Today I am going to discuss the ultimate grudge match between credit cards and debit cards. Many people are out to get the best rewards; however, this is a comparison between two mindsets at its core.

The credit card camp likes to talk about points for travel and cashback rewards. There are truly some great rewards programs, but you must always show restraint.

Debit cards offer fewer rewards and protection; however, they give you the financial security of knowing the money is in the bank.

Good Debt vs. Bad Debt

With that quick background, let’s determine who should use which card. Also, can you leverage both of these together to get the best results?

The case for credit cards. The average person should NOT use credit cards. Heck, I shouldn’t even use my credit card. But, there are some ways to leverage credit cards to improve your financial situation.

Credit cards require strong financial education to take advantage of these perks and rewards. First, you must pay them off monthly in their entirety. Most spenders cannot accomplish this feat.

Become Insanely Productive During the Magic Hours

You are playing the bank’s game if you have a running credit card balance. Credit cards are best when you are debt-free and earning interest from other sources. You can either pay interest or earn interest.

How I use credit cards. I use credit cards when my budget is in disarray from lifestyle changes. For example, I recently moved from Florida to San Diego, California.

Things in California were a mess. I needed to buy a car, furniture, plane tickets, set up my kitchen, etc. It was easier for me to put everything on the credit card.

Now, once the explosion of spending is over, I can pay down the credit card and move back to using my debit card.

Don’t Gamble with Retirement 2

I also use credit cards for “emergencies” that are less than $4,000. I don’t like to use my cash emergency fund when I have the option to use a credit card. It is a way to punish myself and ensure I pay the debt back.

If I use my cash, I can wiggle around paying it back quickly. Since I hate credit card debt with a passion, I know I will pay it off in a couple of months.

Debit cards your way. I have two fantastic debit cards that I use differently. I have a debit card attached to my favorite high-yield savings account (HYSA) and one that pays me dividends. Let’s look at both of these individually.

20 Creative Ways to Make Money From Home

My HYSA debit card. I have an HYSA through Discover, which has a 1% rewards debit card. I put all of my personal budget cash into my checking account.

When I was in Japan, my personal budget was $800/month. Here in California, it is $1,500/month. If I spend the entire amount, I will earn $15 in cash rewards that Discover will put directly into my HYSA.

$15 may not seem like a lot, but it is a massive amount of “free” money that will then earn compound interest for a long time. I’d rather make $15 than pay $15 to a credit card.

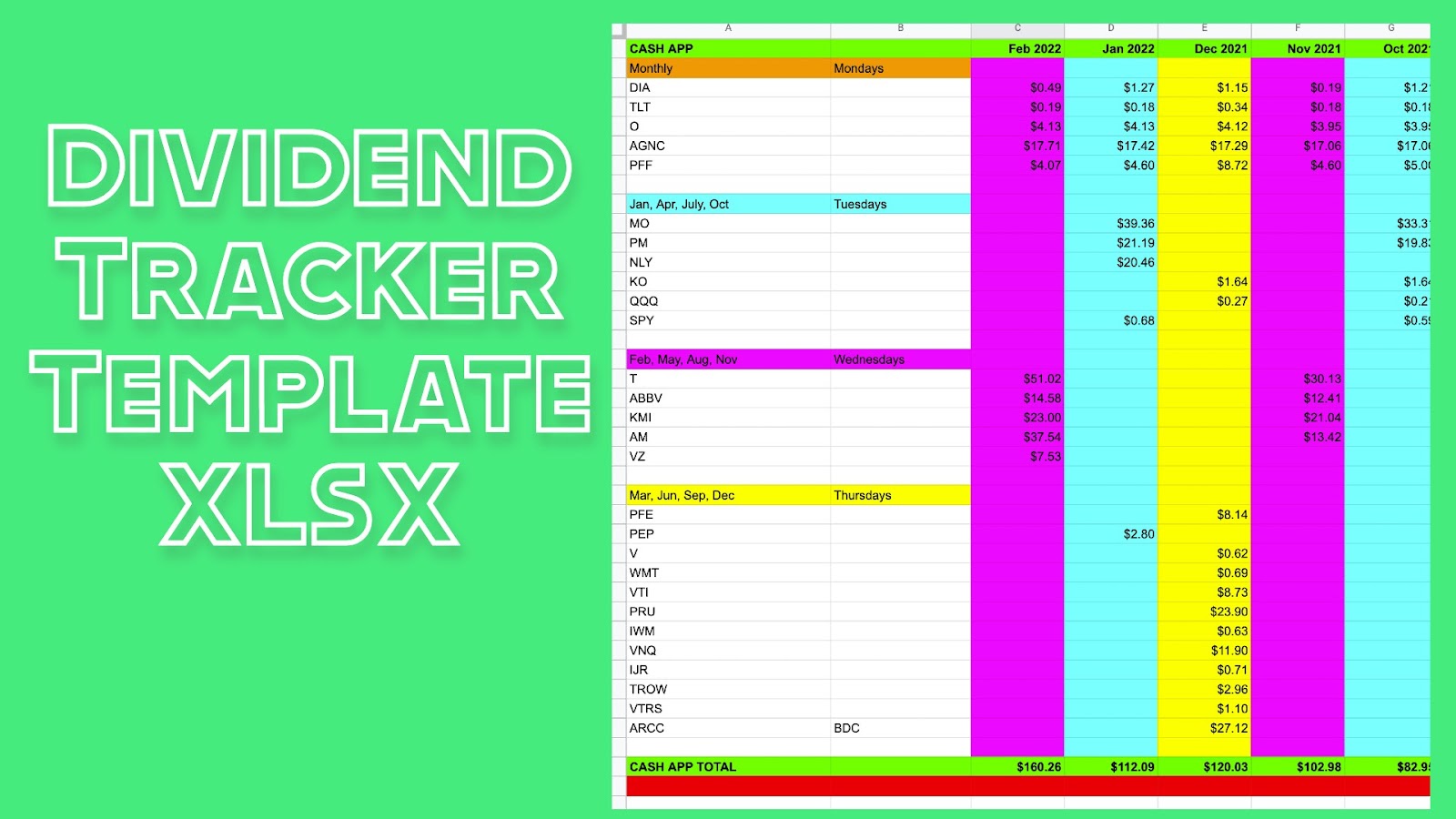

My Dividend Debit Card. I have a debit card through the Cash App. I also have a brokerage account through Cash App that pays dividends directly to my checking account.

Why I Am Investing in Bitcoin

I call this my dividend debit card, and it is incredible. I currently earn roughly $200/month in dividends that I can spend on whatever I want. It is guilt-free money I can spend outside of my personal budget.

Earning dividends requires financial education that most people are most willing to build. However, if you can pull this off, you will be in a class of your own.

Credit cards vs. debit cards. So, where should the average person seek their rewards? The correct answer is the debit card attached to the high-yield savings account.

In all situations, the best answer will be the HYSA rewards debit card. Not only do you get 1% rewards, but you also earn 2% interest (currently) on your HYSA.

TAP Your Home Equity

By using the HYSA and debit card together, you earn “free” money and build compound interest. This technique can be your introduction to the world of passive income.

Credit cards AND debit cards. Once you become more advanced, you can use these cards in tandem to create great wealth and relieve stress.

If you have an excellent budgeting program, you may not want to disturb it for an unusual expense. For example, you may need to spend $400 for a new garbage disposal unit at the end of the month.

Once you plan to pay for it with future cash flow, you can put that expense on your credit card. You can do this instead of depleting your personal budget for the rest of the month, which may cause stress and anxiety.

How We Plan to Retire on Dividends

You can pay the $400 back the following month from cash flow. Now, you earned some rewards, took care of an emergency, and saved yourself a lot of headaches.

However, this is for advanced users. If you WANT to spend $400 on video games and don’t have a plan for future cash flow, don’t use your credit card.

Small decisions equal big decisions. Life is about small choices. If you cannot manage a $400 expense, how can you purchase a $400,000 home?

It may sound trivial to worry about putting $400 on a credit card, but it means taking your life seriously.

Preferred Shares 105: Long-Term Preferred Strategy

Debit cards show the world that you take your future seriously. It means you care about saving your money today versus instant gratification.

Conclusion. My top recommendation is the high-yield savings account with a rewards checking account. I do mine through Discover and have been a fan for over three years.

Next, I would open a Cash app account and add blue-chip dividend-paying stocks. These stocks will give you cash flow to your debit card. It is impressive to have a self-refilling checking account.

Become a Real Estate Agent/Investor

Finally, once I am completely debt-free, have an emergency fund, and have passive income, I can add credit cards to juice my returns.

If my credit card spending gets out of hand, I need to leave them at home and delete them from my Amazon profile.

I used to have to remove my credit cards from Amazon, but now I hate credit debt so much that I have no spending issues. That results from paying off $77,000 in debt—you become immune to its allure.

Life is about the daily decisions leading to balance. You must weigh your spending today versus your needs for tomorrow. In most cases, debit cards give you functionality today and success tomorrow. Good Luck!

- PDF of the Month: Retire Rich with a Business 4 (Free 149-Page PDF)

- Free PDF Downloads: Download FREE PDF LIST here

- Financial Mindset: Become CEO of Yourself 2 (Free 196-Page PDF)

- Retirement Planning: Your Retirement Planning Guide 2 (Free 255-Page PDF)

- Investing: How We Plan to Retire on Dividends 2 (165-Page Free PDF)

- Cryptocurrencies: Counting on Crypto 2 (Free 159-Page PDF)

- Real Estate: Financial Independence through Real Estate 2 (Free 123-Page PDF)

- Business: Retire Rich, Retire Comfortable with a Business 2 (Free 185-Page PDF)

- Latest DGWR: Don’t Gamble with Retirement 8 (Free 445-Page PDF)

- Everything!: The Biggest Book on Passive Income Ever 2! (book)(Web Edition)(Art Edition)

- I bought a Kindle Oasis: Check it out on Amazon

- Read My Books for Free: Free Kindle Books Schedule

- Crypto Exchange: My Favorite Crypto Exchange VOYAGER (Join Voyager)

- Kindle Unlimited: Why I Finally Subscribed Kindle Unlimited (learn more)

- Book Reviews: 505 Takeaways from 101 Books (pdf)

- Writing: The Publishing Chronicles (Part 1, Part 2, Part 3, Part 4, Part 5)

- Best REIT- Fundrise: REITs vs. Homeownership (Join Fundrise)

- Follow us: On our Facebook Page and Join our Facebook Group

- Support the Channel on Cash App: $Kingmarine1981

- For more detailed analysis, join my Youtube: MFI YouTube Channel

Monthly Dividend Tracker Template: Buy on Etsy

Disclosure: I am not a financial advisor or money manager, and any knowledge is given as guidance and not direct actionable investment advice. I am an Amazon Affiliate. Please research any investment vehicles that are being considered. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it. I have no business relationship with any company whose stock is mentioned in this article. All Right Reserved Military Family Investing

Leave a Reply