I was writing an article about my Recession Investing Plan yesterday and realized how tricky it is to purchase 30-Year Treasury Bonds.

I started buying these bonds three years ago and had to learn via trial and error. I haven’t purchased a 30-Year bond in a couple of years because yields have been low.

However, yields are heading towards 4%, and it’s a great time to start building cash flow from fixed income. I have an entire series dedicated to fixed-income securities. With that, let’s buy 30-Year Bonds directly from the US government.

- Investing for Interest 101: What is Fixed Income?

- Investing for Interest 102: Super Safe Savers

- Investing for Interest 103: The Treasure in Treasuries

- Investing for Interest 104: Bountiful Bond Funds

- Investing for Interest 105: The Hunt for Baby Bonds

- Investing for Interest 106: My Favorite High-Yield Savings Account

- Investing for Interest 107: Series “I” Bonds for You and I

- Investing for Interest 108: The Magic of CD Ladders

- Investing for Interest 109: Series “I” vs. 30-Year Bonds

Setting up your TreasuryDirect Account

The first step in the process is to set up your account on TreasuryDirect.gov. It’s been over 15 years since I set my account up, so I am a little rusty.

Treasury Direct is extraordinary because you can also buy Series “I” Bonds and start accounts for your children. Today we are focusing on 30-Year Bonds; however, the process will be the same for 10-Year Notes and 20-Year Bonds.

Buying Bonds at Auction

The US Government sells 30-Year Bonds at auction. This will affect you in two ways: you can’t buy when you want, and the price can change.

First, we can look up the last prices from the previous auction here. You can also look at the upcoming bond auction schedule here.

Results from Auction

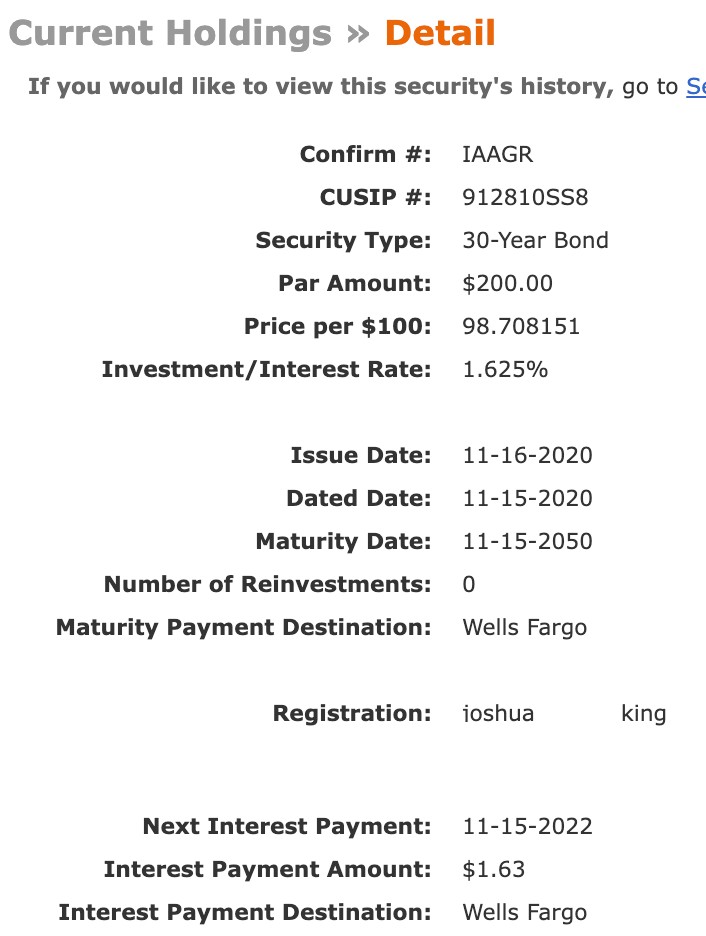

The results from the last auction are vital to understanding your bonds’ yield. The interest rate is the amount of interest the government will pay you—it determines your coupon payment.

However, the price you pay for your bond affects your yield. You can see here the price per $100 is $90.57. Therefore, you paid $90 for a $100 bond, which increases the yield.

Your bond may show 3.0% interest, but your yield on cost is 3.511%. These numbers are significant to bond investing—please read “The Bond Book” to dive deeper into bonds.

Preparing for Upcoming Auctions

You will want to do a few things to prepare for the monthly 30-Year Treasury Auction.

- Keep an eye on 30-Year Treasury Yields

- Find the Auction Date

- Determine if it is a New or Reopening Auction

- Set up your C of I funding

Keep an Eye on 30-Year Treasury Yields

It’s essential to keep awareness of the bond market. It has been turbulent recently and can catch you off guard if you are not tracking changes.

With an auction, you can pay more or less than your desired bond price. For example, I once wanted to buy a $400 bond.

However, early in the Pandemic, bonds were selling at a premium. So, my $400 bond was going to cost $440. I didn’t have that amount in Certificates of Indebtedness, so the bond purchase did not process.

You want to prepare for bond auctions by looking at the current interest rates (I’ll explain later) and current yields (they are different). You can track daily 30-Year Treasury yields here.

Find the Auction Date

The government usually holds 30-Year Treasury Auctions in the middle of the month. You can find the upcoming auction dates here.

Determine if it is a New or Reopening Auction

This step was one of the most confusing parts of the buying process. The US government only changes interest rates on 30-Year Bonds four times a year.

The interest rates stay the same for three months. The new interest rate is not a reopening, and the next two months are called reopenings. Not to worry, my tracker quickly shows how these work.

30-Year Bond Months: February, May, August, November

29-Year, 11-Month Bond Months: March, June, September, December

29-Year, 10-Month Bond Months: April, July, October, January

Going into a new 30-Year Bond auction, you will not know what interest the US government will stamp on the bond. This means you want additional funds in your C of I account, just in case.

However, going into reopening months, you will know the interest rate on the bond, and you will have an idea of yields. You can closely predict the price per $100.

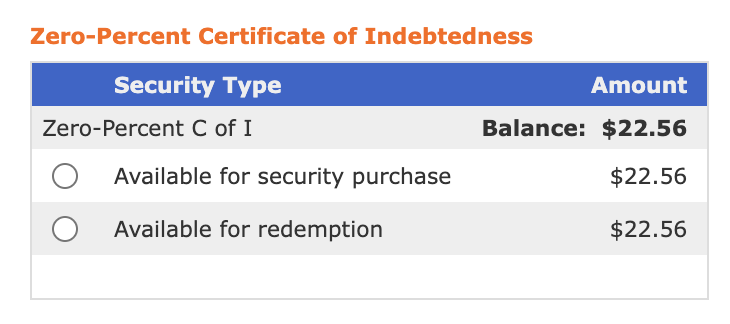

Set Up Your Certificate of Indebtedness Funding

The C of I is basically a checking account inside of your Treasury Direct account. It doesn’t accrue interest, however.

I like to use the C of I account to buffer the madness of an auction. As I said, you can closely predict the price per $100. But, you can also get caught off guard.

You don’t need to purchase C of I’s to invest in 30-Year Bonds; you can link directly to your checking account.

But what if bond prices spike upwards? What if you expect to pay $400 for a $400 bond, but it increases to $440? Not only do you pay more, but your yield also decreases.

I prefer to add in the C of I step. I automate the purchase of my C and I every month. Then, on the 5th of each month, I have a reminder to go in and set up my bond purchase through the BuyDirect tab on the top of the TreasuryDirect Website.

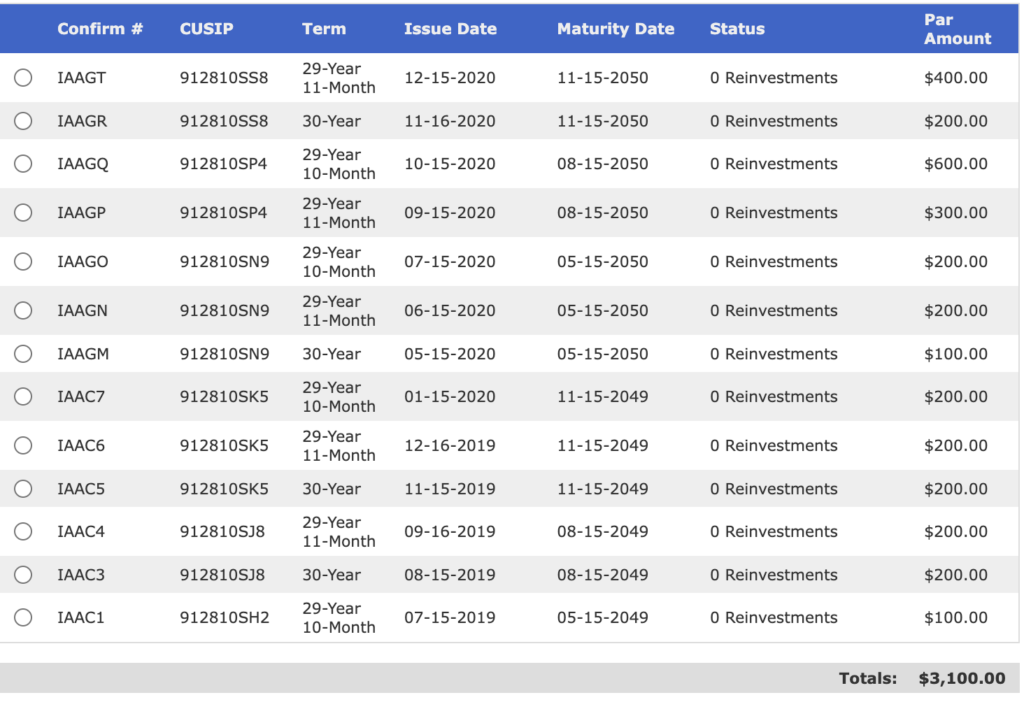

Tracking Your 30-Year Bonds

You will have to play around with the TreasuryDirect website to get the hang of it. However, once you start buying bonds, you’ll want to track your interest payments.

The good thing about fixed income is that it is fixed. You can determine your actual payments down to the penny.

You can also set up each individual bond to pay to a different checking account. I had to create my own tracker because I couldn’t find one. Let’s review it.

My 30-year Bond Tracker

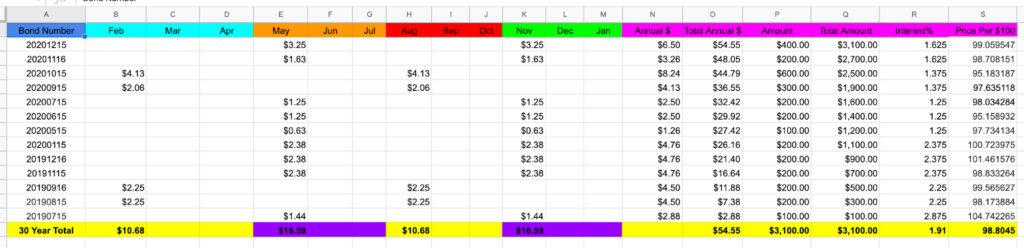

Luckily for you, I am giving away my 30-Year Bond tracker for free. You can download it right alongside this book on my website. Each bond pays twice a year, six months apart.

Bond Number: The date of the bond, per the TreasuryDirect website.

February: Bonds you purchase in Feb, Mar, Apr, Aug, Sep, and Oct, will pay in Feb and Aug.

May: Bonds you purchase in May, Jun, Jul, Nov, Dec, and Jan will pay in May and Nov.

Annual $: The total annual amount from the bond.

Total Annual $: The cumulative amount from all the bonds.

Amount: The amount on the bond.

Total amount: The total of all your bonds.

Interest %: The interest rate on the bond.

Price per $100: The price you paid per $100. You can find this when you click into each individual bond. You can determine your yield from this number. If you paid over $100, your yield is lower than the stated interest rates. If you paid less than $100, your yield is higher.

How the Payments Look in Your Checking Account

The US Government doesn’t combine your interest payments. Each bond is its own account; you will receive many payments on payday.

You can see the payments on August 15th align directly with my tracker. Again fixed income is great because it is fixed.

Conclusion

I hope I have provided you with a lot of value. Getting into bond investing is intimidating. However, bond investing can become fun once you get the hang out of it.

It is different from investing in dividend-paying stocks. Please download the free book and bond tracker. Tell your friends, and look into my books and articles. Good Luck!

- PDF of the Month: How We Plan to Retire on Dividends 4 (Free 139-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 4 (Free 149-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 8 (Free 445-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply