Learning to invest for income changed my life; I figured out how to build my own paycheck. Most people do not invest for income; they want to get rich quickly.

I dividend income investing into six different types, which you can read about here. One of my favorite types of income investing is closed-end funds.

Closed-end funds offer a simple, reliable way to extract income from the stock market. However, there are some things you must understand to be successful. Let’s begin.

Inflation Ate My Paycheck 101: Adjust Your Lifestyle Today

What are closed-end funds? Closed-end Funds (CEFs) are a collection of securities brought under one umbrella, similar to Exchange Traded Funds or ETFs.

CEFs differ from ETFs because CEFs maintain a set number of shares. ETFs grow and shrink as more money pours in or out of them.

Because CEFs have a set number of shares, they operate under a Net Asset Value (NAV). This is the value of the underlying securities in the CEF.

You can purchase CEFs at a premium or discount to NAV, depending on the market conditions. CEFs with great reputations often trade at a premium because people gravitate toward high-performing products.

Become Insanely Productive During the Magic Hours 2

The Cons of CEFs. Let’s start with some disadvantages of investing in CEFs, the first of which is high expense fees.

ETFs usually use passive investing, which means they do not have a fund manager—they trade along a static index.

CEFs most often use fund managers to keep everything operating smoothly; however, this comes at the cost of higher expense fees.

Additionally, CEFs use leverage to increase their returns, and the cost to borrow factors into the expense ratio.

You are paying for someone to look after your financial interest. When interest rates rise, the managers at PIMCO navigate the situation to keep your dividends coming to your account. I personally sleep well, knowing someone has control of the situation.

The Ultimate Solo Writing Business

CEFs versus interest rates. CEFs are extremely sensitive to interest rates because they use leverage (loans). Therefore, you will see your investments in the red quite often.

Investing in CEFs requires a different mindset than investing in stocks. Think of CEFs as buying rental properties.

The Advantages of using CEFs. Let’s say I have $1,000 to invest in CEFs, and I choose PIMCO Dynamic Income Fund (PDI).

Currently, PDI trades for $18.14 and has a monthly dividend of $0.2205—giving it a dividend yield of 14.5%.

RV Life vs. Homesteading: Which Lifestyle Suits You Best?

I buy PDI strictly for income. Sometimes, the price rises due to market sentiment and interest rates, and sometimes the price drops.

However, I continue to receive my monthly distortions. This is similar to owning a rental property. Sometimes your house value rises and falls, but you only concern yourself about your rent check.

The advantage of using CEFs is that you are not guessing in the market. You are buying groups of bonds, loan obligations, utility companies, and infrastructure businesses.

How to use CEFs effectively. You will need income if you are getting older, say the late 30s and 40s. It would be great to have a dividend growth portfolio of great stocks like McDonald’s (MCD) and Johnson & Johnson (JNJ).

House Rich, Cash Poor: Avoid the Housing Trap

However, these stocks don’t pay enough to change your life, at least within 5-10 years. You need income now, and that’s where CEFs perform best.

The best way to employ CEFs is to slowly convert one bill at a time. This means to start replacing your bills with CEF income one by one.

For example, we can start with your monthly Netflix bill at $18. At a 10% yield, you would need $2,160 to invest in CEFs to cover this bill.

Eventually, you want to replace all your monthly expenses with CEFs. If you are retiring to a small city or overseas, CEFs can provide your entire paycheck.

The Biggest Book on Passive Income Ever 2!

I currently receive $166/month in CEF income inside my Wells Fargo brokerage. Getting $100+ on the first of the month and $50 on the last day is nice.

This consistent income helps you understand the power of income investing and creating a paycheck replacement.

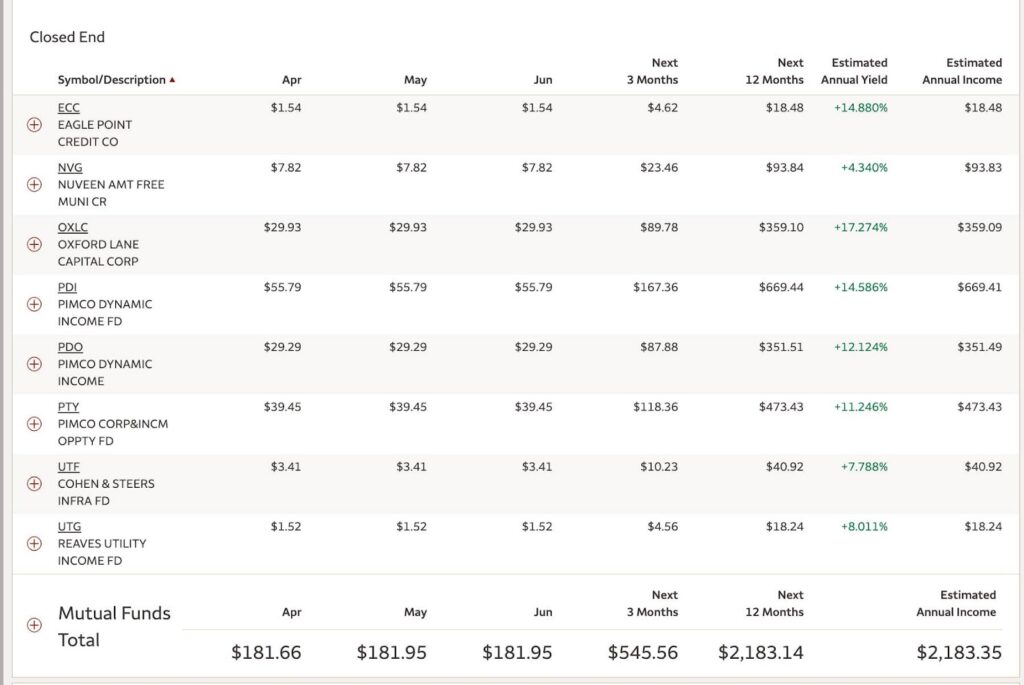

My favorite CEFs. I have been income investing for three years and have learned so much. I have also acquired many different CEFs along the way.

Income Portfolio vs. USDC: The Battle for 9%

Here are some of my top picks. Please do your due diligence on these products. A great resource is Rida Morwa on SeekingAlpha. He is the most established income investor on the platform.

- Bonds- PIMCO Funds (PDI, PTY, PDO), which specializes in bonds and other debt instruments. I use NVG for tax-free municipal bonds.

- Collateralized Loan Obligations- These are perhaps more rate sensitive than bonds, so be careful. I use ECC, OXLC, and XFLT.

- Instructure- UTF invests in boring products that keep the economy going and average roughly 7% yield.

- Utilities- UTG invests in boring utility companies that keep the economy flowing, averaging roughly 7% yield.

CEFs as part of your overall portfolio. I would love to put all my money into CEFs; however, that wouldn’t be wise.

CEFs rarely grow in value over time. You want to make your money when you buy (buy low). Therefore, you still want to invest in DGI stocks and index funds. CEFs are also known to pay special dividends from time to time.

5 Takeaways from “Shipping Container Homes”

CEFs work best as the base of your income stack. Let’s say you need $1,000/month in dividends to cover some bills.

I would generate about $500 from CEFs, then layer on other income types like preferred shares. Then, I suggest adding high-yield blue chips like Altria (MO) and AT & T (T) because they are not so sensitive to interest rates.

CEF reinvestment. Finally, I would add some high-growth dividend stocks like Microsoft (MFST), Visa (V), and Mastercard (MA).

Essentially, I am using my CEFs to allow time for my other stock to grow and mature. There is one last thing to remember about CEFs—reinvestments.

Retire Rich, Retire Comfortable with a Business 3

CEFs are not known for raising their dividends over time. This fact makes you responsible for building your income stream by reinvesting a portion into the portfolio.

A good starting number is 25-30% for reinvesting, perhaps more to grow faster. Watching my income continue to grow has been a massive highlight in my life.

Conclusion. Closed-end Funds are a considerable part of my income portfolio. Over the years, I only had to deal with one dividend reduction. Considering it was during the pandemic, I can live with that.

Besides Seeking Alpha, a good book on CEFs is “Step-by-Step Bond Investing.” You can also learn more about bonds and interest rates in “The Bond Book.”

CEFs are my favorite instrument on the stock market; however, you must have the right mindset. You cannot go into CEFs looking for capital appreciation, just income. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- Writer’s Comparison: M1 Macbook Air vs. GalaxyBook3 Pro 360

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: Fundrise vs. US Treasuries (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

PDF of the Month: Don’t Gamble with Retirement 10 (Free 419-Page PDF)

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply