As inflation slowly recedes, so does the hype for one of my favorite investment tools—Series “I” Bonds. The hype turned into mania when they paid 9.62% interest last year.

The goal of an “I” bond is to protect your cash from inflation while giving you a modest return. When they hit 9.62%, it was probably the safest 9% return you could achieve.

However, inflation is subsiding, and so are interest rates on “I” Bonds. This is still the perfect time to buy “I” bonds because it is always a great time to buy.

The Magic of Remote Work

The bedrock of your investment portfolio. As we convert from spenders to savers, we need to use all the investing tools at our disposal.

The first options to earn compound interest are high-yield savings accounts and certificates of deposit. These instruments can serve us well in our emergency funds.

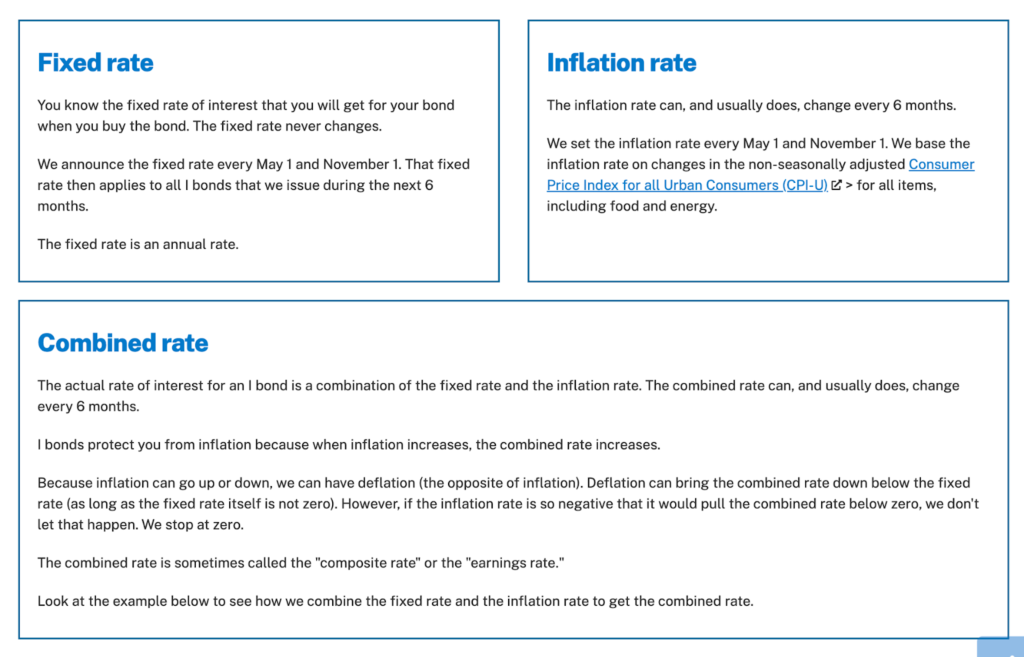

The next step is purchasing Series “I” Bonds from the US Treasury at Treasurydirect.gov. Each Series “I” Bonds is like its own unique high-yield savings account.

Depending on when you buy, they have a base interest multiplier, and then another current (six-month) rate gets applied.

How to Buy an Expensive Home Safely

These two numbers combine to give you your composite rate. The best part is all this happens automatically and doesn’t require any action from you.

Series “I” Bonds are the bedrock of your saving portfolio (not investing). We save and invest for different reasons, and Series “I” Bonds can give you “investing-like” returns without any risk.

Buy and hold forever. I am writing this article because I am seeing reports of people selling their “I” Bonds seeking more yield.

People will always seek higher returns (I do as well in my income investing portfolio), but that is not the point of Series “I” Bonds.

Don’t Fumble the Bag

The point of Series “I” bonds is to invest $100 in 2023 and have the spending power of $100 in 2053. If you understand inflation, you’ll understand why this is a challenging goal to accomplish.

Inflation erodes your spending power over time, so investing helps protect our capital from this erosion. Most people will never invest in the markets, so Series “I” Bonds offer the average middle-class person a great opportunity to conquer inflation.

Let’s look at inflation over 30 years. If you had $100 in 1992, you would need $208 in 2022 to achieve the same spending power (inflation calculator).

That means we must be aware of inflation. Even if Series “I” Bonds don’t give us market-beating returns, we can use them to counteract inflation.

Dividend Investing in Your 50s

Most people didn’t expect inflation to hit so hard in 2022. I started writing about inflation (Prepare for Inflation) in June 2021.

The people who already had Series “I” Bonds in their Treasury accounts were the big winners. They were not scrambling to buy the bonds after the 9.62% announcement.

They simply kept going about their day, and the government automatically increased their bonds to 9.62%.

The true magic of Series “I” Bonds is that you don’t have to track or follow their progress constantly. You buy and hold and let the government works its anti-inflation magic.

Saving for a House Down Payment #1: Single Person, Small City

There is a $10,000 annual limit. Another wrinkle to consider is the $10,000 annual limit per TreasuryDirect account.

My friend is a hardcore believer in Series “I” Bonds, so he buys $10,000 of bonds during January of every year. If he started selling bonds in favor of other higher-yielding products, it would be tough to rebuild his portfolio.

$10,000 may seem like a lot of money, but trust me; you can achieve this level of saving once you put your mind to it. If you fear the stock market, Series “I” Bonds are a great way to achieve a risk-free yield.

What is a risk-free yield? Bonds from the US Treasury are the highest-grade investments you can buy. If you don’t trust the government to repay you, there will be bigger concerns than your bonds.

Successful People Need the Most Help

It’s tough to achieve a high yield without some form of risk. There is a $10,000 annual limit on “I” Bonds because hardcore investors would pile into these instruments if they could.

The limit forces investors to buy Treasury Inflation-Protected Securities (TIPS) and Treasuries (bills, notes, bonds). Yes, investors love “I” Bonds, but a $10,000 annual limit doesn’t move the needle for them.

Bonds for family. In my article “The Bonds of Thanksgiving,” I wrote about the power of bond investing in building family wealth.

Passive Income Road Trip #7: Automated Business

Everybody in your family can have a TreasuryDirect account, even your newborn. You can purchase Series “I” bonds for the entire family up to $10,000 annually per person. So your family of four can purchase up to $40,000 per year.

Giving your children the power of inflation protection will set them up for future success. Yes, receiving an “I” bond for Christmas will not be ideal, but you get what I am saying.

You can start automatically purchasing “I” bonds for your kids by setting up auto-purchase. This method is what we call dollar-cost averaging.

Over the years, it will capture a few bonds with a higher fixed-rate stat (source TreasuryDirect). Currently, the fixed rate is 0.4%. This number will give you out-sized returns over bonds with a 0.0% fixed rate.

When you combine the 0.4% with the inflation rate, the higher fixed-rate will achieve a higher composite rate.

The Emotional Roller Coaster of Debt

I have been buying Series “I” Bonds since 2014 and have purchased a few bonds with excellent fixed rates. You can see a difference in their total amounts.

Conclusion. The moral of the story is to keep buying Series “I” Bonds year round. Buy them for yourself, your spouse, and your children.

Start a Sports League Toward Passive Income

As much as I love income investing with high-yield products, I still have to protect my principal. That is where Series “I” Bonds play a vital role in my portfolio.

Don’t get caught in the hype of selling your “I” Bonds to buy higher-yielding securities. The purpose is to buy and hold these wonderful tools for 30 years.

In 30 years, you should have a similar buying power to when you bought the bond. With inflation always working against us, Series “I” Bonds are essential to our saving and investing goals. Good Luck!

- PDF of the Month: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 9 (Free 394-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 3! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply