I recently discussed high-yield bond reinvestment as a safe way to assume more risk in your portfolio. It’s a great way to dabble in the waters of income investing.

My 30-year bonds just paid me their semi-annual payments, so it’s time to reinvest. Today, I will walk through how to convert a reasonably low-yield coupon payment into high-yield income. Let’s begin.

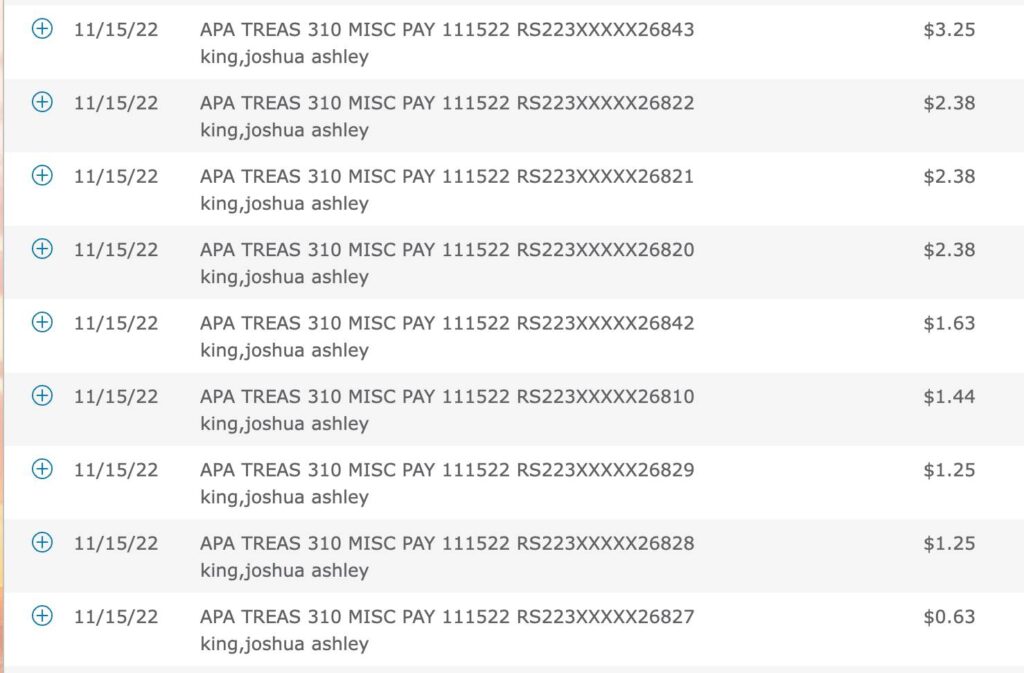

Receiving your coupon payments. The first step is to receive the coupon payments from your bonds. As I wrote in “How to Buy and Track 30-Year Treasury Bonds,” each bond provides its own separate payment.

As you can see, I received payments from nine bonds for a total of $16.59. Don’t forget that you also must pay tax on interest payments at the end of the year.

Understanding Cash-on-Cash Return

I will pay my taxes with cash flow early next year, so I don’t have to worry about myself in the present. You’ll need to determine your tax strategy as well.

The Treasury Direct website also allows you to change the location of your coupon payments. So you can deposit them directly in a checking account near your brokerage.

Time to go shopping. Now for the fun part of bond reinvestment—going shopping. I divide my high-yield income investing products into six types: preferred shares, closed-end funds, mortgage REITs, dividend ETFs, business development companies, and high-yield blue-chip stocks.

With $17 in my pocket, I went shopping across all the types to find the best deals. I shopped on my Wells Fargo brokerage, which does not support fractional shares.

RE Lifestyles 3: Renovate & Rent vs. Fix & Flip

Places like M1 Finance, STASH, and Cash App support fractional shares, so it is much easier to spend your $17.

Looking for deals. Looking for great deals isn’t all about finding the highest yield. You have to look at your overall portfolio composition to ensure you have some balance. Here are some of the deals I reviewed:

- Preferred Shares: Public Storage P (PSA.P), Price: $16.79, Yield: 5.90%

- Closed-End Funds: Oxford Lane Capital (OXLC), Price: $5.22, Yield: 17.41%

- Mortgage REITs: AGNC (AGNC), Price: $9.13, Yield: 15.77%

- Dividend ETFs: Virtus Preferred (PFFA), Price: $19.18, Yield: 10.27%

- Business Development: Capital Southwest (CSWC), Price: $18.03, Yield: 10.98%

- High-Yield Blue-Chip: AT&T (T), Price: $18.97, Yield: 5.95%

And the winner is… Oxford Lane Capital (OXLC) is a closed-end fund specializing in collateral debt obligations (CLOs).

Living Overseas Passively on Royalty Income

I choose OXLC because it is a monthly paying CEF, and all debt products have been on extreme discounts because of rising interest rates.

Other options. You have many more options than high-yield when you receive your coupon payments. You can invest in index funds, Series “I” Bonds, or Real Estate Investment Trusts.

Eventually, you may need to use your coupon payments for income. I recommend you reinvest 25-30% of your payments into income-producing securities to keep growing your wealth.

What’s the point of bond investing? You may ask, “Why not invest directly in these high-yield securities?” Investing in bonds first aims to protect your capital (or principal). Although you may only earn 4% on your bonds, it’s a safe 4%.

The Magic of Income Investing

You do not depend on the stock market by taking the extra step to invest in bonds. The volatility of the stock market can drive people to do silly things.

Once you get the hang of high-yield income investing, you may want to invest directly in the markets. However, it’s always a good idea to tuck some capital safely into certificates of deposits, high-yield savings accounts, Series “I” Bonds, and Treasuries.

Using bond income for speculation. You can also use some of your bond income to speculate in the markets.

Currently, a few places can net you big rewards (or failures). I am tracking Facebook (META) and Sofi Finance (SOFI) as underdogs moving forward.

Debt-Free? So, What’s Next?

Also, the crypto markets are in complete disarray. I started a small crypto portfolio on M1 Finance by investing $100. I may add $100/month over the next year.

Conclusion. By running your income through bonds, you free yourself from stressing over losing the principal. Your portfolio will grow much slower but will be much safer.

If you are getting older, preservation of capital is your number one goal. You do not have the time to recover from market craziness.

The Magic of Dividend Growth Investing

However, even young people can benefit from bond investing. Only some people have the disposition or emotional stability to invest directly in the markets.

As a matter of fact, most people invest for capital gains, which is good during a bull market. During a bear market, loss of capital can make people panic sell and lose even more principle.

What are your investing guidelines? Do you prefer to invest directly in the markets or filter through bonds first?

I do a combination of both methods. However, I take 1-2 hours daily to read the market news, conduct analysis, and perform due diligence. That’s what it takes to become a great income investor. Good Luck!

- PDF of the Month: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 4 (Free 112-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 8 (Free 445-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Book Design: Design Tips on YouTube

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply