great rates and not have to re-address them for a long time. However, many investors like shorter duration bonds like 3-Month (TBIL), 1-3 Years (VGSH), or 5-Year (UFIV).

You can find exactly which Treasury Bonds you want via the stock market. But why would you invest in a Treasury Bond fund over individual Treasury Bonds?

What is Quiet Quitting?

Most bond funds pay monthly. One of the best things about treasury bond funds is that they pay monthly.

Monthly paying securities give you a huge advantage as you progress into retirement. Your bills arrive every month, so having a monthly paying fund will help you address your expenses efficiently.

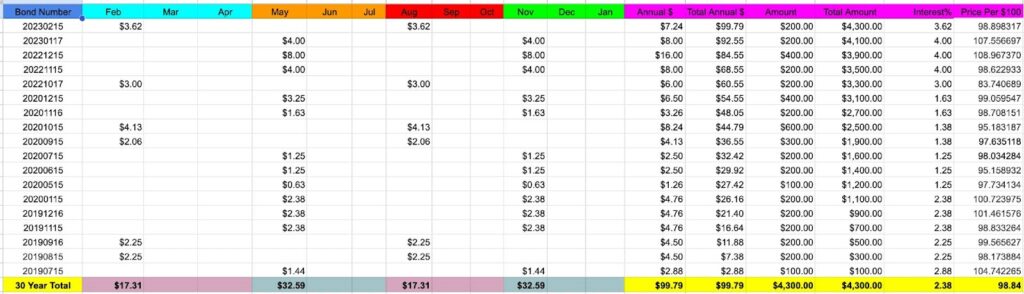

Individual Treasury Bonds pay semi-annually. If you dollar-cost average into Treasury Bonds over a year, you will end up receiving payments in February, May, August, and November.

You’ll want to keep a tracking system for your individual Treasury Bonds, or you will lose track of upcoming payments.

The Magic of High-Yield Bond Reinvestment

The TreasuryDirect website does a great job of keeping up with your bonds individually. However, you’ll become overwhelmed once you get past 20 of these bond issues.

I have a bond tracker I have used for over four years. It may be difficult to understand without accessing the TreasuryDirect website’s individual bond data.

How about taxes? The IRS taxes interest payments and non-qualified dividends at your effective tax rate—so it’s ordinary income.

However, individual bonds have one significant tax advantage over bond funds—they are not taxed at the state level. This can be a major win for high-state tax areas like California and New York.

Love Calls: Survive in a Long-Distance Relationship

In general, Treasury Bond funds produce non-qualified dividends instead of interest. They create business income as a result of handling bonds.

Therefore, your state may tax you on these proceeds. Do your research and also look into municipal bond funds for their tax advantages.

The bond market versus the stock market. The bond market is less volatile than the stock market. The bond market has been crazy over the last year because of swiftly rising rates.

Investing in individual bonds carry no risk—as long as you hold them until maturity. If you decide to sell them early, you can lose (or gain) money depending on current rates.

Five Takeaways from “HSA Owner’s Manual”

The stock market is much more emotional than the bond market. Your Treasury Bond funds can suffer from massive sell-offs, recessions, and bad economic news.

Let’s say I had $10,000 I needed to access in one year. I would put it into a 1-Year Treasury Bill instead of VGSH. The US government guarantees interest payments and principal on your 1-Year Treasury Bill.

The Treasury Bond fund has no guarantee to return your principal. So, what are the best scenarios for using a bond fund?

Why use a bond fund? Bond funds can be a great alternative if you don’t like to track down individual bonds.

Fruits of the DGI Tree

It is effortless to dollar-cost average into bond funds on platforms like SoFi, Cash App, and STASH.

It is easy to see the value of your bond funds at any time. Individual bonds are always the same value until you attempt to sell them.

Once you look to sell, many factors determine their value on the open market, including coupons, yields, and duration. Read “The Bond Book” for more on selling marketable securities (bonds).

Treasury Bond funds are also great for Roth IRAs and other tax-advantaged funds like Health-Savings Accounts and 529s Savings plans.

Passive Income Road Trip #6: Royalties

When to use individual bonds. Individual bonds are outstanding for your Tier 2 and Tier 3 emergency funds. I would keep at least 3-6 months of savings in my high-yield savings account and certificates of deposit.

However, once you get past that amount, you’ll need to earn a decent yield on your savings. Individual Treasury Bonds can be a great place to store 1-2 years of protection.

The idea is that bond values rise when stocks fall. Ideally, the Federal Reserve lowers rates during a recession, increasing the value of your Treasury Bonds.

Coaching in the Metaverse

Let’s say you have 5-year Bonds at 4.5%. If the Federal Reserve lowers rates to 2%, your bond price will increase.

Again, that’s the theory, but anything can happen. However, if you use bond ladders and follow the markets, you can do pretty well with Treasury Bonds.

Conclusion. I combine individual Treasury Bonds and Treasury Bond funds across my portfolios.

Being Broke Isn’t CutePart III: Becoming Debt-Free

I love having monthly paying bond funds in my accounts. I also love knowing that I have some Treasury Bonds not trading on the stock market.

The central concept is understanding how to leverage both options to create consistent income and stability.

Your bond funds can perform poorly in a rising-rate environment, so knowing when to purchase these is essential.

In general, it’s best to purchase bonds when yields are high. However, sometimes you may not get that chance (2008-2022), so learn how to overcome this adversity (dividend stocks, bond closed-end funds).

Stocks and bonds go great together; however, you must leverage the best bond products for today and tomorrow. It’s hard to go wrong with Treasuries if you understand them. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply