I hate credit cards with a passion, although I’ll admit they are a necessary evil. There are just too many random events that can occur, especially when you have a family.

Personal loans are a much better option than credit cards, but they require you to keep a tight handle on your spending.

Most of us cannot control our spending when we are younger. As we age, we appreciate the value of keeping our debt low.

Hustle in Your 20s and 30s, Enjoy Your 40s and 50s

Today, I want to look at how to leverage credit cards and personal loans at various times in your life. I also throw in my experiences with both of these debt vehicles.

Your introduction to credit card debt. Most of us didn’t plan to get into credit card debt. We didn’t wake up and say, “Man, I wish I had $20,000 in credit card debt.”

However, once you leave your parent’s house and get a job, you are officially an in-debt-ured servant. We simply did not have the financial tools and fiscal control to turn the tides in our favor.

Credit card debt is more of a mindset than a number. No one taught us to live below our means because only you can decide your lifestyle choices.

Strong Finances, Strong Marriage

Your parents may value nice cars at the expense of a smaller house. You may love jewelry over going to fancy restaurants.

My spending vice was always cutting-edge technology and video games. However, I never wanted an expensive car or fancy clothes—it balanced pretty well.

We get into credit card debt when we take on too many “spending vices.” You may want a nice car, designer clothes, and top-level dining. This will put you into debt quickly.

Controlling your spending. Controlling your spending is the first step to getting out of credit card debt.

Five Takeaways from “Creating Income Streams”

My wife and I never overspent on items and trinkets. We didn’t buy top-level cars or go on outrageous vacations. But, somehow, we ended up with $50,000 in credit card debt.

What was the culprit? Our first house was too expensive, straining other parts of our lifestyle.

You must get yourself on a hardcore budget to begin controlling your spending. Credit cards are dangerous because you can make split-second spending decisions with long-term consequences.

I recommend getting on a daily spending budget. For example, give yourself $500 per month for personal spending—$16 per day.

Live and die by this daily budget. If you love morning coffee, dedicate $8 per day to it. If you want to buy three $60 video games per month, you’ll have to adjust other parts of your lifestyle.

Run a Profitable Dog Park… On Your Property

Once I put myself on a daily budget, I empowered myself to control my finances. Again, the root of all our financial problems stems from our spending habits.

Transitioning to personal loans. You can transition your credit cards to personal loans after three to four months of not using cards.

It is vital that you control your spending before you consolidate your debt into personal loans. If you can’t control your spending, you’ll end up doubling your debt load.

The value of personal loans. Personal loans are much better than credit cards because they have a verified end date—even if it is five years away.

Should You Buy Property in a Small City?

Once my wife and I controlled our credit card spending, we transitioned to three personal loans. We knew that, at the latest, we would be debt-free in five years.

We then tackled each personal loan, starting with the smallest. This is the debt snowball method, and it works by building your financial confidence.

What happens when you become debt-free? With dedicated focus, you can become debt-free in less than four years.

However, building a large emergency fund can be challenging. Life tends to catch you with your pants down, so you must have a plan.

Look at your budget while you are debt-free. How much did you use to pay toward debt? Let’s say you were putting $1,000 per month toward debt.

No Freakin’ Way I Am Working Another 25 Years

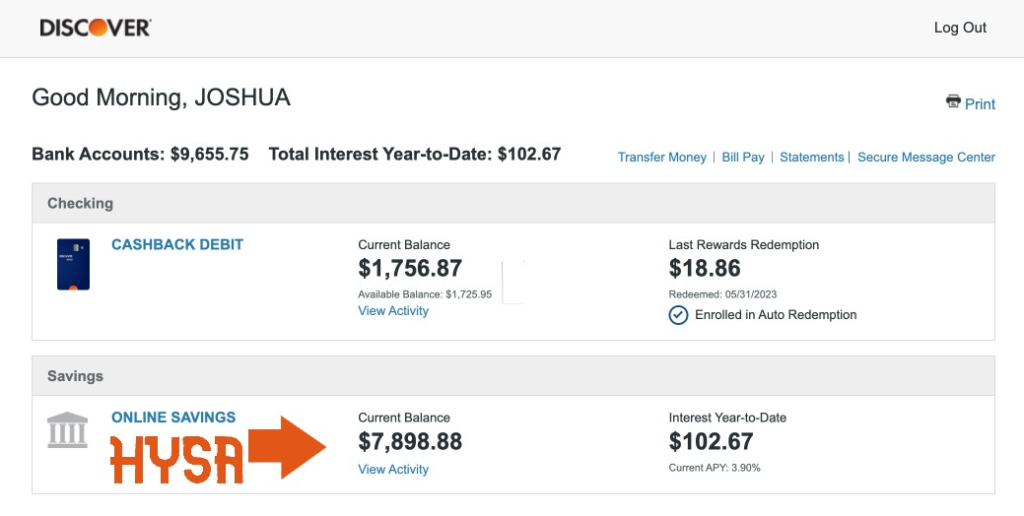

I would take out a $10,000 personal loan that cost me $300 monthly over three years. I would put this $10,000 into a high-yield savings account (HYSA) that paid me 3-4% interest.

Why take out a personal loan when you are debt-free? I am going against Dave Ramsey’s advice, but I am a realist.

Trying to save $10,000 will be a massive undertaking for most Americans. I would rather take out the loan and work as hard as possible to pay it back quickly.

Understanding your personal financial psychology. Everyone is different, and we view money through a different lens.

Do I Need Lots of Money to Start Investing?

I still use my credit card in emergencies because I hate credit card debt. I have $8,000 in my emergency fund currently.

However, if I use my HYSA to cover emergencies, I am not motivated to repay it with any sort of timeline. When I have credit card debt, I want it off the books as fast as possible.

So, I play into my strengths and weaknesses; you must understand how you view money.

If you can save $10,000 quickly, go without a personal loan. If you think taking a personal loan will motivate you to repay the loan with a burning passion, go that route.

Good Debt vs. Bad Debt

Don’t leave it to chance. The worst thing you can do is not plan ahead; this leads to going back into credit card debt.

If you think you will casually save $10,000, you have another thing coming. Saving will have to be your top priority, even above enjoying your new debt-free status.

What happens when most of us see a zero balance on our credit cards? That’s right; we have a tendency to enjoy ourselves at the mall or Best Buy (in my case).

Personal loans vs. credit cards. Credit cards are good in a pinch. If you can’t remember how much you have on your debit card while paying at a restaurant, it’s better to use your credit card.

Become Insanely Productive During the Magic Hours

However, credit cards are not your friend. The power of compound interest is the 8th Wonder of the World.

Credit cards use this massive power against you. Personal loans at least have an amortization schedule that you can readily evaluate.

I used personal loans when we moved to a new duty station because my wife wouldn’t have a job. This gave us a security blanket while she looked for work.

I’m glad I didn’t try to act like everything would be perfect; that would have been a recipe for unexplained credit card usage.

Conclusion. Once you get your finances together, you’ll have even more options to keep your house in order.

Don’t Gamble with Retirement 2

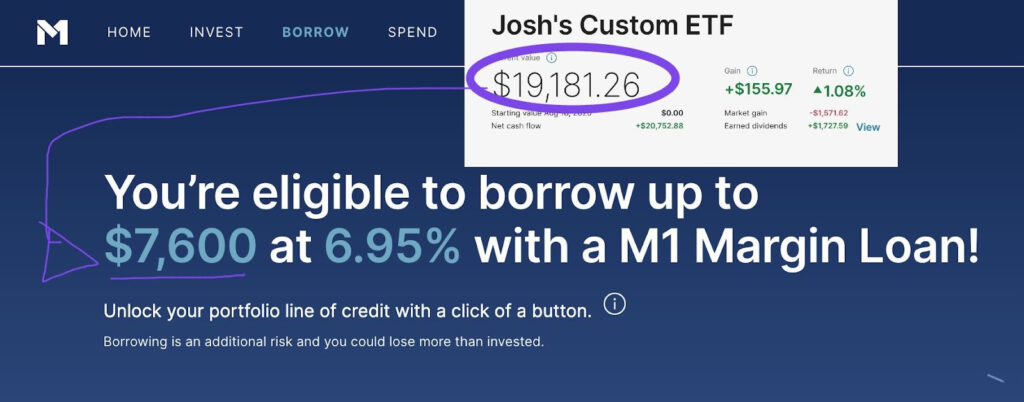

Now that I have a lot of money in my brokerage accounts, I can use leverage against it. So I can take a personal loan directly against my investment holdings.

This is how rich people like Elon Musk generate income without selling their shares. Plus, you don’t pay taxes on a loan.

Life is full of ways to get ahead. The first step is getting out of credit card debt and building an emergency fund. Personal loans can help you. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Leave a Reply